The Real Time Mandate

Once a cumbersome and time taking process, payments have been altered forever. The increased speed, transparency, and ease of transacting through apps like Venmo, Zelle, Google Pay etc. represents the reality of payments today – this reality has been powered by the fast-growing phenomenon of instant payments.

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide.1 However, the overall opportunity remains untapped. Visa Inc. estimates US$ 185T in payment flows across B2B, B2b, B2C, P2P and G2C.2 Despite the opportunity, uptake of real time payments is still in early stages, with most growth coming from the P2P players. As customers get used to instant P2P payments and start expecting a similar experience across all types of payments, the next wave of untapped money flow is likely to be captured. In addition, as local real time payment schemes upgrade their functionality, and new systems like the FedNow are launched, other use cases will become more favorable.

Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

With increased competition, not providing this capability to your customers can be very costly. However, several challenges need to be overcome. For banks that have relied upon traditional payments systems, the transition to real-time comes ridden with strategic, operational, and technical challenges. Deciding the right connectivity model for real time payment rails, modernizing current technology infrastructure, managing security concerns, and training dedicated teams to handle real time operations etc. represent key hurdles. At this stage, a holistic future-proof strategy is needed. There is a need to think through and dissect elements such as the target customers, the offering ,and competition to define the correct value proposition. In addition, chalking out a holistic plan with clearly defined goals and objectives, investment needs, and a holistic business case, among others, will help remove ambiguity from the implementation process.

There is a sea of opportunity, if only one can identify the best way to tap into it!

Growing Ubiquity of Real Time Payments

Traditional payments involving complex processes and delays have no place in today’s fast paced environment. With everything being immediate, it is no surprise that real time payments have sky-rocketed in recent times and will continue to do so throughout the decade. RTP transactions are likely to exceed 300 billion by 2023, growing at ~40% per year worldwide. Multiple factors are responsible for this growth, including:

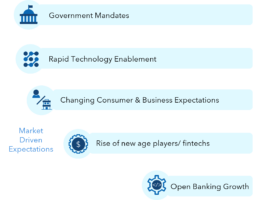

Government Mandates

Increasingly, governments and regulators are taking active part in the payment’s fabric of the country, including the development of RTP systems. For example, the launch of UPI in India, was driven by the central bank’s desire to reduce high levels of cash usage and bring more citizens and businesses within the ambit of the formal economy and taxation.

Currently, 55+ countries around the world have launched RTP schemes.3 Pushed by varying reasons, governments and other regulators have come to recognize the ability of instant payments to drive economic value.

In addition, by directly being a propagator of these payments, governments’ have been able to generate trust in these new payment methods and influence consumer behavior.

Exhibit 1: Drivers for Growth of Real Time Payments

Market Driven Expectations

Real time payments are fast becoming the go-to payment channel. Adoption is being driven by:

Rapid Technology Enablement. High proliferation of smartphones and digital apps, adoption of cloud-based solutions and growing ubiquity of new technology like 5G, Blockchain and IoT are all working towards creating a conducive environment for real time payments by offering support for higher speed, rich context, connectivity, and security.

Changing Consumer & Business Expectations. Consumers of today, especially millennials who make up the largest generation in the workforce, expect payments to be speedy, transparent, and convenient. In fact, 30% of individual consumers consider it a key factor when selecting a bank, and 24% are willing to switch banks if they lack this capability.4 On the other hand, even businesses are demanding a simple and fast experience to saving costs, streamline their operations, and protect themselves from hackers.

Rise of New Age Players/ Fintechs. In recent years there has been an influx of big tech players and fintechs constantly redefining the payments world. Not only has the supply of these players increased,

but consumer familiarity and demand for their solutions has gone up as well. In fact, almost ~64% of consumers around the world have used at least one fintech platform this year, compared to 33% in 2017.5 The innovative services and experiences offered by these players have spurred a new desire for instant and convenient payments systems to be established.

Growth of Open Banking. While maturity of open banking varies across markets, regulatory support for it has been universally rising. Markets are realizing the powerful combination of real time payments and open banking – open banking frameworks can support a more seamless integration and on-boarding process for financial institutions looking to piggyback new payment networks and offer those services to their own customers.

Unlocking the Next Wave of Growth

Visa estimates total money opportunity of US$185T across the globe, comprising of B2B, B2b, B2C, P2P and G2C flows. Despite the current high growth, it stands uncontested that there is a substantial money movement opportunity worldwide. Most markets are still in nascent stages of adoption and have only focused on P2P use cases until now as a substitute for cash and cheques in interaction between individuals.

To benefit from the next wave of growth, regulators, banks and FIs will need to support and serve a broader set of use cases beyond P2P. Even business payments are now ripe for innovation. For example, in the US, while B2B accounts for 76% of all money flow6, most of it is done via wire, check or ACH – systems that are slow, cumbersome to deal with and lack the ability to offer robust information and visibility into end-to-end payment transactions. Additionally, as the pandemic wreaked havoc in the supply chains across countries, many suppliers realized the need for real time payments tied to end-to-end tracking of goods.

Critical Need for Adoption

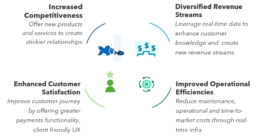

Creating new solutions based on real time payments can prove helpful in creating stickier client relationships. Moreover, banks can also take advantage of new functionalities such as ‘Request to Pay’, a messaging layer, and combine it with instant payments to enable payees to seamlessly pay them from their bank account.

Diversified Revenue Streams. Real-time processing generates immediate and accurate data that can provide deeper insights into the customers’ behavior, as well as help in finding new revenue streams. The real-time push is also adding greater weight to the concept of open banking and APIs, which will make data aggregation even easier. While data is invaluable, especially in B2B transactions, enabled in part by ISO 20022, it will ease the reconciliation process significantly.

Enhanced Customer Satisfaction. A bank’s ability to provide RTP is deemed the second-most important factor in choosing a banking partner (after it’s ability to provide solutions throughout the customer’s business lifecycle).7 Tech savvy small businesses, their customers, and suppliers need a faster and more robust way to pay bills, manage their cash flow, and protect themselves from hackers. Financial institutions of all sizes need to allow customers to pay the way they want to, including at the time they would like. With real time payments, banks can further digitize their customer experience to make it seamless and intuitive, ease onboarding and accept payments across various customer touchpoints.

Exhibit 2: Benefits of Real Time Payments for Financial Institutions

Improved Operational Efficiencies. Fast payments reduce costs for the maintenance and upgradation of legacy systems. Even operational costs are lower due to immediate decisioning of any exceptions encountered with transactions. The newer technology required for real-time also helps relieve banks from managing and synchronizing multiple databases, overseeing aspects of recovery and business continuity.

Several institutions are benefitting from a reduction in product time-to-market by ~90%8 because real-time processing allows immediate product configuration and migration.

Several institutions have already transitioned to Real Time Payments Rails with a variety of use cases. For example:

JP Morgan Chase has launched a ‘Request for pay’ solution with real-time payments that lets its corporate clients send payment requests to their retail customers through the bank’s app and website. The company has already begun a pilot with a corporate fintech to launch this service.

Commercial BankProv partnered with COCC as its core provider to connect to the RTP network operated by TCH (The Clearing House). The goal is to support high volume transactions, especially from its cryptocurrency clients, who need to move funds fast to mitigate valuation risk from the inherent volatility. In addition, the RTP network also allows the bank to enhance reconciliation, and immediately settle funds.

.

Roadblocks in the Path to Success

Banks are faced with multiple challenges on their journey to go real time. From connecting to the right rails to to developing the ‘true’ business case, there is a lot that needs to be figured out. Challenges include:

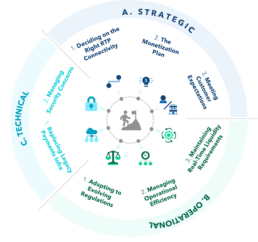

A. Strategic Challenges

- Deciding on the right Connectivity. Many banks have yet to decide how they’ll access the RTP system. They must decide between direct connectivity vs. connectivity through third-party service providers (TPSP). Banks need to choose the right partner from amongst hundreds of options (the choice of partner will impact the business case significantly), assess client demand, and determine the underlying technology strategy.

- The Monetization Plan. Currently there isn’t a dedicated model for banks to charge for real-time payments and it is hard to advocate for RTP without cannibalizing the existing credit card business. Additionally, as pricing will play a key role in the success of real time payments, banks need to decide whether to base it off ACH/ wire pricing or a combination of the two.

Exhibit 3: Challenges hindering real time adoption

- Meeting Customer Expectations. Often, specific customer groups, such as merchants and traders, are used to specific payment methods so might be reluctant to set up new processes. Banks will likely need to customize how they facilitate this transition. In addition, identifying the right use cases and user experience for existing customers poses another challenge. Users may have varying preferences and banks need to actively work towards identifying high value prospects and the right use cases and experience for them.

B. Operational Challenges

- Maintaining Real Time Liquidity Requirements. Faster payments pose a new challenge to banks’ liquidity management by making it more difficult to predict future liquidity positions. While in the case of traditional batch settlements, banks know in advance when transactions should settle, in case of real time settlements, it is driven by what the bank’s customers do. Banks can’t get pre-notified by a customer of payments going out or money being received.

- Managing Operational Efficiency in Real-Time. A key consideration is how a firms’ various functions must adjust to real-time. For example, due to the irrevocability of RTP transactions, funds are gone once the transaction is approved, without the ability to cancel or contest payments. To effectively disapprove of any potential fraudulent transactions, the right controls need to be put in place. Moreover, banks must also decide which operational area will support real-time payments for various clients, and how they will access the scarce expertise and skillsets needed to run these services.

- Adapting to evolving regulations. Regulatory action around information security, privacy, performance etc. is rapidly evolving as real-time payments are gaining traction. As a result, banks will need to be abreast of the latest regulations and identify ways to mitigate risks, dedicate the right personnel to manage areas such as consumer complaints, queries and avoid any issues that could lead to additional expenses to adjust the system.

C. Technical Challenges

- Replacing Legacy Payment Infrastructure. Traditional systems are typically not fast enough to handle each transaction end-to-end at an individual level, including processing, settlement and reconciliation. Additionally, they don’t offer 24×7 availability which is crucial to handle volumes at any point of the day. Banks must modernize their legacy systems by analyzing their existing technology, improvement costs and employee support to implement these services without disrupting current services.

- Managing Security. Due to reduction of payment time and payment touchpoints, they are increasingly becoming vulnerable to security threats. Banks are struggling to adapt their existing security infrastructure to short review times that are necessary for real-time processing. They need to identify and mitigate fraudulent transactions at lightning speed. This requires complex analytical capabilities and use of AI/ ML to assess transactions and offer predictive insights in real time.

Road to Implementation

There are a lot of components to real time – different networks, applications, and services – that customers want to enable and benefit from. The sheer task of being on top of so many components has made institutions unsure of where real time payments fit into their broader strategy. Thus, a holistic approach is needed, and several areas need to be dissected to define a bank’s real-time payments value proposition.

Exhibit 4: Roadmap to Implement Real Time Payments

Target Customers

Banks need to determine which use cases to prioritize. Knowledge of the growth potential and attractiveness of diverse use cases is important. Some key questions that bank need to answer include:

- Who are high value prospects for each real time payments solution? Are they existing or new customers of the bank?

- What use cases represent the maximum potential for growth and adoption by high value customer groups?

- Which customer touchpoints and outreach programs will be best suited to meet the needs of target prospects?

Competition

Lessons can be learnt from successes and failures of real time strategies deployed by direct and indirect counterparts. It is key to ‘skate to where the puck will be, not where it has been’. Key questions include:

- Who will the relevant competitors be, and which areas are they serving vs. the areas that represent whitespace opportunity?

- What lessons can be learnt from the deployment of real time payments solutions by industry counterparts?

- How do competitors successfully differentiate their solutions from others in the industry?

- Are there players from other industries and verticals that have or will foray into real time payments? How are they likely to impact our success? What is the best defense/offense?

Product/Value Offering

To support a diverse set of use cases, it is first important to connect to the most desirable rails. From government owned local RTP networks to real-time card rails offered by firms like Visa and Mastercard, there are multiple options to choose from. The choice of rails will play a monumental role in the features and functionalities that the bank will be able to offer to its end users. Upon deciding the rail of choice, the next step is to conduct a thorough due diligence and risk evaluation to assess the impact on onboarding, deposits, and revenue from connecting to the vendor. Lastly, to ensure a smooth transition to instant payments, the right technology systems need to be in place as the requirements of system performance, availability and scalability are critical for smooth operation. The technical architecture required to send and process payments in real-time is also quite different to the existing infrastructure.

Key questions include:

- Which real time rails and vendors will be best suited to serve planned use cases, meet customer expectations and offer major functionalities needed for the offering?

- What tech requirements will be necessary to support the real time payments solution? (24x7x365 operations, prefunding requirements)

- What will the partnership model look like with the vendor of choice? How will revenue, costs, and risks be divided?

Just defining a robust value proposition will not be enough – sufficient thought needs to be put into aligning with existing strategy, determining investment needs, defining the operational model, and fleshing out the full business case. This involves looking at the commercial market and analyzing potential gains from using real-time payments in comparison to traditional rails. Lastly, an execution playbook is also needed. Banks will be able to use this playbook to also test hypotheses against the real world including (1) Are expected volumes being generated (2) Are the right customers being served and onboarded? (3) How is RTP impacting the bottom line? Etc.

In Closing...

While real-time payments have already been in vogue for some time now, significant value remains untapped across use cases like business payments that go beyond traditional P2P. Banks/FIs need to hit the bull’s eye in identifying the best way to capitalize on this whitespace and do so better than competitors.

As banks begin implementing/ ramping up their real time transition, pertinent challenges need to be overcome – from the potential cannibalization of the existing card business, to performance and scalability issues faced with legacy infrastructure.

Developing a clearly defined holistic roadmap will be crucial in guiding success. To start, banks should rigorously assess target customers, the product offering, and competitor positioning to define their real-time payments value proposition. Alongside, a holistic business case needs to be developed to capture maximum benefits. Lastly, a clear understanding of the operating model and development of an execution playbook are imperative to win in this space.

References:

- ACI Worldwide ‘Keeping Pace with Innovation in Real Time Payments’

- Visa 2020 Investor Day Presentation

- Modern Treasury ‘Real Time Payments around the world’

- Pymnts.com

- Tipalti

- Bai.org

- Citizens Commercial Banking

- Adyen

Read More

From Interface to Intelligence

The next frontier of digital commerce is not better checkout, but better coordination. This whitepaper examines how agentic AI is transforming fragmented transactions into intelligent, autonomous experiences - and what businesses must do to stay ahead.

Banking on You – Personalization in Financial Services

Capturing and sustaining attention is key to building customer loyalty, driving sales, and standing out in a competitive landscape. In this attention economy, what really helps business maintain relevance is to personalize the interactions for their needs, context and preferences.

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.