Credit Cards are Fading...

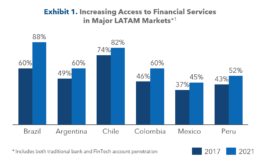

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem. Although total retail spending decreased 18% during the first year of the pandemic, P2P transfers and real-time payments have seen high levels of adoption. In fact, digital banks and wallets have reached more than 50% of the banked population and 33% of the overall population (1).

However, this growth in payments did not translate to growth for credit cards. Credit cards have only grown 1-3% in the recent years. While credit cards accounted for ~60% of all LatAm card purchases in 2019, it has decreased to ~35% due to the increasing popularity of debit and prepaid cards (2).

There are multiple reasons for this struggle:

Competition from FinTechs. Technological payment options such as P2P payments, advanced security features and digital payment cards have gained traction due to the growing mobile penetration (70%)(3). Especially real-time payments have been cannibalizing credit cards as they are free of charge to the customers and help merchants bypass interchange fees.

Barriers to Customer Uptake. Costs of obtaining a card and associated red tape have also damaged the popularity of credit cards in the region. In Brazil, new card adoption has been low because, on average, consumers pay 190% annual interest on credit cards. Moreover, less than 50% of Latin Americans have a credit score history to begin with, and credit bureaus of countries like Chile only register negative strikes against credit, further lowering card approval rates(4).

Regulatory Challenges. Many Latin American governments have laws in place that restrict credit card growth. The Central Bank of Argentina has fixed APRs at 55%, which has been deterring issuers from promoting their credit cards due to limited opportunity for interest revenue (5).

Governments in Brazil, Colombia and Puerto Rico issue their social benefit payments through prepaid cards distributed by public banks. While this is good for lowering cash usage and increasing financial participation, prepaid and debit cards pose a threat to credit cards by capturing first-time customers.

Exhibit 1. Increasing Access to Financial Services in Major LATAM Markets*

...But their value continues

The challenges above might be discouraging for issuers, but credit cards are still one of the most important products within their portfolios. Credit cards are big contributors to customer loyalty and holistic growth:

Higher Revenue. Credit cards typically contribute higher revenue compared to other payment products because of their multiple revenue streams. Cardholders pay annual fees and interest on unpaid balances , while merchants are charged interchange fees, allowing issuers to monetize their credit cards with each purchase. Research shows that customers spend up to 100% more when they use credit cards and are more likely to accept higher prices (6).

Access to Insightful Consumer Data. Big data analytics have become integral to the payment industry and credit cards give issuers access to insightful data (e.g., purchase frequency, spending categories, customer service preferences etc.). These data points allow issuers to drive growth across their entire product portfolio by segmenting customers, personalizing product offerings, implementing risk management processes, and incorporating retention strategies.

Long-Lasting Client Relationships. Despite a sharp drop credit card satisfaction during the C-19 pandemic, 89% of cardholders indicated that they would remain loyal to their issuers. This is because credit cards are interconnected with entire ecosystems of financial products (e.g., higher tier cards, investment products and fixed-term loans), resulting in longer-term and more intertwined issuer-client engagement (7).

Using Rewards to Catalyze Growth

LatAm’s dynamic and competitive landscape calls for innovative credit card value propositions. Issuers have a powerful tool at their disposal to accomplish this: reward schemes. ~80% of customers consider rewards as a differentiator in choosing a card, however, credit card reward satisfaction rates are at ~50%: once revolutionary and eye-catching reward schemes such as the single-rate universal cashback and point programs are no longer considered interesting. Issuers now need to offer newer, more attractive value propositions (8).

There are multiple whitespace opportunities for such rewards in Latin America. Issuers have focused their card strategy towards high- and middle-income segments and mainly offered travel rewards. However, the C-19 pandemic has rendered travel rewards difficult to redeem and issuers have been slow to adjust their reward strategies. On the flipside, issuers have struggled with lowering their cost to acquire low and lower-middle income segments. Instead, so far these segments have been served by prepaid and debit cards, which have a significantly lower ability to drive growth due to their restrictive revenue models.

Rewards present an opportunity for credit card issuers to offer value propositions tailored for the nuanced needs of customer segments, markets, and competitor strategies.

1. Dynamic Rewards

Latin American issuers already deploy some dynamic strategies for credit cards: many FinTechs offer dynamic CVV numbers for actively changing security credentials, and traditional banks proactively increase credit lines to stimulate additional spending. It is now time for reward schemes to evolve in order to respond to varying spending patterns and keep their cardholders engaged.

Conditional One-Time Offers

One-time offers that reward task completion are a way to gamify the cardholder experience.

Issuers can offer higher earn rates, special bonuses, and discounts to customers for meeting certain spending minimums to aid in customer activation. For example, in Brazil, where card members prefer to give clothes and shoes as Christmas gifts, spending at select department stores can be rewarded during this period. However, Colombians generally prefer to buy their holiday gifts early so a similar strategy can be offered in November instead (9).

Accelerated Rewards for Revolving Categories

Reward schemes can be made more dynamic by offering higher rewards for select spending categories on a revolving basis. For example, BNPL schemes for larger purchases like travel bookings, are quite popular. Since these schemes are usually set-up directly with merchants as a direct withdrawal or cash payment, they don’t incur interchange fees. Thus, there is an opportunity for issuers to adjust their revolving reward categories seasonally to transfer high-ticket purchases like travel bookings to credit cards.

2. Flexible Rewards

~70% of credit card customers modify when/where they purchase to maximize their rewards, and issuers need to integrate flexibility in their reward schemes to meet customer expectations (10). Flexible strategies not only give customers freedom to adjust how they earn rewards, but also provide issuers with a tool to readjust their value proposition when market conditions change.

Accelerated Rewards for Preferred Categories

One of the most popular reward schemes is to allow customers to choose the category they would like to earn accelerated rewards in and update this category periodically. However, because this scheme is commonplace in crowded markets, issuers need to offer additional flexibility to differentiate themselves. While most cards allow for the selection of one category monthly, an enhanced accelerated reward strategy could let customers select 2-3 categories monthly or quarterly. More flexibility would motivate customers to use a single card for all of their purchases, resulting in more active card usage.

Flexible Reward Redemption Options

Travel co-branded cards have struggled during the pandemic because earning miles no longer held real value at a time with extensive restrictions and low demand for travel. Similarly, cards issuing cashback did not perform well in markets where the pandemic eroded people’s incomes and getting direct discounts became more important to the cost-conscious customers. By giving customers a variety of redemption options such as cash, points and discounts, issuers can meet the changing needs of their customers and respond to market shocks easily. Moreover, issuers can target a greater range of customer segments with a single product through the versatility of the multiple redemption options.

Exhibit 2. Spectrum of Reward Flexibility

3. Hyper-personalized Rewards

While there has been plenty of innovation in the payment space, credit card reward schemes have mainly stayed the same in many Latin American nations. Most credit card rewards still follow a one-size-fits-all approach (e.g., single-rate reward earning schemes), resulting in generic value propositions that fail to attract customer interest.

Research shows that customers are 8x more likely to remain loyal to their credit card if the loyalty program is personalized to their needs and expectations. However, only 22% of credit card customers are satisfied with the level of personalization they are getting today (11). Issuers can employ hyper-personalized reward schemes that put the customer first to gain a competitive edge.

Automatic Accelerated Reward Category Selection

Cardholders whose loyalty program makes them feel special and recognized have a 2.7x higher satisfaction rates. Issuers can automatically adjust their customers’ top earning category to offer a tailored reward experience (12).

This strategy offers a personalized alternative to rewards with manual category selection as customers would be assured that their rewards follow their spending patterns and deliver maximum benefits.

Targeted Offers at Select Merchants

Discounts on select merchants is a common reward scheme in markets such as Argentina and Uruguay, and issuers can differentiate themselves by offering spend-driven personalized discounts.

This strategy is especially impactful for lower-income customer segments who are seeking to keep their costs low. Targeted and personalized discounts present the card as an ever-evolving product that prioritizes the customers’ needs.

4. Alternative Rewards

There is still significant white space in Latin America for differentiated credit cards. Dynamic, flexible, and hyper-personalized rewards can be further enhanced by targeting particular customer segments and offering unique value propositions in crowded yet static environments.

Double Rewards

Double reward refers to issuing rewards in two installments: the first half when the customer makes purchases and the second half when they pay off their balance in full. This is a low-risk strategy for issuers to market credit-builder products to first time cardholders.

Double reward is also suitable for markets where there is a shortage of credit reporting agencies and bureaus such as the Bahamas. Promoting healthy credit behavior can help issuers build internal credit reports that can later be used to upgrade customers to higher card tiers.

Reward Match

Issuers can match the rewards earned by a cardholder at their account anniversary as a bonus. Reward matching is especially suitable for mature card markets with high attrition rates and intense competition, such as Brazil where cardholders have on average 3.6 credit cards (13). Customers in these markets often switch between cards to maximize rewards, and reward matching can build customer stickiness due to the year-long waiting period. For cards with annual fees, the delay in redemption also locks in fees for another year, partially offsetting the cost of the reward match.

Cryptocurrency Rewards

Latin American countries have been adopting cryptocurrencies at a record rate: El Salvador has declared Bitcoin as its legal tender and companies across the region offer crypto-backed loans with APRs as low as 2%. Issuers can take advantage of this recent trend by offering cashback in popular digital currencies (e.g., Ethereum and Bitcoin) or depositing rewards into a trading platform to be converted into the customer’ preferred cryptocurrency (14).

These rewards are suitable for markets with high economic uncertainty and a lack of trust in the local currency. Due to hyperinflation in countries like Venezuela and Argentina, cryptocurrencies are already being used by citizens to hedge their incomes against spiking consumer prices (15). Crypto rewards in these markets would turn rewards into a form of investment and drive spending even during economic crises. Such rewards are also especially appealing to a younger and more tech-savvy customer base.

Minimizing Issuer Liability

One of the most important aspects of establishing a reward strategy is ensuring that the issuer is protected against high acquisition and ongoing costs of rewards. An average issuer’s reward expenses have shown a ~30% increase in the recent years, reinforcing the importance of protecting the bottom line while offering rewards (16). Issuers can employ the following strategies to turn credit card rewards into a sustainable growth tool:

Require Minimum Accrual for Redemption

Minimum accrual requirements create target spending thresholds and can promote card use for several months for thin file customers. Such requirements ensure that customers enticed by welcome offers actively continue using their cards.

Flexible Reward Redemption Options

This strategy encourages cardholders to continue making purchases on their card and remain active throughout the statement month. Allowing access to rewards like cashback after the closing date often prompts cardholders to use these rewards to lower their card debt, keeping the monetary value of rewards within the issuer’s card ecosystem.

Incentivize Internal Reward Redemption

Reward multipliers can be offered on internal redemption portals such as travel booking and gift card purchases. This reduces the real cost of rewards as issuers usually lock in discounted rates through their partnerships with service providers and keep a larger share of interchange fees.

Establish Caps on Rewards

Imposing earning caps is especially popular with cards that offer highly accelerated rates for select categories. As customers can selectively use different credit cards to maximize their rewards, caps ensure holistic card use for all purchase categories.

In Closing...

The LatAm payments industry is growth exponentially, and credit card issuers must proactively enhance their value proposition to remain competitive and capture their share of this growth. There are still several whitespace opportunities for credit cards across the region, and issuers can use reward schemes to their advantage.

Dynamic, flexible, hyper-personalized and alternative reward schemes have a great potential to help issuers with customer loyalty and activation, driving long-term growth. However, reward schemes cannot follow a one-size-fits-all approach. Credit card markets across the region vary greatly and reward strategies need to be tailored to competitive landscapes, regulatory frameworks, macroeconomic conditions, and attributes of targeted segments.

Issuers also need to have a holistic approach to connecting with their customers and going beyond product-focused strategies. The dynamisms of the payments landscape in LatAm requires issuers to pair cards with additional offerings such as digital wallet integration and advanced security features, offering holistically innovative credit card value propositions.

__________________________________________________________________________________________________________

- LATAM Payments Megatrends Report, Americas Market Intelligence, 2021

- Acceleration in LATAM Digital Payments, PYMNTS, 2021

- Mobile Penetration in LATAM, Geopoll, 2021

- LATAM Lending Landscape, Lending Times, 2018

- Financial Cards and Payments in Argentina, Euromonitor International, 2021

- Do People Really Spend More With Credit Cards, Forbes, 2018

- Credit Card Satisfaction Study, JD Power, 2021

- Majority Say Credit Card Rewards Are Very Important and Drive Card Usage, Ipsos, 2021

- Christmas in Latin America, Statista, 2015

- What’s Trending in Loyalty?, Bond Brand Loyalty, 2016

- What’s Trending in Loyalty?, Bond Brand Loyalty, 2016

- What’s Trending in Loyalty?, Bond Brand Loyalty, 2016

- Brazil Country Report, Verisk Financial, 2021

- Bitcoin Adoption in Latin America, Nasdaq, 2021

- Inflation Seen Spiking Festive Spending Splurge, Reuters, 2022

- Consumer Payment Survey, Deloitte, 2020

Read More

From Interface to Intelligence

The next frontier of digital commerce is not better checkout, but better coordination. This whitepaper examines how agentic AI is transforming fragmented transactions into intelligent, autonomous experiences - and what businesses must do to stay ahead.

Banking on You – Personalization in Financial Services

Capturing and sustaining attention is key to building customer loyalty, driving sales, and standing out in a competitive landscape. In this attention economy, what really helps business maintain relevance is to personalize the interactions for their needs, context and preferences.

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.