How did we get here?

ORIGINS TO PRESENT DAY

It is no surprise that the financial services industry has been a fertile valley for technological disruption. The rise of online banking powered by bank mainframe computers was an early testament to this. It fundamentally altered the relationship between end-consumers and financial institutions by rendering branch visits no longer necessary. Eventually we reached a point at the turn of the 21st century where the bulk of internal processes and external interactions of banks had become fully digitized. Today we witness:

- Electronic trading platforms that facilitate trades on capital markets in real time

- Mobile payment offerings which exchange funds have become commonplace as smartphone penetration reaches record levels around the world

- Robo-advising platforms that provide algorithmic-based portfolio recommendations, lowering costs and enhancing alpha through the automated analysis of enormous volumes of data

- Cloud-enabled CRMs that allow banks to monitor their relationships with clients, creating a stronger feedback loop which helps improve offerings

In short, great strides have been made to augment both top and bottom lines.

BUBBLING TENSIONS & BLOCKCHAINS

Interestingly, this has all occurred amidst the backdrop of increasing societal distrust of the financial system, particularly in the aftermath of the 2008 Global Financial Crisis. While consumers have definitely benefitted from these innovations, institutional players themselves have been the biggest winners from these developments.

For decades, this consortium of legacy players has served as the foundational layer of trust and been robust to external shocks. At the same time, the necessary existence of these intermediaries has allowed for significant rent extraction (for instance, on only 55-65% of insurance premiums typically go towards paying claims, while 45-35% is accrued to administrative costs and corporate profits)

While substantial profit margins are not inherently something to condemn, does intermediation in of itself still create value in line with broader economic growth and fair market evolution, especially now that technology is starting to remove its necessity?

In response to this sentiment, we are now witnessing a new paradigm within finance, one that synthesizes financial products with decentralized networks. Decentralization refers to ecosystems where administrative power is not concentrated in a single intermediary, but rather distributed across actors that are economically incented and cryptographically bound to cooperate harmoniously. Such a system of organization has gained immense popularity since the launch of Bitcoin in 2009 and the subsequent obsession with exploring the applicability of blockchain ledgering and other types of distributed ledger technologies (DLTs). In this model, software code seeks to become the new layer of foundational trust. This is manifested by immutable smart contracts verified and timestamped on a blockchain (a kind of distributed database that requires redundancies and the absence of a single central coordinator), such as Ethereum or EOS, that virtually anyone can create (with a little know-how) and no malicious actor can unilaterally appropriate (ideally). The promise of this disintermediation is vast indeed, as it implies two crucial elements:

1. The democratization of access as, anyone with an internet connection can access financial services regardless of the wealth, relationship, location, and other requirements typically imposed by intermediaries.

2. The security of trustless operations as blockchain-enabled transactions provide security and retain custodianship of user assets, without validation from a central party — a crucial feature for those living in areas of poor governance or under the duress of a surveillance state.

Why does it matter now?

INCLUSION & OPPORTUNITY

The extent of this rapidly materializing opportunity is apparent by the sheer multitude of people who currently exist either outside of or on the extreme periphery of the current global financial system:

- ~ 1.7 billion adults around the world (roughly a third, globally) have trivial to no access to formal financial services.

- The vast majority of the unbanked can be found in emerging markets

- This majorly comprises women and individuals from households ranking in the bottom 40% by income of their respective countries

- Often, these individuals tend to lack personal documentation and IDs that would allow them to engage with the current financial system (e.g. rural dwellers and migrant workers) which further perpetuates their condition of poverty

- Interestingly, this phenomenon is present even in high-income countries, like Singapore, for example, which sports an ID-less rate of an alarming 37%

Therefore, it is not a surprise that bringing the entire unbanked population into the fold of the existing formal financial system can generate an estimated whopping $380 billion in new revenues.

That being said, it is critical to note that the unbanked populace still leads an active financial life through informal financial services, such as the local pawn broker or village money lenders. Thus, the savviness and cognizance of financial wellness exists, at least latently. Furthermore, the expansion of brick and mortar infrastructure carries little economic feasibility in many of these geographies.

Consequently, pre-existing smartphone and internet connectivity now offers a unique avenue of entry for decentralized networks to reach the unbanked. Again, they are unbanked but not unaware. The informal economy is a testament to their understanding of the importance of financial wellness, as well as the roles and responsibilities of various parties in a transaction. Given that blockchain-ledgering can allow for the creation of digital identities, decentralized financial applications can begin catering to the needs of these 1+ billion people from the outset. They can keep costs low through the exclusion of expensive intermediaries and provide transaction security regardless of someone’s level of personal documentation.

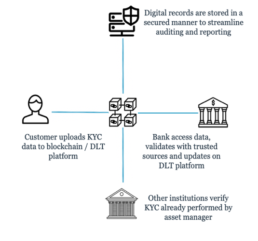

Figure 1: Illustration of identity creation and management on a DLT-powered platform that banks can tap into

Our prediction is that decentralized networks will capture much of the wealth generated as millions more are lifted out of poverty and subsistence living, as a result of macroeconomic factors and projected global economic growth in the decade to come. In fact, the global middle class is expected to increase 2.7 times from approximately 2 billion in 2009 to 5 billion in 2030, indicating a jump from $21 trillion to $56 trillion in global middle-class expenditure. As decentralized finance will be the beachhead infrastructure for those on the cusp of entering the middle class and the banked world, it will also be one of the primary arenas where this wealth accretion will occur. Players looking to move into the space now will be in a unique position then to capitalize on it. This will include new revenues through the provision of investment opportunities, lending options, insurance policies, and a whole host of financial products that become more relevant as disposable incomes increase.

Ultimately, by recognizing:

1. the unique trustless value proposition and digital reach decentralized finance has to offer, and

2. the sheer quantity of people who exist outside of formal finance but are financially aware, and

3. the projected explosion in the world-wide middle class

we can now appreciate the enormous and long-lasting social and economic dividends available through this radical inclusion enabled by decentralized finance.

What lies ahead?

A BRAVE NEW WORLD

Beyond pushing the boundaries of inclusion, the scope of what is considered a viable financial product is also rapidly broadening. Tokenization, the act of representing real world assets with tradable tokens generated on blockchain ledgers, will allow individuals to gain exposure to assets they were previously barred from, such as private equity or real estate, effectively increasing the liquidity and flexibility for owners.

Micropayments between parties that regularly transact with each other (like consumers tipping content creators) will become economically feasible by being conducted off-chain – without transaction-level validation on the blockchain – for speed and scalability while the beginning and end states of these interactions will be settled on-chain at regular intervals to ensure security (as we are witnessing with Bitcoin’s Lightning Network). Algorithmic stable coins, which leverage supply balancing techniques to maintain constant pricing equilibria, will serve as a dependable store of value for lending, salary payouts, remittance, trading strategies, and a host of other functions. Communal insurance policies can be formulated where surpluses are re-invested into the community, as dictated by smart contracts that are automatically executed when pre-determined conditions are met. Consequently, we can now picture scenarios such as:

- Shopkeepers of an ethnic neighborhood in Manhattan on the coast can create a communal flood insurance policy to safeguard century old businesses and retain the cultural heritage of their geography

- A Venezuelan family can store their wealth in digital money with programmed (as opposed to human-orchestrated) scarcity, like Bitcoin, to minimize exposure to the hyperinflation of the government-backed Bolívar

- Readers of a Sudanese political satirist can support her work through stable coin payments per view of publication

- An immigrant in the United States can send remittances back to family members in her country of origin without costly money transfer fees

- A middle-class individual in Pakistan can borrow from a Canadian lender to invest in a real estate development in Brazil in a frictionless manner

Figure 2: Selected list of popular types of DLT applications within financial services

The common motif that runs through these scenarios is that of self-empowerment. The next incarnation of finance will empower individuals by meeting their specific needs and narrow interests in a way that previously could not have been facilitated by intermediated finance due to a lack of economic incentive. Disintermediation, afforded by DLT-powered trustless environments, creates the demand for all sorts of niche services that decentralized networks and protocols can cater to and unlock previously untapped value from.

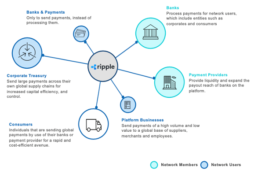

At the same time, corporations like banks stand to significantly benefit as well from decentralization-enabled advances in process streamlining. For example, Ripple, the blockchain-based payment protocol, is upending (among other things) traditional interbank transactions and rendering older infrastructure, like SWIFT, obsolete by allowing for virtual real-time settlement (two seconds in actuality) of global payments: a $2 trillion market that is poised for disruption through this radical efficiency. And while these revolutionary opportunities looming on the horizon are undoubtedly exciting and will transform conventional finance as we know it, the path ahead is not without its own unique set of intricate complexities and multi-faceted hurdles.

Figure 3: Mapping of Ripple’s value proposition and multi-faceted infrastructure revolutionizing payments

IMPENDING CHALLENGES

The underlying infrastructure of decentralized networks is still being built. Technical problems of scalability (featuring lively debates on which consensus algorithms are optimal, what constitutes the ideal mix between Proof-of-Stake and Proof-of-Work, the role of Layer 2 protocols, etc.) are just as present as (and to a great extent, intertwined with) issues of compliance with existing regulatory frameworks.

Different types of blockchains have differing takes on issues such as — how consensus verifying the integrity of data is to be achieved, how decentralized the decision-making process ought to be to achieve consensus, the respective decision-making abilities that should be delegated to different kinds of stakeholders, what sort of value can be tokenized, etc. The rules of consensus-making are both a function and a determinant of how scalability and reasonable throughput can be achieved across a blockchain.

This complexity is further compounded by differing regulatory requirements across jurisdictions and incongruent definitions of concepts, such as what constitutes a security, an investment contract, and AML/KYC compliance. This is why, as part of the infrastructural development and creation of enterprise standards, great attention is currently being given towards the interoperability of blockchains, bridging both technical and regulatory differences through modularity coupled with seamless integration.

A REAL (ESTATE) USE CASE

To further appreciate these challenges, let us examine an actual use case within decentralized finance. The tokenization of real estate is an apt utilization of DLT as it leverages the immutability of blockchain-ledgering and the programmable business logic of smart contracts. Such tokenization can enable secure fractional ownership of real estate assets, to improve market liquidity and generate efficiencies through transaction automation and speedier settlements.

For this to work in practice, the underlying blockchain platform must have the legal rights needed to store ownership information, transfer possession rights, and generate tokens representing the underlying ownership that can be redeemed for the appropriate value within a market. The tokenization and subsequent fractional selling of a property could be conducted in a manner deemed as a legal security offering in the EU, but illegal in China or the US. It is possible that the blockchain platform used can be compliant in one jurisdiction, but the property could be domiciled in a geography with a different regulatory regime altogether.

Furthermore, various tokens can be representative of different kinds of rights of the same underlying asset: tokens that allow for voting in governance decisions, equity tokens representing overall ownership, or specific claims tokens for mineral or water rights on a given property. This makes the formulation of business logic within smart contracts and the ability to conduct token-holder tracking, even across secondary markets, very critical.

Traditionally, the securitization of real estate has been chiefly done through Special Purpose Vehicles (SPVs) which levy fiduciary obligations and duties on the original asset owner. While tokenization has the potential to streamline this process, it is very likely that the creation of SPVs, which can be quite an involved process, will continue to be a reality for now. In fact, this underlying tension between new tactics and old understandings can be found throughout decentralized finance. The juxtaposition between novel methods of value creation with current compliance grounded within the intermediated finance paradigm requires a savvy approach to achieve economically beneficial harmonization.

The verdict

It is difficult to characterize this emerging phenomenon as anything other than exciting and brimming with opportunity. We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers change if they are to remain relevant in an era where trillions of dollars of value generation are up for the taking.

Starting Your Journey

Which decentralized finance use cases do you believe will provide the highest ROI for your organization? Tokenizing your illiquid asset holdings? ERC-20 tokens could be good fit but ERC-223 is making a name for itself as well. Launching your own cryptocurrency to improve the speed of cross-border transactions? Creating a crypto-compatible trading platform? Timestapping the movement of products across the supply chain on a blockchain ledger to provide you a more transparent view of your vendors and distributors? Which platform should you build off and partner with? IBM’s Hyperledger Fabric? R3’s Corda? Maybe creating a sidechain on Ethereum makes more sense? Perhaps you want to build your own blockchain, which opens a slew of questions related to crypto economics, consensus algorithms, byzantine fault tolerance methods, and degrees of permissioned-ness…

There is no one way or standard method of providing financial products through decentralized networks. At the same time, different use cases may be more profitable or desirable than others depending on the circumstances of your organization as well as your strategic vision. It is important for businesses to understand what they ought to prioritize through a rigorous cost-benefit analysis and opportunity sizing as well as determining what capabilities are required and how to attain them (build vs buy vs partner). The processes of transforming opportunities into pilots and then converting those into sustainable, commercialized intitiatives or conducting due diligence on existing providers and integrating their offerings into your own are not easy tasks. Benefit calculations must incorporate risks by developing a range of projected outcomes that are sensitive to potential deviations.

Amidst this realm of questions and uncertainty emerging from the paradigm of decentralization, a crucial fact sticks out: plowing ahead in this new domain will be critical in maintaining a competitive edge and unlocking novel avenues for value creation. Kepler Cannon looks forward to working with our clients and partners to jointly navigate the new way forward as finance continues to evolve and we find ourselves at this new frontier: one that is dramatically different but all too enticing not to dive in head-first.

Read More

Banking on You – Personalization in Financial Services

Capturing and sustaining attention is key to building customer loyalty, driving sales, and standing out in a competitive landscape. In this attention economy, what really helps business maintain relevance is to personalize the interactions for their needs, context and preferences.

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.