Everything You Wanted to Know about Blockchain(But Were too Afraid to Ask)

Introduction

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

The blockchain distributed ledger system was made famous with the controversial introduction of the Bitcoin cryptocurrency.

While the uses of Bitcoin are controversial, blockchain is widely regarded as having the potential to be among the key technological revolutions of this century.

Today, most major financial institutions are running some kind of blockchain pilot program. However, while blockchain recordkeeping has the potential to address certain infrastructure limitations of the financial industry, it is not a cure for all.

Blockchains can modernize various aspects of the current IT infrastructure environment by streamlining the underlying information architecture. However, ‘quick wins’ are likely to be elusive. First, many technological challenges with blockchain need to be overcome before it can be considered enterprise-ready. Second, institutions need to carefully determine whether this technology will be more cost effective than the status quo, for the specific problems they seek to address.

The Basic Concept

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

The blockchain distributed ledger system was made famous with the controversial introduction of the Bitcoin cryptocurrency.

While the uses of Bitcoin are controversial, blockchain is widely regarded as having the potential to be among the key technological revolutions of this century.

Today, most major financial institutions are running some kind of blockchain pilot program. However, while blockchain recordkeeping has the potential to address certain infrastructure limitations of the financial industry, it is not a cure for all.

Blockchains can modernize various aspects of the current IT infrastructure environment by streamlining the underlying information architecture. However, ‘quick wins’ are likely to be elusive. First, many technological challenges with blockchain need to be overcome before it can be considered enterprise-ready. Second, institutions need to carefully determine whether this technology will be more cost effective than the status quo, for the specific problems they seek to address.

BITCOIN VS. BLOCKCHAIN

For readers less familiar with the core technology, it is crucial to separate Bitcoin and blockchain. The former is an application that uses a blockchain for the transfer of network-issued currency, and the latter the enabling technology that can be applied more broadly.

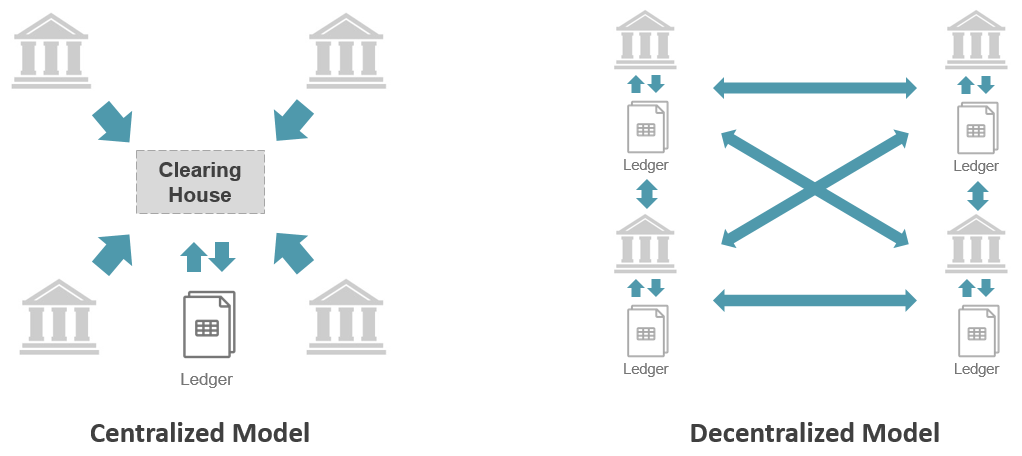

Blockchains, the underlying ledger technology for Bitcoin, create a new medium for assets. The adoption of blockchain technology changes the nature of money itself, enabling it to move seamlessly, without requiring any sort of central clearing house (Figure 1). Traditionally, digital payments worked via messages (record, process, clear, settle, reconcile) to enable the value transfer and a single, centrally maintained ledger. If blockchain technology gets adopted, this value transfer would become immediate and direct, as the valid ledger would be distributed and decentralized, rendering a central clearing obsolete.

Figure 1: Centralized vs. Decentralized Ledgers

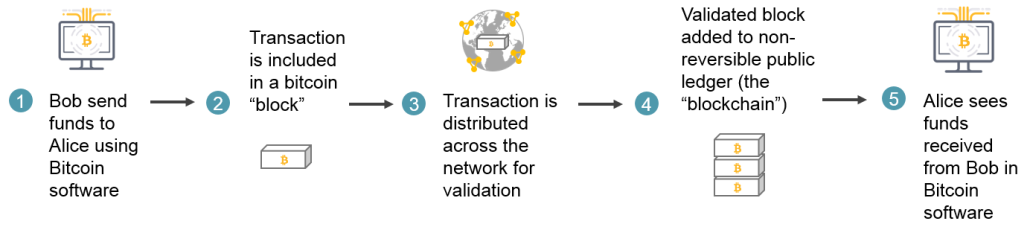

BITCOIN 101

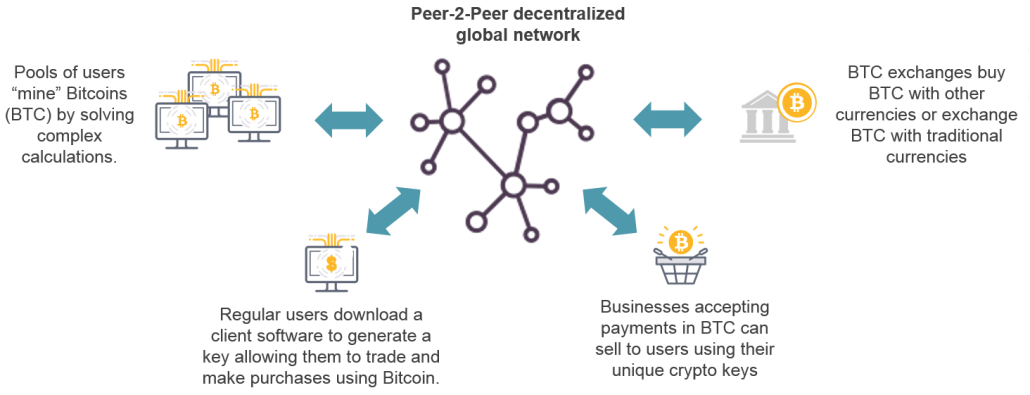

The Bitcoin cryptocurrency is a network-issued form of payment. The ecosystem itself was built as a distributed, peer-to-peer platform, with the objective of being able to validate and track transactions without any centralized control points. The main stakeholders and processes are depicted in Figure 2 below.

Figure 2: How does Bitcoin work?

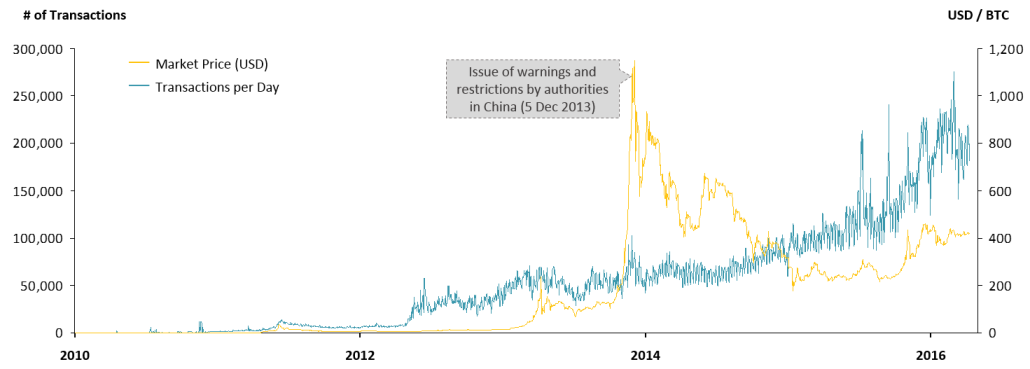

At its core, Bitcoin is based on a global, peer-to-peer value transfer and transaction protocol (i.e., the blockchain). The currency of this network is denoted in BTC, with the smallest unit Satoshi (one-hundred-millionth of a Bitcoin). Figure 3 illustrates the dramatic rise of BTC against the dollar over the past few years, as well as the steady increase of transactions:

Figure 3: The Rise of Bitcoin

THE BLOCKCHAIN: IN BLOCKS WE TRUST

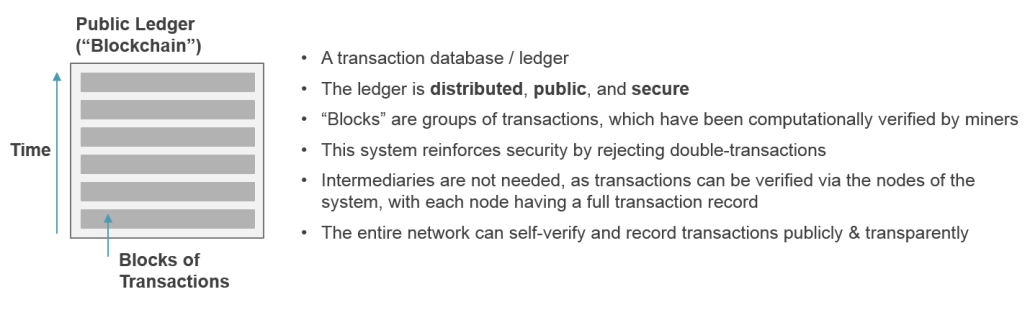

The blockchain is a publically-available ledger of Bitcoin transactions (although it can be used for tracking different assets) that are structured in so-called blocks, each of which contains a certain number of transactions. New blocks are added to the public ledger approximately every 10 minutes; they contain transactions that are validated by network participants.

To understand the advantages of blockchain, consider the following analogy: for a blind polling system, imagine a mechanism that could publish encrypted records of all voting activity. Using a private key, any voter could validate whether his / her vote was counted, and anybody could validate that all counted votes are valid, i.e., provided by eligible voters. Such a system would provide full transparency without sharing any of the voting information – and blockchains do the same for any asset transfer.

The blockchain serves as a decentralized database for the Bitcoin ecosystem, but also fulfills a multitude of other functions. The key elements considered here are those relevant for a broader usage of the blockchain:

1. Validation and record keeping of transactions

In the blockchain universe, there is no record of absolute account balances; rather, by having access to all transactions since the very first launch of the blockchain, participants can calculate individual account balances “on the fly” by being able to see how many coins an individual account received versus how many it sent out. When a new transaction is proposed for inclusion into the blockchain, network participants can easily check if such a transaction is valid, i.e., if the corresponding account has the funds in question. If validated, the transaction will be included in a block (minimal transaction fees apply) and eventually added to the blockchain.

Figure 4: Blockchain Characteristics

2. “Proof-of-work” consensus mechanism

Generally speaking, a “proof-of-work” is a piece of data which is difficult (costly, time-consuming) to produce but easy for others to verify. For blockchains, this concept is used to manage the ledger control among the various participants (i.e., who can make changes to the ledger and when). Blocks are validated in a random process, the so-called “mining”; for each of the blocks, a “proof-of-work” has to be produced.

Figure 5: Blockchain – A Distributed, Public Transaction Ledger

All participating individuals (“miners”) compete to find this “proof-of-work”, a solution to a crypto math problem that involves the transactions of that block as an input. Once a miner finds a solution, it gets broadcasted to all network participants, who can easily confirm its validity and accept the new block. In this way, the network is also protected against fraudulent activity or alteration: the power of the consensus mechanism lies within the extreme computing resources needed for solving the underlying crypto math problem for each of the blocks. The system makes it virtually impossible for any individual to compute the block confirmations quickly enough to be able change the transaction after-the-fact (the details would exceed the scope of this intro text).

In very rare instances, two miners can find two valid blocks simultaneously, both containing a different set of transactions, and thus creating two “forks” of the blockchain. Such a conflict gets resolved as soon as one of the two forks progresses to a greater length (i.e., another block, based on that fork, is confirmed), at which point the network discards the shorter fork. One of the important implications of this mechanism is the avoidance of double-spending: an individual might be able to spend the same coins twice in the short-run (i.e., a ~30-min period), but only one of the transactions will be confirmed.

What Lies Ahead

The key advantages of a blockchain-enabled world are obvious: financial institutions would be able to track their assets ubiquitously – instead of having to keep track of multiple databases separately. Today, settlement and clearing of US equities takes three days. Blockchain has the potential to reduce this transaction time to just minutes, while simultaneously reducing costs and systemic risk. Blockchain-based ledgers would also facilitate compliance with AML, KYC, and other regulations, since they provide an unalterable record of all past transactions.

However, the current state of distributed ledger technology faces many challenges: it is immature, unproven, has inherent scale limitations in its current form and lacks underlying infrastructure that would allow a seamless integration into the existing financial market environment. Improvements will come with time as the industry learns from successes and failures of marketplace experiments.

From a pure technology perspective, the blockchain does not facilitate data integration and does not feature any built-in synchronization mechanism with existing systems. It does not include supporting workflows, exception processing or any of the extensive preprocessing logic that often accompanies complex matching, allocation and other processes that precede the point at which a transaction is considered complete.

It remains to be seen whether the current use of central, responsible authorities, such as central repositories and custodians, will continue to dominate the marketplace in the future, or whether distributed systems using mathematics and cryptography to guarantee integrity will provide a better alternative. One future scenario may involve both forms of processing simultaneously. Either way, financial institutions should pay close attention and seize the emergence of this technology as an opportunity to assess how to modernize themselves.