Who is Gen Z and Why Do They Matter?

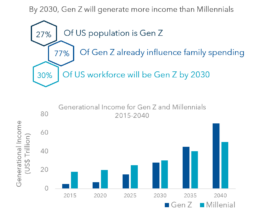

Born between 1997 and 2012, the Gen Z generation has already surpassed millennials, establishing itself as the largest generation in the United States, boasting an impressive 86 million individuals(1). The sheer magnitude of this population is matched by their significant spending power, currently estimated at $143+ billion in the US(2). Looking forward, their potential is staggering, with projections of ~$60 trillion in spending power as they inherit an astonishing $75 trillion of wealth from the Baby Boomer generation(3).

Education is a key differentiator for Gen Z, as 57% are projected to complete a college education, outpacing the 44% of millennials who achieved the same milestone(4). This makes Gen Z the most educated generation in history, setting the stage for lucrative career opportunities and higher earning potential.

Over 38% of Gen Z individuals have entered the workforce already, and by 2030, they are projected to comprise 30% of the US workforce(5). This significant presence in the job market is mirrored by their influential role in family spending decisions — 70% of Gen Z report that they wield influence over expenditures on household goods, travel, food and beverage, electronics, and more(5).

The sizeable population of Gen Z, their potential to shape most of the income and expenditure, and their current influence on purchase decisions underscore their significance to banks and other industries.

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Exhibit 1. Gen Z by the Numbers(6)

Gen Z's Unique Characteristics

The financial landscape is undergoing a rapid transformation, propelled by the emergence of Gen Z. As the first generation to grow up entirely in the digital era, Gen Z possesses characteristics and preferences that distinguish them from their predecessors. To effectively engage with this demographic, financial institutions must tailor their strategies and offerings accordingly.

- Digital Natives

Gen Z is the first generation to grow up in a fully digital era, leading to unique digital preferences and behaviors. As much as 98% of Gen Z individuals in the United States own a smartphone(7).

Implication: FI’s need to prioritize digital solutions and provide seamless, user-friendly mobile apps to meet Gen Z’s expectations for convenient, fast, and accessible financial services.

- Financial Consciousness

Gen Z demonstrates a heightened awareness of financial matters and seeks to make informed financial decisions. Close to 80% of Gen Z individuals believe it’s important to start saving money early, with only 46% feeling confident about their financial knowledge (vs. millennials at +65%)(8).

Implication: FI’s should provide financial education resources, tools for budgeting and saving, and personalized financial advice to cater to Gen Z’s desire for financial empowerment.

- Authenticity and Personalization

Gen Z values authenticity and personalized experiences, expecting tailored offerings and genuine interactions. Evidently, 52% of Gen Z individuals prefer brands that offer personalized experiences(9). Moreover, content creator-driven platforms like Tik Tok, Discord, and Twitter increasingly influencing their purchase decisions through authentic reviews and peer recommendations.

Implication: FI’s should leverage customer data and technology to provide personalized banking solutions, customized recommendations, and seamless omnichannel experiences that resonate with Gen Z’s desire for authenticity and individuality.

- Social and Environmental Consciousness

Gen Z has a strong emphasis on social and environmental issues, influencing their consumer choices and brand loyalty. 83% of Gen Z individuals in the US believe companies should take action to address social and environmental issues(10).

Implication: FI’s should integrate sustainable practices, offer socially responsible investments, and engage in community impact initiatives to resonate with Gen Z’s values and build long-term relationships.

- Diversity and Inclusions

Gen Z values diversity and inclusivity, seeking representation and fairness across various aspects of life. Studies show 79% of Gen Z individuals believe it’s important for brands to show people from different backgrounds in their advertisements(11)

Implication: FI’s should prioritize diversity and inclusion in their marketing, branding, workforce, and product offerings to create an inclusive and welcoming environment for Gen Z customers.

Targeting Gen Z customers now can yield significant lifetime value for financial institutions. As Gen Z represents the future workforce and the largest consumer demographic, capturing their loyalty early on can result in long-term customer relationships. Gen Z customers have the potential for extended engagement, higher product adoption, and increased cross-selling opportunities, leading to enhanced lifetime value. Additionally, by establishing a strong connection with Gen Z now, financial institutions can benefit from their potential growth in income and wealth accumulation over time, maximizing the return on their marketing and acquisition investments.

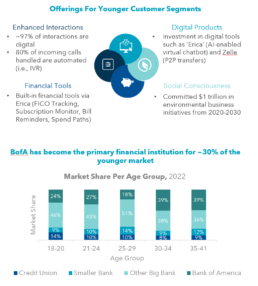

Exhibit 2. Bank of America Case Study(12)

Exhibit 3. Common Offerings for Gen Z

How Financial Institutions are Targeting Gen Z Today

Gen Z today is currently in the midst of major life transitions and in the beginning of their financial journeys. 34% are currently students, 19% are employed full-time, and 24% are employed part-time or self-employed(13). A majority of them are beginning to settle down as 71% of Gen Z adults plan to move in the next 5 years as they graduate or find new jobs. Almost 43% of Gen Z members expect to buy a house within 5 years,(14) so they have begun thinking about their financial standing and steps to build a good credit score. The priorities of Gen Z and the expected life transitions they are going through are reflected in the products that are popular. Financial institutions aware of these demographic changes are targeting Gen Z through products with suitable fee structures and rewards, interactive online experiences, and financial literacy content. All of these products are tailored to Gen Z’s needs and help them kickstart their financial journeys.

No/Low-Fee and Credit Builder Cards

Gen Z, despite their perceived risk, has demonstrated responsible credit behavior, with 63% already credit active, carrying an average debt of $2,000, and maintaining a utilization rate of 31%.(15) Notably, 50% of credit-active Gen Z individuals fall within the prime and above category surpassing the 39% of credit-active millennials at the same age(16). 70% of newly acquired accounts globally are for fee-based products, with over 60% of these coming from younger consumers(17)

Product characteristics Gen Z look for are accessible credit and debit products with minimal or no fees, no minimum balance requirements, overdraft protection, and innovative rewards programs tailored to their needs and spending patterns. Some of the most popular products targeting Gen Z are the Bank of America Student Card, Wells Fargo Clear Access Card, Discover Student Checking Account, Chase First Banking Debit Card, Capital One Journey Student Credit Card etc(18).

Financial Literacy Tools to Kickstart the Journey

Gen Z needs financial literacy tools to kick-start their financial journeys, Currently, only 46% of Gen Z feel confident about their financial knowledge, compared to 61% of millennials or 52% of Baby Boomers(19). However, Gen Z is showing a keen interest in financial literacy and is eager to learn. Over 43% of Gen Z said they want to learn to save, 38% want to learn to manage their expenses, and 36% want a class on filing their taxes(20). Financial institutions can foster relationships with Gen Z individuals by offering products that would ease this financial education and begin building customer loyalty and long-term client relationships. Financial institutions have picked up on this trend and are attracting the attention of Gen Z through financial education tools.

Revolut has piloted “Introducing Edutainment” aims to educate through quizzes, videos, blogs, social media posts, and tutorials on Instagram and TikTok. Bank of America has introduced the “Better Money Habits” series offering financial education content for high school students, college students, parents, and international students.

Bolster Marketing and Brand Identity

Gen Z regularly interacts with brands and companies online, expecting authentic and interactive content. To capture their attention, financial institutions need unique visuals that fit each audience, focusing on customer service and support, collaborating with influencers, and creating a clear brand image. Financial institutions are becoming acutely aware of the power of online interactions in generating business. Neobank Step Bank partnered with Charli D’Amelio, a renowned TikTok influencer with a following of 141 million users, to effectively communicate its brand message to the teenage demographic(21). JPMorgan has set up shop in Decentraland(22), a primary metaverse environment, where it has access to a monthly active user base of about 300,000 people and 18,000 daily users(23). To target this generation, financial institutions need to bolster customer acquisition and marketing strategies through all relevant digital and social media channels.

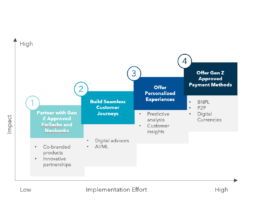

Exhibit 4. Potential Gen Z Strategy

Other Gen Z Strategies

Preparing for the future customer base will require financial institutions to innovate. While Gen Z individuals might currently prefer low-fee products, financial literacy, and social media presence, as they grow older their preferences and needs will likely change. This digital native generation will require products and services that are able to provide them a convenient experience, seamless customer journeys, and advanced payment methods. To gain the loyalty and business of the future Gen Z individual financial institutions can partner with innovators or build new products in-house:

1. Partner with Gen Z Approved FinTechs and Neobanks

Successful fintech partnerships lower in-house investments for banks. It enables traditional banks to create a compelling digital banking experience through apps and products that easily integrate into their ecosystem. Financial institutions like Morgan Stanley, WaFd Bank, and Community Financial Credit Union, have partnered with neo-banks to offer tech-forward services. Popular fintech Greenlight has created a new partnership offering from Greenlight for Banks that allows banks and credit unions to offer the fintech’s suite of banking and education products to their customers through a co-branded landing page and apps. This follows Greenlight’s successful partnership with JPMorgan Chase to offer an account designed for kids called Chase First Banking, which reached 1 million users rapidly(24) Blue Ridge Bank also teamed up with Mos, a student financial aid fintech. Through this partnership, Blue Ridge helps students navigate the financial aid application process to reduce debt and build a healthy financial future.

2. Build Seamless Customer Journeys

The digital experiences provided by most traditional FIs today are suboptimal. This is indicative of a larger issue — 40% of Gen Z individuals are unable to locate what they are looking for online and 25% report that their FI’s website or mobile app did not support their needs(25). With a significant portion of Gen Z (~35%) accessing financial services through mobile phones, financial Institutions must modernize their online client journeys(26).

Financial institutions typically handle 50 client journeys like opening a new account, borrowing money, promoting customers’ financial well-being, handling transactions/payments, and solving customer issues. When it comes to these journeys, Gen Z expects more than conversational AI/chatbots, online apps, AI-powered personal finance tools, and digital value-added services.

3.Offer Personalized Experiences

Gen Z desires more customized interactions as they are used to trading personal data for a better experience for services like Facebook, Amazon, Google etc.

By using data such as credit profiles, account information, everyday touchpoints, and transaction histories, financial institutions can create customized, relevant end-to-end experiences for customers. By some conservative estimates, personalization could lead annual revenue uplift of 10% for financial institutions(27).

In the past decade, the majority of FIs have set up their data analytics infrastructure, however, they struggle to transform these analytics or data points into actionable insights. By tracking customer interactions and obtaining a 360-degree perspective of the consumer, developing customer insights on lifetime value, and social presence, and using sophisticated analytics and ML to recognize trends and patterns financial institutions can create a truly seamless customer experience(28).

4.Offer Gen Z Approved Payment Methods

Newer products like digital wallets, P2P payment apps, and BNPL are getting adopted quickly by Gen Z. Today, Zelle is available to 95 million people in the US and quickly becoming a go-to-choice for splitting the tab. Some have begun offering BNPL through one-to-one arrangements with specific merchants (e.g., TD Bank is providing BNPL for NordicTrack, the fitness equipment manufacturer), while others are creating models that are the backbone behind BNPL propositions (e.g., Westpac has a BaaS arrangement with Afterpay(29). Considering predictions for BNPL alone reaching 35+ million Gen Z individuals by 2026(30) financial institutions need to future-proof their BNPL strategy.

Emerging Challengers

When is comes to Gen Z banking, it’s the Neo banks and FinTech startups that are getting it right via innovative products, financial literacy tools, personalized experiences, savings solutions, etc. In 2022 there were 250 digital challenger neo-banks worldwide, with more on the way. These challengers to legacy financial institutions are here to stay, and they’re going after Gen Z. They are quickly gaining ground and their clientele is mostly tech-savvy younger generations. Neo banks are creating a straightforward banking experience with tech-advanced interfaces. There are many examples of challenger neo-banks going after Gen Z, with Copper, Revolut, Greenlight, Jassby, Osper, RoosterMoney, Current, FamPay, Monzo and Step being some of the most prominent players.

Copper

Copper Banking is a Seattle-based neo-bank that focuses on empowering and educating teens in the banking sector. It has secured $45+ million in funding and has gained over 800,000 users since its launch in 2019. Copper offers a range of financial products, including a debit card, peer-to-peer payments, direct deposit, automatic savings options, and integrated financial education content.

Through their app, Copper provides tailored features for young users, along with functionality for family members. Their goal is to foster financial independence among teens by offering smart portfolios, managed investments, and the opportunity to invest with as little as $1.

Copper has created a comprehensive repository of blogs, articles, and guides within their app to support financial literacy. These resources cover important topics such as saving, investing, budgeting, and card usage, presented in simple terms. The interactive website interface enhances user engagement and includes sections on common financial mistakes made by Gen Z, as well as educational videos on subjects like collateral and mortgages.

Exhibit 5. Copper Case Study(31)

Revolut, a UK-founded fintech startup established in 2015, has become a leader in banking solutions for the Gen Z and Millennial generations. With $1 billion in revenues in 2022, it has successfully targeted over 25 million young consumers. Revolut offers a wide range of innovative financial products to meet the unique needs of Gen Z and Millennials through traditional banking features and groundbreaking offerings such as stock and cryptocurrency trading, personalized budget management, and attractive cash-back programs.

To cater to the younger demographic, Revolut introduced “Revolut <18:, a specialized product is designed for teens aged 13+, with parental or guardian approval which combines money management tools, digitized payments, and investment management solutions. The secure mobile banking app is a core feature of Revolut <18, allowing young users to easily track expenses, set savings goals, and receive real-time notifications, while the linked prepaid debit card enables secure online and in-store purchases. In addition to practical features, Revolut places a strong emphasis on financial education and offers educational resources and financial tips to promote money management, budgeting skills, and responsible spending habits among young individuals.

Exhibit 6. Revolut Case Study(32)

In Closing..

The young and restless Generation Z is growing rapidly and is already the largest generation in the United States. As this generation becomes the predominant workforce with the largest purchasing power, it is important for financial institutions to innovate to cater to their unique nature and product preferences. Gen Z has distinct tastes and preferences compared to millennials. They are digital natives, with a very diverse cohort, who emphasize social and environmental consciousness. Today, Gen Z individuals are seeking low/no fee products, financial education tools, personalized products, and online content with a clear brand identity. By fulfilling these needs, financial institutions can capture their loyalty. However, as they grow older and gain more purchasing power, financial institutions will need to reposition their offerings to fit their evolving needs. Financial institutions must make targeted long-term bets and provide Gen Z innovative experiences, tailored products, collaboration with the newer FinTechs, etc. There are already strong challengers in the market, namely fintech, and neo-banks, who are targeting Gen Z, so financial institutions have their job cut out for them!

__________________________________________________________________________________________________________

- “US Population by Age and Generation”, Knoema, 2020

- “Gen Z and the Future of Spend”, Forbes, 2021

- “Gen Z and millennials are expected to inherit over $60 trillion in wealth by 2050” Business Insider, 2021

- “What We Know About Gen Z So Far”, Pew Research, 2022

- “Uniquely Gen Z”, IBM Institute, 2020

- Euromonitor, 2021

- “Gen Z And The Rise Of Social Commerce”, Forbes, 2022

- “Gen Z Banking”, EVERFI, 2022

- “Uniquely Gen Z”., IBM, 2020

- Gen Z Buyers: The Future is Ethical Consumption” Maersk, 2022

- YPULSE, 2022

- “Bank of America Grabbing 1 in 3 Gen Zs and Millennials with Mobile”, The Financial Brand, 2022

- “Gen Z Values Home Ownership”, Realtor, 2021

- “Gen Z Values Home Ownership”, Realtor, 2021

- “Your Guide to Gen Z’s Credit Behaviors and Preferences”, Trans Union, 2022

- “Your Guide to Gen Z’s Credit Behaviors and Preferences”, Trans Union, 2022

- American Express Co Earnings Call, 2023

- “Banking for Z Next Generation” Banking Journal, 2022

- “ Gen Z: Stepping Into Financial Independence”, Investopedia, 2023

- “Generation Z: Keen on Learning About Personal Finance and Credit” Experian, 2020

- “Teen-Focused Digital Bank Step Raised $50 Million Series B“,Business Insider, 2021

- JP Morgan OpensDecentralandLounge to Capitalize on Metaverse, 2022

- DecentralandHolds First-Mover Advantage in Battle Against Meta, Yahoo Finance, 2023

- “Greenlight’s New B2B Offering Brings Kid-focused Banking To Traditional Firms”, Banking Dive, 2023

- “Gen Z And Millennials Use Bank Branches Because Of A Poor Digital Experience”, Forbes, 2021

- “US Gen Z mobile banking user stats (2020-2025)”, Insider Intelligence, 2022

- “What Does Personalization in Banking Really Mean”, BCG, 2019

- “What Does Personalization in Banking Really Mean”, BCG, 2019

- “Can banks grab the buy now, pay later opportunity?”Accenture, 2022

- “Why Buy-Now-Pay-Later is the Trend to Watch”, Global Payments, 2023

Read More

Banking on You – Personalization in Financial Services

Capturing and sustaining attention is key to building customer loyalty, driving sales, and standing out in a competitive landscape. In this attention economy, what really helps business maintain relevance is to personalize the interactions for their needs, context and preferences.

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.