THE INNOVATION MANDATE

The word crisis has its origins in the Greek word ‘krisis’ – which means ‘decisive moment’ or ‘turning point’. History bears witness to the fact that crises have redefined many businesses. During the recessionary downturn of 2008, while many firms collapsed under the pressure of unpredictable and rapid change, there were several that emerged stronger than ever. The key differentiator for those who thrived post-crisis lay in their ability to innovate. Market capitalization of firms that embraced innovation outperformed competitors by 10% during the 2008 recession and 30%+ in post-crisis years.

Today, as we stand in the face of a historic economic disruption, 90%+ executives expect the fallout from C-19 to fundamentally change the way they do business over the next five years. Some known changes that are expected to last, include:

– Shifting customer preferences for low touch/ contactless offerings

– Slow-down in the adoption of ‘physically shared’ services

– Growth in hybrid/ omnichannel customer experiences

– Lower demand for non-essential products and services by customers most impacted by the pandemic

– Emergence of new competitors across industries with pandemic-ready business models

The impact of C-19 on business trajectory and customer disposition has a crucial role to play in shaping innovation going forward. Financial institutions have had innovation agendas for over a decade, driven by regulatory changes and competition from fintechs. However, past initiatives leave a lot to be desired. While only a few firms have incorporated innovation wholly as part of their business strategy, most have failed to embrace or seize its full potential, brushing it off as a ‘nice-to-have-capability’. Today, the radical changes brought forward by C-19 create an irrefutable case for firms to reinvent themselves in order to sustain and emerge stronger out of the pandemic. As Harriett Jackson once said, ‘Nothing is more expensive than a missed opportunity’, firms must capitalize on their chance to win by investing in innovation.

To truly unlock benefits of innovation and achieve transformative changes in the current scenario, business leaders need to look beyond their available resources and collaborate with the right set of external partners. Despite having R&D teams and dedicated internal personnel, firms can experience lackluster results when trying to innovate. On average, 3 out of 4 innovations fail to hit their profit and revenue goals due to the inability to commercialize and monetize ideas.2 Internal teams are hindered by a myopic view and need a better understanding of external environment and opportunities to steer themselves in the right direction. By leveraging outside help to tap into insightful pools of knowledge, businesses can foolproof their innovation plans.

HITTING THE BULL’S EYE

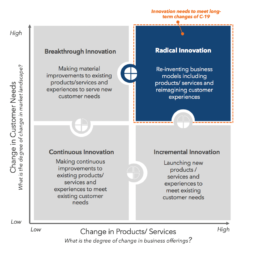

Before firms decide on specific areas to innovate, it is essential to zero in on the right strategy for driving change. Business leaders face a dilemma in identifying the right mix of growth opportunities. Investment dollars are limited, and there is immense pressure to make winning investments. Today, most firms find their customers demanding offerings and experiences significantly different from those in the pre-COVID era. To re-engage these customers and meet their altered preferences, focus should be on a complete reimagination of business models (see exhibit 1). A radical innovation strategy entails efforts that aim at revolutionizing business or its various segments, and can include the following:

– Develop products and services to meet evolving customer needs

– Change traditional ways of doing business to reposition firm in the competitive landscape

– Transform internal processes and strategies to support new business models

– Re-think customer experience to drive engagement and loyalty

In addition to choosing a broad governing strategy for innovation, devout attention should also be given to prioritize the right lines of business, customer segments, parts of the value chain and internal processes to gain the most from innovation.

Exhibit 1: Prioritizing Innovation Strategies

Some pertinent areas that can gain from radical innovation include:

Exhibit 2: Key Areas for Radical Innovation

Re-imagining Customer Experience

With restrictions on movement and fear of physical contact, many customers shifted to digital offerings in the early days of the lockdown – making their first-ever digital transactions. As more and more people become digital immigrants, businesses will need to rethink every customer interaction to sustain long-term loyalty.

Additionally, even as physical processes re-start post lockdown, there is a need to carefully craft purposeful and binge-worthy omnichannel experiences crucial to the new normal. For example, the China Merchants Bank added several non-banking functionalities, in addition to traditional financial services, to its mobile application during the lockdown. Food delivery, online courses and ridesharing services etc., were made available via the platform. Moreover, the app even provided real-time pandemic data, online counselling and a designated hospital search through partnerships with various third-party suppliers. The solution enhanced user experience by addressing serious concerns of users in the COVID era and garnered over 100M visits in just one month.

Redefining Products Portfolio

To keep up with the new needs and preferences of consumers, innovation must quickly permeate product and service development. Considerations regarding cost-effectiveness, social distancing, changing credit-worthiness, and digital affinity etc. must be front-and-center while designing future offerings. For example, Starling bank, a mobile-only bank based in UK, introduced a “connected card” that can be given by self-isolating customers to trusted parties to pay for essential items. Protected via a secure pin and a balance limit of 200 pounds, the card works like a transferable debit card that has eased concerns of self-isolating customers in procuring items without the hassle of dealing with cash, cheques and account numbers etc.

Reshaping Core Business Models

In this new environment, there is a lot of pressure on existing businesses to become resilient, responsive and future-proof. Outdated and traditional models of business need to be replaced and redesigned to adapt and thrive through the economic yoyo and realize post-pandemic opportunities. For example, in the new age of digital transformations and changing regulations, many banks are transitioning their core business models to adopt a banking-as-a-service approach. As a use case for this approach, Standard Chartered Bank’s Korean banking arm enabled ‘social banking’ to ingrain banking abilities into consumers’ keyboards. Through this new model, users can use their keyboards to access account balances and transact with different Korean banks without using traditional physical cards and heavy mobile apps for monetary exchanges.

Modernizing AI and Analytics Foundation

Firms can no longer rely on targeting customers and predicting their likely behavior based on historic performance. Similar to real-time logic in an in-flight missile, what happened in the last second (e.g. wind conditions) matters a lot more than the historic projectile or the launch location. As an initial step, firms must build an adaptive data foundation that enables quick experimentation with unconventional cross-sectional data (e.g. current infection rates, unemployment rates, layoffs, ride sharing volumes and routes).

With such a foundation, innovation efforts should then be directed to monetizing this data across a plethora of new use cases. For example, to keep up with C-19 induced changes in customer demand, several banks have started mining credit card transactions to determine changing consumer spending priorities. From tracking user life stages and geolocation to create appropriate loan products to combining social media data with internal data to draw insights, real-time information is building opportunities to innovate in the new normal.

BUILDING THE RIGHT CAPABILITY TO INNOVATE

Despite coherent ideas and prudent strategies, more efforts fail than prove to be useful, making innovation a far-fetched reality for many. In the 21st century, surrounded by a talented workforce and disruptive technologies, there is no dearth of creativity within firms. New ideas exist internally. However, roadblocks lie in the commercialization and monetization of these ideas. Simply put, great ideas are just as good as the ability to execute and deliver them. A few common obstacles to internal progress include:

Fear of the Unknown

While innovating beyond the purview of core products, many companies dabble with new business areas, different revenue models, uncommon product offerings, and unfamiliar regulatory considerations. These uncharted waters make it tough for internal teams to manoeuvre the innovation process, resulting in sub-optimum product and experience development that fails to achieve desirable results. For example, Google’s launch of Glass, one of its most ambitious tech products, received plenty of backlash, despite ranking high on the innovation scale. As Google tried to step beyond its area of expertise, flaws in product design, confusion related to usability and room for misuse for surreptitious recordings led to its failure and ultimate withdrawal from the market.

Limited or Late View into External Successes

Despite having fancy R&D labs and dedicated resources, it is not easy to keep up innovation efforts with the ever evolving needs of the market. Most internal teams are too invested in improving existing products and services that anything more radical often gets pushed to the back burner. Even when new opportunities present themselves, there is always a quandary in identifying the most profitable ideas. Afraid of failure and shifting strategic focus, firms lose out on monetizing the right prospects. For example, Kodak, the once leading film and photography behemoth failed to keep up with the digital revolution in fear of eating away at its strongest product lines. Even with the presence of the right opportunities to grow, decision makers couldn’t capitalize on them, eventually crumbling under intense competition.

Limited Customer Insight

Many times firms lose sight of the needs and wants of their end-users while vetting new ideas. In their quest to produce new products, they often kick-off development without identifying a genuine customer problem or the “job to be done”. Cramming products with many features, components and use-cases without addressing pressing customer requests is only a recipe for disaster. Even when customer suggestions are included, they are limited to end product/ service recommendations that don’t contribute much to creating ideal solutions. For example, when Amazon launched its ‘fire’ smartphone, it failed to make a recognizable dent in the market. Even with a sea of features installed in the product – 3-dimensional effects, one-minute response time for tech support and camera enabled shopping experience, the solution didn’t address any pressing consumer needs. It was just a tech wonder that wasn’t of much value to smartphone users, resulting in its early wipe-out.

Thus, enabling innovation internally is not without its challenges. Despite being one of the most preferred approaches to implement change, internal efforts fall short in delivering optimum results. Investment in R&D labs, intrapreneurial ventures and business development is an ongoing effort for most corporate mammoths. While these units guarantee the existence of dedicated resources to innovate, they are often hindered by a myopic view and limited focus, creating the need to supplement existing efforts.

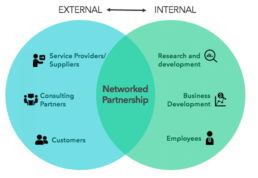

A networked model of co-creation can be adopted to add to the efforts of internal teams. (see exhibit 3). By combining the best of internal and external resources to fill in gaps and streamline processes, co-partnered innovation can significantly improve a firm’s innovation process.

Internal teams can contribute their expertise by leveraging in-house processes, capabilities, technologies and other resources. External outfits like suppliers and consultants, on the other hand, can offer well rounded support through their experience and knowledge of the client’s industry. Additionally, even consumers can aid the innovation process by representing demand for new products and solutions. Thus, this interconnected web of ideas and resources with different origins can accelerate and augment existing efforts in deploying successful innovation.

Exhibit 3: Collaborative model of innovation

ROADMAP TO INNOVATION

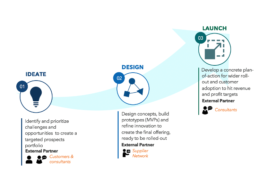

For a collaborative approach to work its magic on a firm’s innovation lifecycle, supplemental efforts of 3rd parties must be ingrained into the innovation process, including: (see exhibit 4)

Ideate

The first step involves creating a portfolio of ideal innovation prospects that have a higher chance of being accepted and generating substantial growth. Internal teams understand the need to develop ideas from a customer-centric lens but very few are able to capture the right input. By asking end-users about product/ service recommendations, when most lack the technical expertise required in development, firms set themselves up for an innovation failure. Thus, there is a need to involve customers the right way by asking them of outcomes they desire from innovation.

Exhibit 4: Leveraging external partners for innovation

For example, for a retail bank, customer input about reducing visits to the bank can be more helpful in innovating as opposed to receiving suggestions for developing a specific kind of digital app.

Additionally, external consulting expertise can also help firms scan the market to identify and size the most rewarding opportunities. They can leverage high levels of knowledge about the client’s core and adjacent industries’ to provide a fresh look at a company’s innovation portfolio.

Moreover, by virtue of not being a part of the client’s closed network, they are even without cognitive biases. Thus, they serve as a useful resource in kick-starting innovation efforts.

Design

Once the right ideas have been shortlisted and prioritized, innovation teams can design prototypes and develop final offerings. However, assessing and producing commercially and technologically feasible solutions requires agile cross-functional resourcing – both physical and mental. Especially when working with newer ideas and technologies where firms may not have prior experience, meeting innovation goals is usually a futile effort. External support in the form of existing suppliers and partners can offer much needed assistance in guiding and accelerating efforts for building solutions. Joining hands with suppliers, companies can commercialize ideas 40% faster than internal innovation efforts.3 In fact, it is ironic that despite having thousands of suppliers, most firms have no formal or proactive way to tap into this indispensable ecosystem. In addition to providing mental horsepower, suppliers even provide the added benefit of disseminating cost and risks amongst multiple stakeholders, preventing firms from slouching under a massive innovation expenses. Their in-depth familiarity across the silos in the client’s business and the existence of pre-made collaboration mechanisms help input valuable suggestions that may be missed by internal teams.

To leverage relationships with suppliers, it is necessary to scout worthy partners. Modern procurement teams/ external parties such as consulting firms can play an essential role in identifying the right suppliers by acting as ‘innovation scouts’. These stakeholders help firms collaborate with both existing and new vendors. In fact, to truly augment internal capabilities, firms must continuously appraise a broad pool of potential partners without limiting focus to a select few candidates.

Lastly, for delivering successful innovation via the supplier network, it is crucial to to ensure strong alignment of goals, objectives and outcomes:

- Screen suppliers based on their collaborative ability including technological, quality, and industrial skills as well as strategic alignment around product/ service goals

- Agree on the ownership of intellectual property rights and risk sharing via dedicated contracts that sets the rules of collaboration

- Ensure supplier deliverables include insights from innovation investments made by other industry leaders

Launch

Post production and refinement, innovation units need to hinge upon developing the entire go-to-market plan for encouraging adoption across the usage ecosystem. The roll-out strategy is the ultimate test of the innovation process, as poor execution can render efforts useless. For example, when Sony launched its e-reader, a mighty technological advancement, loopholes in the channel distribution strategy were partly responsible for the product’s inability to create the buzz it anticipated. Despite readers being the targeted audience for its invention, the product was made available at big technology selling stores instead of channels that book-readers most preferred. Such mistakes, though seemingly small, can turn into a hefty price for firms to pay.

Based on inputs of 164 executives across companies with more than $1 billion in revenue, 26% of respondents believe that the transition from innovation or R&D groups to the business unit “needs serious work” at their company4. External partners like business transformation consulting firms can come in handy to define and navigate the strategy for monetizing offerings; their expertise and experience of dealing with diverse industries and stakeholders makes them ideal for driving alignment between teams and transforming operating models to make revenue and profit goals achievable.

Some areas that they can help with, include:

- Designing optimum pricing models for new offerings based on a firm’s strategic vision, competitor intelligence and customer’s willingness and ability to pay.

- Coordinating efforts between siloed and disconnected teams including R&D and sales and marketing etc. to build a holistic go-to-market plan.

- Designing and conducting quick-speed pilots for rapid learning

- Enhancing customer-centricity of new innovations through customized strategies and experience design to meet the right customer segments through the right channels.

- Positioning new offerings in line with the firm’s existing solutions to drive growth and create a positive impact for the overall business.

- Ensuring P&L benefits are proactively monitored and captured

IN CLOSING…

The business world has been upended due to the pandemic. While most firms have fared through the initial impact by making tweaks in their operations, long term success will require dedicated commitments to change. To cater to new customer demands and altered market dynamics, businesses need to innovate radically and proactively to reinvent and transform themselves completely. From rethinking customer journeys and business models to recreating their products portfolio, investment in the right set of ideas is critical for success.

As firms engage in their strategy of choice, they need to leverage external partners to bolster internal efforts and minimize chances of failure. Especially when it comes to monetizing and commercializing ideas, working hand-in-hand with 3rd parties like suppliers and business transformation consultants can help convert mere ideas into sought after solutions.

The push to innovate has never never been felt as strongly as today. Despite being in vogue for over a decade, the true essence of innovation is now to be realized. As Steve Jobs once said ‘Innovation is the only way to win’; firms that embrace this phenomenon will distinguish themselves as clear winners in the COVID era.

Read More

Banking on You – Personalization in Financial Services

Capturing and sustaining attention is key to building customer loyalty, driving sales, and standing out in a competitive landscape. In this attention economy, what really helps business maintain relevance is to personalize the interactions for their needs, context and preferences.

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.