Introduction

90% of businesses say their industry has become more competitive in the last three years (1)

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

As it is rightly said – It is easier to fight the enemy you know than one you don’t. Yet, companies find it challenging to take on familiar opponents, whose ambitions, strategies, weaknesses, and strengths resemble their own.

Business leaders should compare their game plans and prowess by closely anticipating competitor moves, value proposition, pricing strategies, product bundling etc. with their doppelgängers and later, investigate indirect and surging competitors to develop an informed and proactive plan to protect and gain their “size of the pie”.

In this paper, we share the need for insightful and actionable competitive intelligence, where firms usually go wrong, and how to successfully gather & leverage competitor intelligence to win in the marketplace!

Exhibit 1. Reasons for Increasing Competition

Competitors cannot be taken lightly

Competition has grown rapidly, especially in the Financial Services, Information Technology, Healthcare, and Retail sectors, as these industries are evolving rapidly and are being constantly fueled by Private Equity and Venture Capital firms.

1. Blurring Industry Boundaries

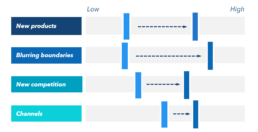

Although never a straightforward task, ‘drawing of lines’ between industries is becoming even more difficult today as ecosystems have become fluid and porous, operating across verticals and channels. Platform companies like Amazon, Google, Netflix, and Uber disrupted multiple industry verticals and began breaking down the boundaries with their innovative business models, products, services and channels.

With Apple’s recent entry into consumer credit through its partnership with Goldman Sachs (having issued roughly $10B in credit to card holders)(2) and Barclays teaming up invoice insurance provider Nimbla in the UK to offer its small-business customers access to insurance for individual invoices (3), it seems that large firms are making significant moves into previously uncharted industries.

Such partnerships — focusing on payments, mortgages, P&C insurance, brokerage services, and investment products — generated more than $70B in revenues in the U.S. alone in 20194. Similar partnerships are likely to disrupt the industry ever so more in near future.

Exhibit 2. Future Trends in Market Boundaries (5)

2. Shrinking Product and Company Lifespans

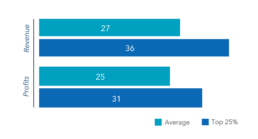

Long-term product ‘cash cows’, which stay in a company’s portfolio for several years, are becoming a thing of the past.(6) Today, a significantly larger share of a typical company’s revenue, is derived from new products and enhancements launched within the past three years (see Exhibit 3). The collapse of this lifespan has led to the norm of upgrading products and services every few years — otherwise, risking being surpassed by competitors.

The need of the hour is for firms to not rely on “too big to fail” ideology. The harsh reality is that 75% of the S&P 500 companies are likely to disappear by 2027, (7) and the biggest reasons for this are their inefficiency in managing themselves and serving their clients.

3. Rising M&A and VC/ PE Investments

Financial services deals in Private Equity have grown on the back of strong returns, including a multiple of 2.2x of invested capital in recent years (8). With Stripe raising $600M at a $36B valuation from VC valuations, and Intuit acquiring Credit Karma at $8.1B , the industry appears to be growing more rapidly than ever. (9)

With such deep pockets, business expertise, guidance, consultancy, and industry connections behind them, the smaller niche firms are able to accelerate at faster rates.

Exhibit 3. Contribution from products launched in past 3 years (10)

Exhibit 4. Average Company Lifespan (11)

The Need for Intelligence

Today, 87%+ of organizations are classified as having low business intelligence and analytics maturity. (12) In our experience, this is driven by the following reasons:

1. Monitoring is not ‘Intelligence’

The biggest misconception about competitive intelligence is the assumption that it is ‘information’ about competitors. Tracking tactical marketing/product information and press releases does not offer the full benefit of competitor intelligence.

One previously successful company that fell victim to inadequate intelligence is Nokia, the global leader in mobile phones in the late 1990s and early 2000s. With the arrival of the Internet, it was clear to other mobile operators how data, not voice, was the future of communication. However, Nokia continued to focus on hardware and not profit from the drastic change in user experience. In 2008, Nokia finally made the decision to compete with Android, but it was too late. Its products weren’t competitive, leading it to Nokia losing its prime position in the market space.

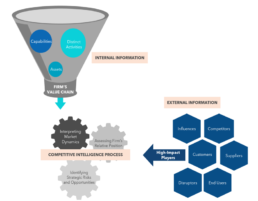

Exhibit 5 below depicts our recommended approach to distilling competitive intelligence.

The most essential part of competitive intelligence is to separate signal from noise, distil the plethora of information to insights, and then incorporate it into your go-to-market and functional strategies.

Exhibit 5. Recommended Competitive Intelligence process

2. Shaping your Strategy

Market research alone is $20 billion industry. Specific competitor information is another $2 billion (13). The paradox is that companies spend millions acquiring competitive or market “intelligence” but never question or re-visit the actual use of this information in branding, product, R&D, marketing, sales, purchasing or any other function. Executive management implicitly assume the information is being used effectively.

Personalization and timeliness are key to making competitor intelligence valuable. Ideally, 15-20% of the time is spent in planning, 30-35% in the actual gathering intelligence, and ~50% in the personalization (see Exhibit 6 for the distinct needs of each function), synthesis and strategy development.

Exhibit 6. Valuable Intelligence for each Business Function

3. The Right Stuff

Competitive research continues to be extremely time-consuming. Most researchers struggle for the following reasons:

- Inadequate questioning-

Several researchers limit themselves to what they read in the public domain and through marketing/PR updates from competitors. On the surface, most of this can sound like business as usual but everything requires vetting, triangulation and distillation. The age old technique of asking the ‘5 Whys’ can often uncover the motivations and strategies behind these events. - Information overload vs. relevance-

Due to limited time and plethora of publicly available information, firms often depend on industry reports. However, these are often high-level and not bespoke enough to be actionable. They are also usually not insightful, after-the-fact, and may have a myopic view of the competition. - Personal bias-

Often, market research teams may omit information that does not support their views, knowledge base and beliefs, thereby making the entire process misleading. Rather than being omitted, such information should be further vetted for insights.

Exhibit 7. Is your Competitive Intelligence Process efficient?

What is Your Maturity Level?

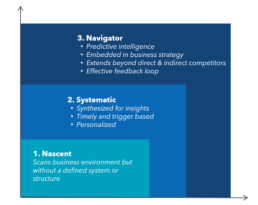

Exhibit 8. Maturity of Competitive Intelligence Capability

Level 1. Nascent

For more than 30 years, most large corporations worldwide have adopted competitive intelligence as a way to expedite good decisions; yet only 50% of them actually use the intel they collect (14).

Firms with nascent capabilities scan the competitive environment regularly, but without any defined system or structure in place. Market research may or may not be personalized for the various user groups and may or may not be leveraged by these user groups to ‘tune’ their strategies. The likely implications of events unfolding in the market may not be self-evident. Most of such research is focused on direct competitors and based on publicly available information only.

This situation often leads to spreading skewed information across the enterprise, with moments of inspiration followed by long periods of blind-sightedness.

Level 2. Systematic

Firms at this stage have all the relevant intelligence from both internal and external sources, including customers, salesforce, product team, industry SMEs, public sources etc. This includes analyzing ‘lost deals’ for competitive insights.

A 360 degree deep-dive into competitor pricing, proposition, products, marketing and customer support, helps develop targeted go-to-market strategies, product roadmaps, acquisition strategies etc., needed to outmaneuver the competition.

Deploying a unified intelligence system that integrates intelligence from multiple sources, synthesizes for insights, and then disseminates strategic recommendations in a contextualized way to various user groups, is the key to success for firms at this maturity level.

Corroborating and contextualizing this competitive intelligence is critical in ensuring that the findings are understood well and taken seriously.

Level 3. Navigator

At this stage, the firms not only use competitive intelligence to plan their next steps but also are able to use them to accurately predict the next steps of their competitors and market at large.

The competitive intelligence process is now tightly embedded in pressure testing existing strategies and defining new ones. In addition, there are ongoing alerts and a strong feedback loop based on successes/failures in the marketplace and experiences in the field. These trigger points are then used to take investment decisions.

By being the navigator, competitor intelligence also provides a comprehensive view of the competitive landscape – direct, indirect, aspirational, and even emerging competitors, which in turn helps in enabling strategic scenario analyses.

In Closing...

Making strategic decisions without insightful competitive intelligence is like flying a plane without a radar — You might eventually reach the destination, but it will take a while and you may bump into a few planes enroute.

Though in existence since the 1970s, Competitive Intelligence is still an area that most large corporations fail to succeed in, incorporate in their routine functioning, and leverage their resources completely, thereby hampering their position as market leaders.

A prognostic intelligence process, undertaken/ established by experts, that is seamlessly ingrained in the firm and that helps to keep tabs on all competitors (existing and imminent) and timely communicate strategies and intel to target groups while collating both internal and external data is the recipe to win in the mature markets!

__________________________________________________________________________________________________________

- “State of Competitive Intelligence Report”, Crayon 2020

- “If Tim Cook won’t tell the world how the Apple Card is doing, I will”, Ron Shevlin, March 2020

- Barclays Press Release, January 2020

- “For financial-services firms, inter-industry partnerships are pathways to growth”, Strategy+ business, October 2021

- “Future Trends: Looking Back and Leaping Forward”, Majesco, December 2019; Kepler Cannon Analysis

- “The product life cycle is in decline”, Freddie Pierce, May 2020

- “Why you will probably live longer than most big companies”, IMD.org, December 2016

- CEPRES Platform 2015

- 9 big things: Fintech unicorns find pandemic funding, Kevin Dowd, April 2020

- “New Product Development: Process Benchmarks and Performance Metrics”, APQC and PDI, 2011

- S&P 500 data sources

- Gartner Data & Analytics Summit 2019

- “Companies collect Competitive Intelligence, but don’t use it”, Benjamin Gilad, 2015

- “Only half of the companies actually use the competitive intelligence they collect”, HBR, January 2016

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.