Introduction

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry. With wealth solutions traditionally designed for High Net Worth Individuals (HNWIs), wealth managers in Asia have yet to develop successful strategies tailored to the specific needs of the mass affluent segment. To be successful in this market, it is no longer sufficient to have the best ‘product’ but also the organizational capability to deliver tailored solutions that seamlessly blend products, services, and a signature customer experience into solutions that are tailored to meet customer needs.

The Opportunity

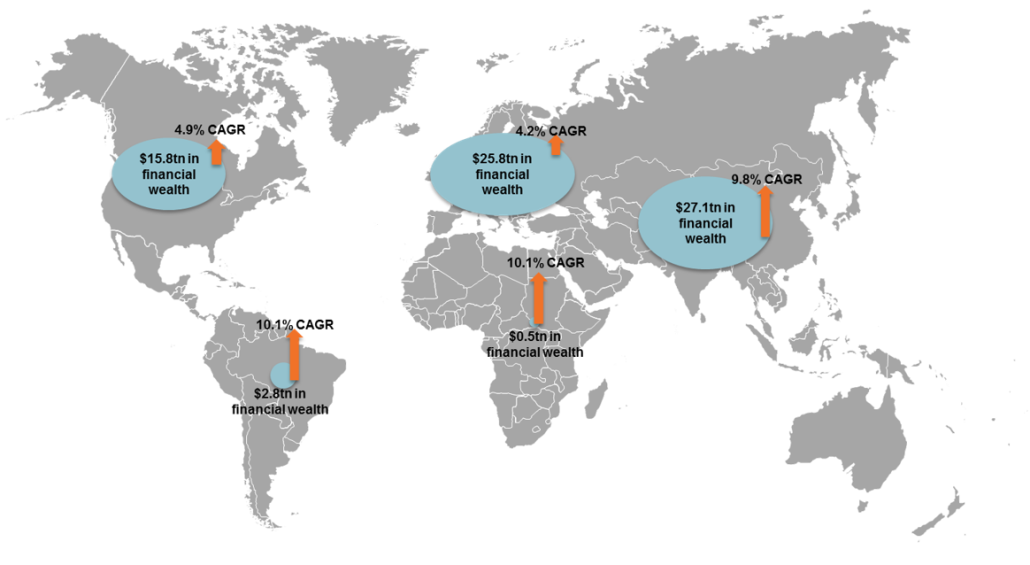

With $47.3 Trillion in private wealth, Asia holds the second largest concentration of wealth in the world, behind only North America’s $50.8 Trillion. Over the next five years, Asia is poised to usurp North America’s number one spot with an accumulation of $70.7 Trillion in private wealth [BCG, Winning the Growth Game, 2015]. Despite the region’s large share of wealth, wealth management firms have captured very few of these assets as investors tend to hold large portions of wealth in cash and deposits. As their wealth grows, investors will have increasingly complex needs and greater desires for professional help presenting an opportunity for wealth managers to capture new customers and larger wallet shares.

Many managers are already focused on the large opportunity in APAC, but most target the HNW while neglecting the fastest growing wealth segment in Asia: the mass affluent. With approximately $27.1tn in assets today and a 9.8% annual CAGR, the mass affluent are on track to hold $43.3tn in assets by 2020, far outpacing in size and growth the wealth of their HNW counterparts. Targeting this segment, however, is tricky. Wealth managers cannot just replicate traditional approaches used in Western markets. A tailored strategy is required to address and meet the unique needs and preferences of these local markets.

Exhibit 1: Global Mass Affluent Financial Wealth

In addition, this large pool of assets is even more attractive to wealth managers given over 38% of mass affluent investors in Asia do not receive any financial advice at all today, and an overwhelming portion of their assets are held in cash (with estimates ranging from 20-35% across the region).

"With $47.3 Trillion in private wealth, Asia holds the second largest concentration of wealth in the world, behind only North America’s $50.8 Trillion. Over the next five years, Asia is poised to usurp North America’s number one spot with an accumulation of $70.7 Trillion in private wealth."

Yet, there are many key challenges and nuances to overcome in capturing this market:

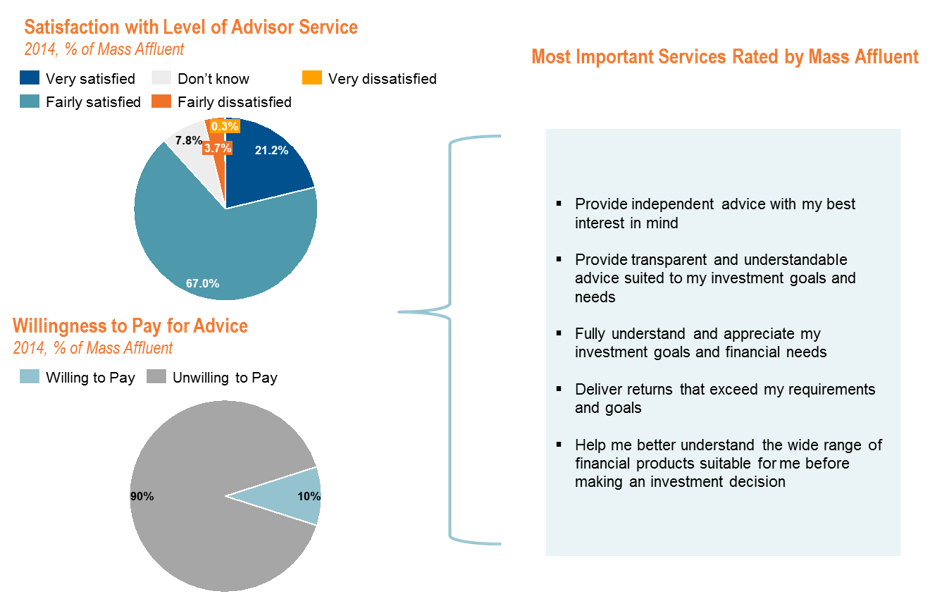

- Asian investors are unaccustomed to paying for advice. In fact, fewer than 10% of mass-affluent investors are willing to pay explicit advisory fees. While stricter regulation regarding fee transparency has made hiding fees more difficult, the mass affluent still expect full-service advice at little to no cost.

- Despite having a large concentration of investible cash, cultural norms for maintaining cash require further education of the mass affluent customer to help maximize returns while achieving their liquidity objectives.

- The majority of investors are happy with their current advisor. Of the 63% of mass affluent investors with an advisor, most of them are highly satisfied. Only by offering more personalized and proactive advice can wealth managers convince satisfied customers to consider working with another advisor.

Exhibit 2: Key Trends in Financial Advice [Cerulli Asia Investor Segmentation, 2014]

Despite the Asian mass affluent market being ripe with opportunity, wealth managers will need to to differentiate and maintain a tangible competitive advantage to overcome these challenges and deliver on the holistic, personalized financial advice that is desired by customers. This will require a cohesive strategy that aligns solutions, technology, talent, and organizational structure. As such, Kepler Cannon has identified four key enablers that are necessary in capturing the demand in this market:

A tailor-made solution set addressing the needs of the mass-affluent

Technology enablement of financial planning

A re-trained, upskilled advisor force

A customer-centric organization

A TAILOR-MADE SOLUTION SET

Traditional wealth offerings fail the mass affluent who are unable to meet minimums for HNW products, yet require more holistic and personalized offerings than are typically available to retail customers. Lack of knowledge, understanding, and confidence in investment vehicles are listed as primary reasons that mass affluent investors avoid certain investments5. As such, the element of simplicity is important for encouraging mass affluent investment.

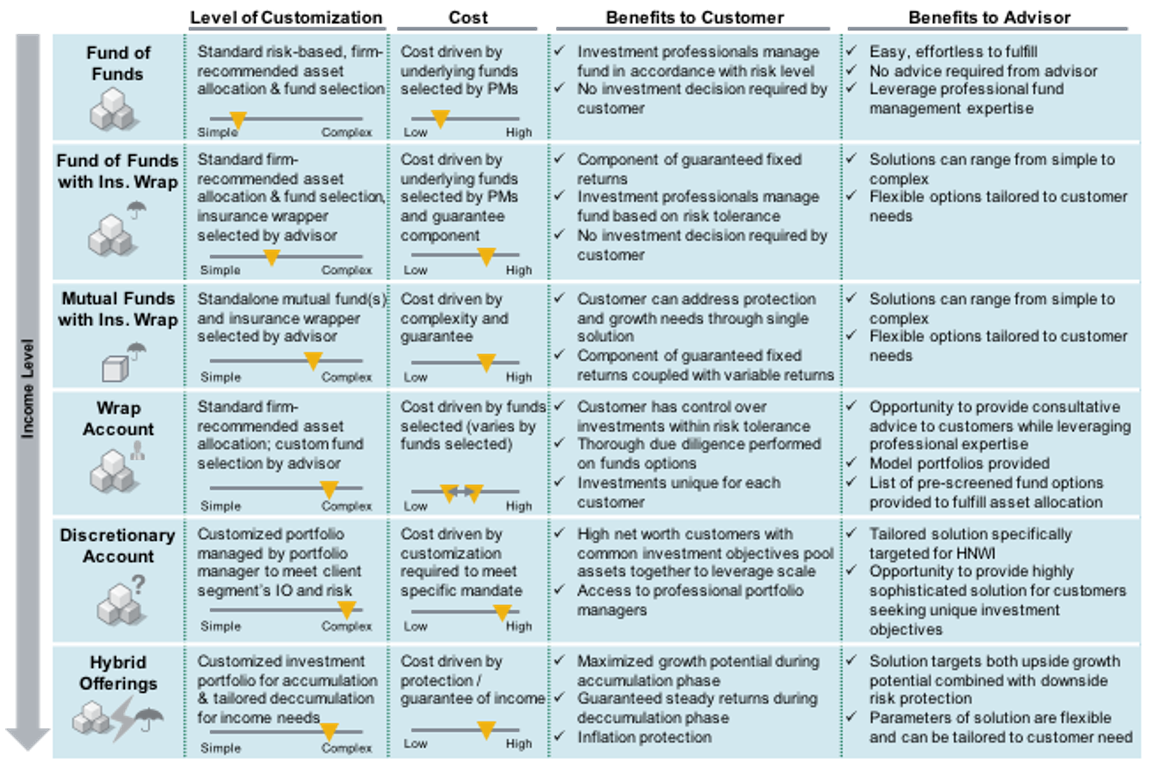

At the core of any wealth management solution is the underlying product. Simple products designed to meet specified levels of risk/reward based on Modern Portfolio Theory are easier to explain to investors and abstract them from the details of execution. These solutions can come in multiple product formats such as mutual funds, FOFs, wrap accounts, discretionary accounts, etc. These solutions need to be designed to meet various client needs within each wealth manager’s customer base to address desire for customization, cost sensitivity, and total investible assets.

Exhibit 3: Spectrum of Wealth Offerings by Client Need

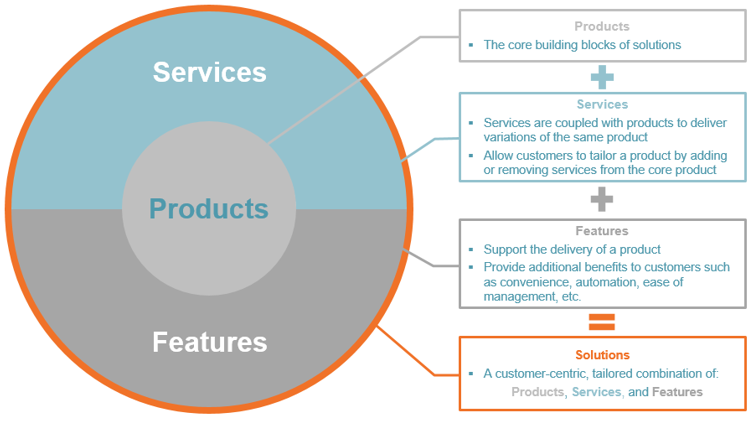

While any wealth manager can offer these products, real differentiation comes from how products are packaged with services and features for a truly unique offering. Will goal-based planning be part of the sales process? Can you offer combined investment and banking services from the same account? Are investments auto-rebalanced? Is there a component of self-directed investing (which is important to many Asian investors)? Depending on the needs of the target customer base, a thoughtful set of products, services, and features can be combined to offer truly holistic, customer-oriented solutions.

Exhibit 4: Developing Solution

Ensuring your solutions address all or the majority of customers’ needs allows for more holistic servicing of customers. It also allows wealth managers to become a trusted advisor, not just a distributer of product, leading to longer-lasting, more substantial relationships with a higher share of wallet.

TECHNOLOGY-ENABLEMENT OF THE MASS AFFLUENT

The Asian mass affluent are highly tech-savvy, driven by the youth of the segment6 with high rates of tablet and cellphone usage. There is not only an expectation for digital tools when investing but a preference for it. Mass affluent investing behavior is directly influenced by the availability, speed, and convenience of digital interactions with wealth managers. This segment turns to online solutions for a variety of traditionally ‘advisor’ led tasks:

- Brushing up on financial knowledge

- Purchasing mutual funds (ease of buying and selling is a top 5 consideration)

- Buying products not offered through their primary advisor

- Monitoring performance and holdings (checking via customer portals at least once a month)

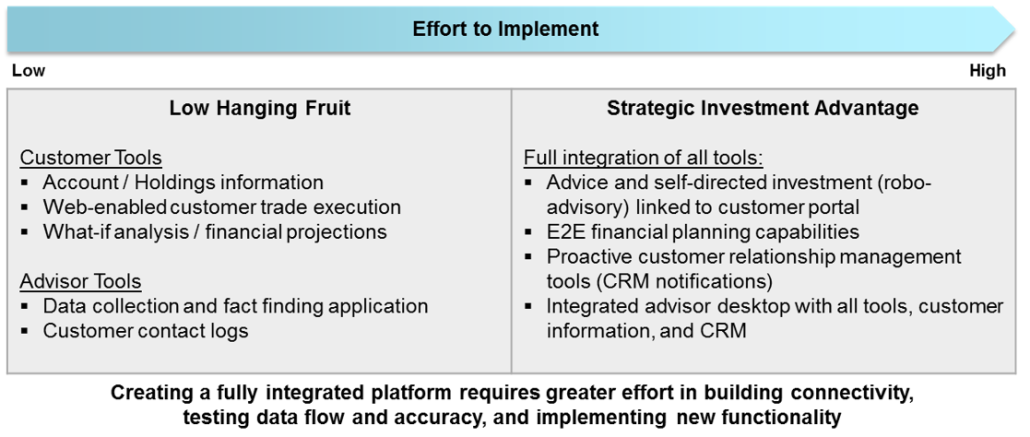

As such, wealth managers must consider both advisor and customer facing platforms that integrate to deliver a seamless customer experience. To create such a platform, senior management must dedicate resources, time, and money to the design and implementation of a digital strategy. As with any technological implementation, challenges such as cost, competing priorities, integration with legacy systems, and speed of technological advances constrain the scope and realization of benefits. Prioritizing quick wins and focusing on building a core offering that can be built out flexibly over time rather than aiming for a complete one-time overhaul is an ideal that many organizations aim for but find difficult to achieve. Identifying the low-hanging fruit and prioritizing delivery in a methodical way is critical.

Exhibit 5: Prioritizing Technology Delivery

There are also a few unique considerations to plan for while designing a digital strategy for the mass affluent in Asia:

- Tools for on-the-go and in the office. Regardless of location, tools need to be able to perform basic functions such as data collection and scenario forecasting based on input data. As advisors often travel to meet clients in their homes and other locations, internet connectivity can be unreliable, so tools should be designed to function well both online and offline.

- Respecting customer privacy needs. Asian consumers are often hesitant to provide their full financial history to advisors. When designing a workflow for any data collection, information collection should be expected to be piecemeal and iterative, allowing advisors or customers to continue to add information to their plan or profile over time. A significant amount of effort must be taken in designing simple, easy-to-use workflows that can accommodate this challenge of limited information while still producing value-add, customized financial advice.

Up-skilled Advisor Force

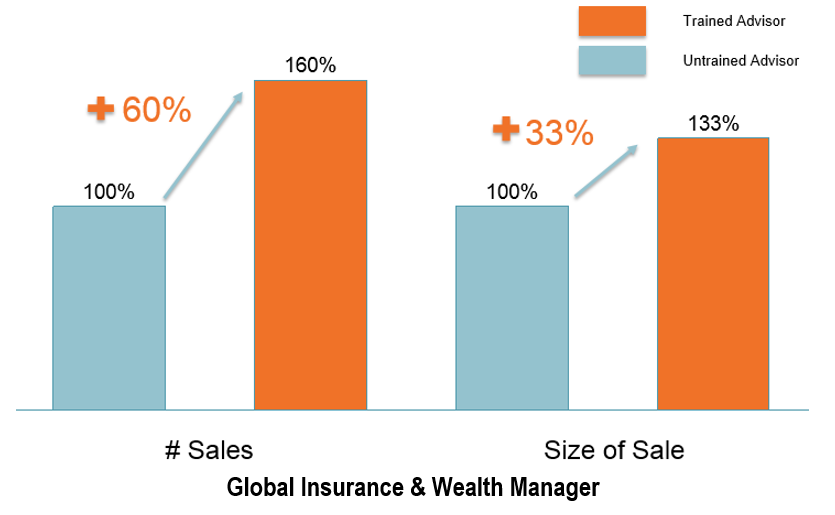

While technology is playing an increasingly larger role in investing, advisors are still at the center of providing financial advice. Current advisor forces are typically product-oriented and focused on selling individual offerings based on client demand. To attract mass affluent customers looking for proactive, personalized advice, advisors will need to begin to differentiate themselves by introducing a more holistic, financial planning oriented approach. For wealth managers that have shifted to this approach, the results are dramatic. The number of sales advisors make typically rose by 60%, with the average size of a sale increasing by 33%.

Unfortunately, this is not as easy as providing advisors with the right tools and solutions. Besides having the appropriate licensing and certifications, an advisor force that is expected to offer holistic, personalized financial planning requires a different skillset, deeper knowledge, and a more long-term, relationship-oriented view. Furthermore, with many advisor forces experiencing significant turnover, it can be difficult to develop meaningful, long-term relationships with customers. There are three key aspects of building and maintaining an advisor force that can serve the needs of the mass affluent:

Exhibit 6: The Value in Upskilling Advisors to be Financial Planners

a. Recruiting the Right Talent: Building the right team means knowing where to recruit, through what channels, and how to market the career opportunities offered. Agency leaders must determine the skills they most desire in their agents, and establish clear guidelines – as well as extensive testing – for assessing candidates along those criteria. With an Asian mass affluent segment hesitant to share personal financial information, the ability of a prospect to build rapport is paramount to perhaps all other considerations. Taking the time and attention to find agents not only with financial knowledge, but with excellent communication skills, confidence in interactions, and motivational drive, will pay great dividends in the long run.

b. Training Financial Planners: While an advisor will not be as knowledgeable or experienced as a product specialist, their education is vital to ensuring that the mass affluent receive quality advice. The task is tall and comprehensiveness is key, with topics ranging from general financial knowledge and the local market, to specific product details, and licensing exam preparation. But the most important component of all is teaching both incoming and existing advisors the financial planning process, and how to serve clients holistically, based on their individual needs and priorities. As demonstrated by Exhibit 7, the successful development of a training platform based around holistic financial planning may be the most decisive element of delivering on the promise and opportunity of a customer-centric offering.

c. Providing Support: With more holistic and tailored solutions, it often becomes more challenging for advisors to be the ‘expert’ on all offerings. While advisors will always be the central point of contact for clients, providing access to product specialists that can support advisors behind the scenes or in sales meetings to answer in depth questions related to specific solutions is critical. Furthermore, ensuring advisors are kept abreast of market updates, solution changes, and new offerings allows advisors to remain at the cutting edge in serving client needs. Firms can do this through a combination of providing continuing training as well as requiring outside continuing education and licensing. Being an advisor should be a career of life-long learning and evolution to meet the evet changing needs of customers and adapt to the market and environment at hand.

DESIGNING A CUSTOMER-CENTRIC SOLUTION SET

The design of a targeted solution set, structure of the advisor force, and investment in technology are all necessary components of a customer-based organizational realignment. However, the structural and cultural transformation that enables delivery of the right organizational structure and support is the lynchpin bringing all of this together. Only through creating a sustainable model of listening, adapting, and executing can organizations continually anticipate and meet customer needs and expectations:

A. Becoming an ‘Experience’ Brand, not a Product Company

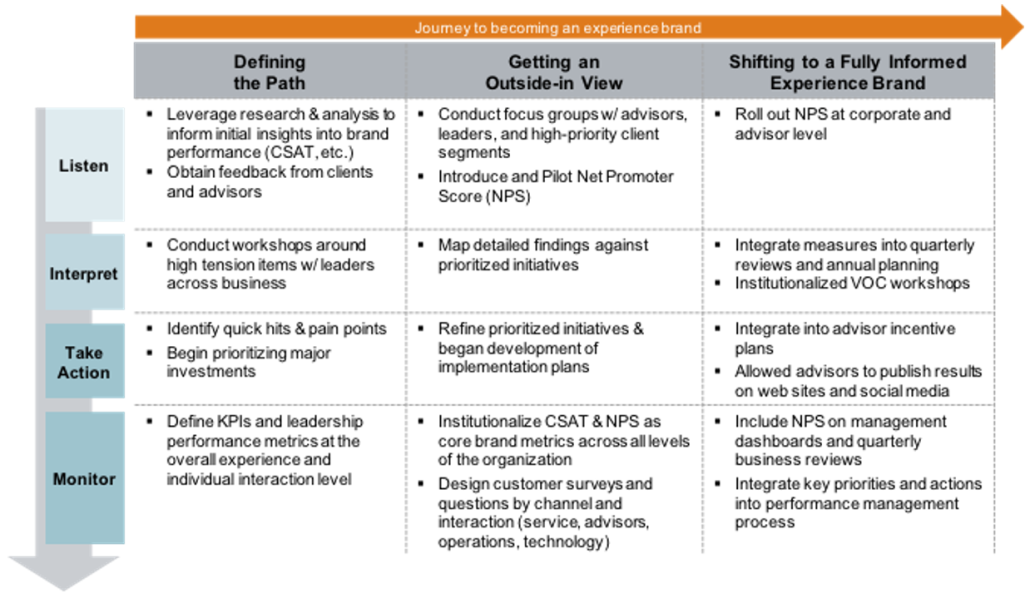

To stand out and differentiate against competitors, Wealth Managers will need to think beyond solutions and products to deliver a unique, highly customer-centric experience. Competing on product and financial performance is not sufficient to build allegiances and deep relationships with customers. Introducing concepts like Net Promoter Score, which has been traditionally used in other service and product-oriented businesses to gauge customer brand engagement and satisfaction is a powerful yet simple way to galvanize organizational behavior.

Furthermore, compensation and incentive structures also need to align advisor behavior with the best interest of customers. Whereas traditional incentive structures are focused on maximizing sales volumes, this new paradigm needs to reward advisors for building lasting, deeper relationships. This journey of becoming an experience brand is challenging, and organizations need to plan for how they can build to this goal over time.

Exhibit 7: Becoming an Experience Brand

B. Enabling Customer Centricity Through Financial Planning

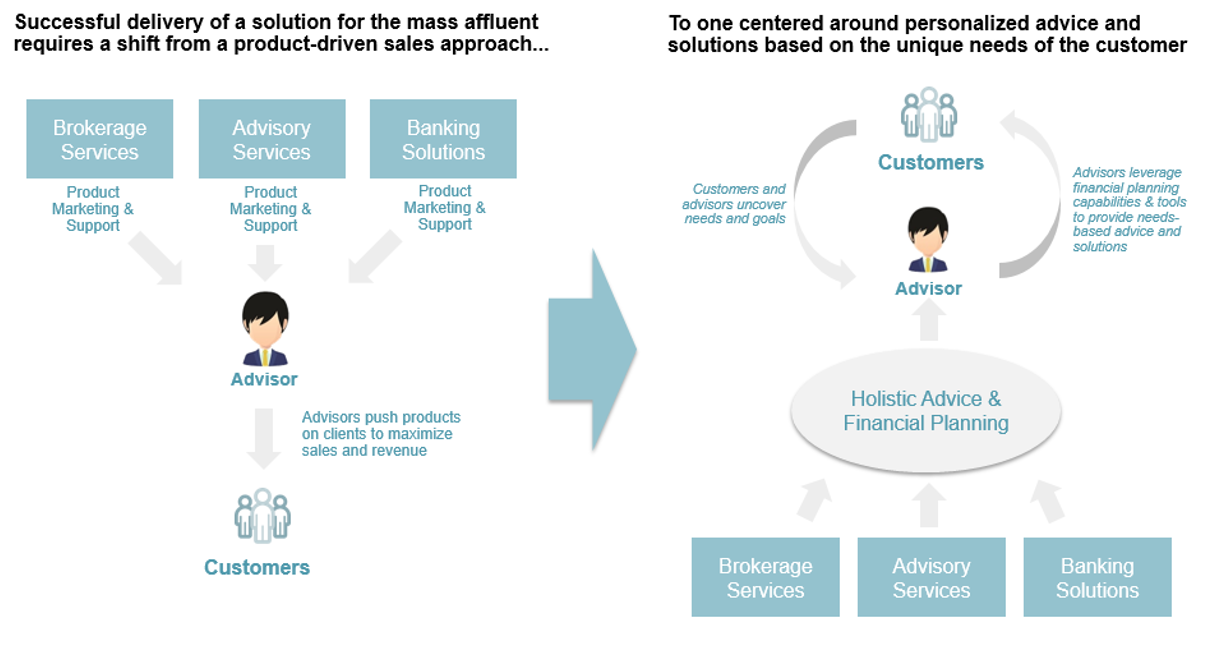

When selling holistic advice and solutions to a customer, products and offerings will need to work together to meet customer needs. To this end, a centralized Financial Planning function that can bring together all firm solutions and offerings to deliver a unified client experience in a seamless and simple way is a necessity. The role of a Financial Planning function is to work with individual product areas to ensure a seamless array of offerings that are directly targeted at addressing the full gamut of client needs. It can also serve as the coordinator in delivering new technology solutions that facilitate financial planning and needs-based selling in a product-agnostic way.

Exhibit 8: Shifting to a Customer-Centric Model

Conclusion

There is a tremendous opportunity to capture the mass affluent investments market in Asia. Organizations need to be prepared and enabled to differentiate themselves from other wealth managers to deliver a truly unique and compelling value proposition in a sustainable way. More than developing a core strategy and action plan to capture more share of wallet from existing mass affluent customers and to attract new ones, a shift in organizational readiness is required to make it a reality.