Rethinking B2B Payments

The business-to-business (B2B) payments ecosystem, long characterized by complex, manual processes, has reached an inflection point. The proliferation of digital payment methods is fundamentally reshaping how businesses and consumers manage their finances.

As B2B payment innovation accelerates, financial institutions and banks failing to meet elevated expectations risk losing significant market share to FinTech disruptors. A recent study found that ¾ of corporate customers consider money management a challenge when executing B2B payments. And yet, while 66% of financial institutions consider digital payment offerings a key success factor, only 30% believe their current tools effectively reduce friction for their customers.1

The consumerization of B2B payments means successfully retaining market share will require banks and FIs to not only digitize payments themselves, but also provide efficient solutions to the entire payments workflow. From dedicated supplier portals to automated Accounts Payable (AP) and Accounts Receivable (AR) systems, the B2B customer experience will be defined by customized solutions, simple cash flow management, and a streamlined payment cycle.

Executing a future-proof digital innovation strategy is pivotal for any bank or financial institutions’ long-term success. While the B2B payments space represents a sea of opportunity, fierce competition has incited a digital arms race!

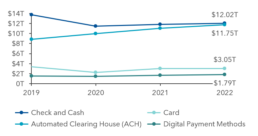

The global transaction value of business-to-business (B2B) payments reached just over $88 trillion in 2022 and is expected to exceed $111 trillion by 2027.2 However, while B2C Ecommerce solutions have expanded globally, revolutionizing how consumers spend and send money in real-time, B2B buyers still overwhelmingly default to old school payment methods. Roughly 40% of all B2B payments in the United States are still executed via paper check or cash:

Exhibit 1. US B2B Payment Transaction Value, by Transaction Method, 2019-2022 (in Trillions)

Buyers and suppliers relying on antiquated payment processes experience pain points that negatively impact their bottom line:

1.High Processing Costs:

Manual payment operations, on average, cost businesses 2% of their annual sales, while payment processing costs another 0.8%.4

2. Delayed Payments:

~47% of suppliers are paid late for their products or services.5 Payment delays are largely due to the extensive B2B payments process – a B2B transaction involves (1) the creation of a purchase order by the buyer, (2) the fulfillment of the order by the supplier, (3) the creation of an invoice from the supplier’s Accounts Receivable (AR) department, and (4) the processing and payment of the order by the buyer’s Accounts Payable (AP) department.

Exhibit 2. Manual B2B Payment Pain Points

3.Supply Chain Disruption:

B2B movements in supply chains typically outpace their underlying cross-border payments, which results in bottlenecks and loss of value.

4.Cumbersome Data Processing:

Manual payment processes often pose a challenge for businesses reconciling multiple invoices and receiving and processing remittance data. Missing data elements in the files, the use of inconsistent file formats, and the lack of back-office support for automated remittances pose significant challenges for data processing.

5.Lack of Transaction Visibility:

Manual payments provide for limited end-to-end transaction tracking, which may result in delays, additional costs, chargebacks, and payment cycle disruption.

6.Increased Susceptibility to Fraud:

Paper checks are more susceptible to commercial fraud than any other payment method, with 2/3 of organizations experiencing check fraud (2022).

Covid-19 exacerbated pain points around managing invoicing and payments in the B2B value chain and helped catalyze digital adoption. As the pandemic wreaked havoc on supply chains across the globe, suppliers realized the need for transparent, end-to-end tracking of goods.

Inefficient processes, coupled with elevated customer expectations, are driving a new wave of payment digitization. One study forecasts that 80% of all B2B payments will be digital by 2025.

...But a complicated problem

While payment digitization has reshaped the B2C space – with over 70% of B2C payments made electronically – electronic B2B payments has significantly lagged in adoption across industries and remains an underpenetrated market. Two major contributing factors to this slowed adoption are (1) the nuanced nature of cross-border payments and (2) the inherent complexity of B2B vs. B2C payment transactions.

CROSS-BORDER PAYMENTS

Cross-border B2B payments, where the payee and transaction recipient are based in different countries, are notoriously complex and difficult. In fact, over a quarter of small-to-medium-sized businesses rank the complexity of executing cross-border payments as one of their top obstacles. Often touching many intermediaries, cross-border payments frequently lead to unpredictable delays. Business seeking to execute cross-border payments face several challenges:

Inconsistent Regulation:

Regulatory adherence and the tightness of controls around Your Customer (KYC) and Anti-Money Laundering (AML) vary per country. For instance, while AML controls are more established in Europe, the controls in Africa, and particularly North Africa, may be less defined or rigorous. This means an increased likelihood of payment delays due to AML problems.

Lack of API Interoperability:

While Application Programming Interfaces (APIs) facilitate information sharing across different payment networks and systems, they can only communicate with each other if they are interoperable. Currently, there is a distinct lack of global interoperability and standardization, with only 38% of payment system operators reporting the existence of domestic standards for APIs.8 Lack of API standardization means that cross-border payments will remain a challenge for B2B payments.

Corridor + Currency Complications:

The setup required to support a B2B client’s business in a new corridor or currency is often cumbersome. Receiving banks lack visibility into when payments will arrive and are therefore unable to provide status updates to their customers/suppliers. Moreover, the amount of money involved in a transaction may change as a result of exchange calculations and various fees.

COMPLEXITY OF B2B VS. B2C

While B2C payment transactions typically compromise of small, one-off purchases executed via synchronous, real-time payment methods (e.g., debit/credit cards, PayPal, Venmo, etc.), B2B payments are considerably more complex.

B2B transactions typically require an extensive decision-making process with inputs and approvals from multiple stakeholders across different departments of an organization. Asynchronous payment methods, coupled with large order quantities that may contain thousands of individual line items, lead to 30–90-day payment terms.

As technology makes global ventures easier to launch and manage, the proliferation of new cross-border B2B businesses has made it more important than ever for financial institutions and corporations to streamline B2B payments.

Exhibit 3. B2B vs. B2C Payment Transactions

The new wave of digital payments

Digital payment methods are addressing B2B customers’ pain points and modernizing the B2B payments ecosystem by offering real-time or same-day payments, elevated security, and transparent bi-lateral communication between buyers and suppliers. The digital payments revolution is being driven by several electronic payment solutions:

Exhibit 4. Digital B2B Payment Solutions

REAL TIME PAYMENTS

A real-time payments (RTP) rail is the digital infrastructure that facilitates payments that are initiated and settled almost instantaneously. RTP are streamlining the payment delivery process for B2B customers by providing benefits that directly impact their bottom line:

1.Increased Savings: Manual payment processes cost B2B customers $25+ per transaction, whereas RTP often cost less than $1 per transaction.10

2. Boosted Efficiency: Near-instantaneous settlement prevents bottlenecks in supply chain execution.

3. Elevated Transparency: RTP provide both parties, payer and payee, notifications of confirmations and settlements. Establishing bilateral communication facilitates trustworthy payments between businesses.

RTP have proven particularly disruptive in the cross-border payments space. Leading financial services firms have designed networks to enable participating financial institutions to execute secure, efficient global business payments. For instance, Visa’s B2B cross-border payments solution, Visa B2B Connect, provides its customers with seamless bank-to-bank cross-border transactions via a non-card-based payment network. Businesses use Visa’s multilateral network to send irrevocable payments in full to the beneficiary’s bank with exact confirmation of funds delivery.

Exhibit 5. Visa B2B Connect Functionality

By offering a global network, Visa B2B Connect’s customers avoid intermediary fees and are ensured clarity on financial exchange rates. Visa is also able to ensure data privacy via a digital identity feature that tokenizes an organization’s sensitive business information, providing them with a unique identifier.

VIRTUAL PURCHASING CARDS

While purchasing cards have revolutionized the B2B payments sector since their mainstream market acceptance in the mid-90’s, 2021 saw the inception of a more secure, digitally-enabled p-card – the Virtual Card. Virtual Cards are essentially “card-less” credit cards that generate a unique 16-digit card number issued for a specific supplier/organization with a pre-set, one-time payment amount. The cards are processed by vendors similarly to traditional credit or pay cards, yet do not require a physical card or open line of credit. Payments via Virtual Card are sent directly to a supplier’s account without any action needed on behalf of the supplier.

Virtual Cards promise elevated security for corporate expenditure from travel to procurement. The unique card number feature ensures that even if the card is compromised, its pre-set pay limit, expiration date, and organization designation prohibit unanticipated spending. Virtual Card payments are anticipated to grow to over $65 billion by 2030.11

Virtual cards have seen increased adoption within the hospitality industry. Online Travel Agencies (OTAs), which operate with relatively thin margins, leverage virtual cards to reduce inefficiencies when purchasing from tourism suppliers. Customers booking their vacations might chose to bundle lodging and car rental booking through an OTA like Expedia or Kayak. As they proceed through the checkout flow, they may choose to upgrade their booking through a loyalty program or add an insurance program from yet another vendor. Virtual card solutions allow for logic to programmatically create a card for each order and automate otherwise entirely manual processes.

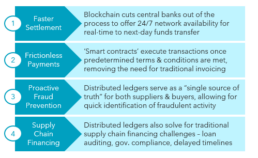

BLOCKCHAIN TECHNOLOGY

While it is a popular subject of controversial press, Blockchain technology’s potential to fundamentally change the payments landscape is undeniable. At its core, blockchain is an advanced database mechanism that allows for transparent information sharing within a business network. It creates a decentralized, immutable ledger of chronologically consistent data that cannot be altered or deleted without consensus from the network.

Exhibit 6. Benefits of Blockchain for Businesses

Whereas public blockchain networks are permissionless and allow all users to read, edit, and validate the blockchain, businesses seeking to securely execute B2B payments require access to private, hybrid, or consortium blockchain networks. These networks feature access restrictions that ensure secure data flow. However, implementing a new blockchain network is costly and resource-intensive.

Blockchain-as-a-Service (BaaS) provides businesses a shortcut by packaging the smart contract technology, blockchains, and network infrastructure they run on. Emerging FinTechs, like PayStand, Bloq and Dragonchain, as well as established tech giants, like Amazon, offer B2B clients blockchain solutions at a fraction of the cost.

EMBEDDED PAYMENTS

Embedded payments promise stickier customer relationships, increased buying ease and convenience, and fewer days sales outstanding (DSO). While online shopping historically required payment processing to be executed via a third-party provider or banking service, embedded payments seamlessly integrate financing and digital payment processing into the ecommerce journey. Payments, therefore, feel more like a natural extension of customer engagement as opposed to a separate, cumbersome activity.

In the B2C arena, embedded payments have become the status quo –Amazon shoppers and Uber riders have grown accustomed to executing payments in-app at the click of a button. To provide a similarly convenient payment experience, B2B embedded payments must provide connective tissue between all aspects of the payment’s workflow – from invoicing to funds disbursement.

While embedded payments are still in early adoption in the B2B space, emerging FinTechs are embracing the long-term value that embedded capabilities deliver. In one example, via a partnership with OpenText, BigCart’s payment solutions are now offered to businesses running OpenText’s cloud-based supply chain management software, providing upwards of 1.1 million trading partners access to embedded offerings.

BUY NOW, PAY LATER

US firms alone account for upwards of $3 trillion accounts receivables on any given day. The BNPL value proposition promises better cash flow management through on-demand settlement of invoices. Providers typically take on the risk of late or unpaid invoices to help better match buyer and supplier cash flows. The matching of cash dynamics allows suppliers to settle transactions faster while providing buyers the ability to increase predictability of cash outflows. B2B BNPL directly improves supply chain throughput and allows businesses to grow without the need for traditional financing. For in-depth Kepler Cannon insights on BNPL, see Navigating the Buy Now Pay Later Era.12

New age BNPL offerings will need to leverage outsourced or automated underwriting to provide significant advantage over conventional credit checks. By accelerating cash flow and potentially reducing the cost of borrowing, providers will be able to effectively showcase value and acquire customers at scale.

The unprecedented size of the market coupled with better risk visibility has led to the emergence of several innovators in the space. New age BNPL players such as Billie, Tillit & Tranch are building highly customized, industry focused solutions using latest technology which allows them to rapidly acquire share from slow moving financial institutions.

The consumerization imperative

Like consumers, businesses require efficient, secure payment methods tailored to their needs. However, B2B payments cannot be viewed in isolation, but rather as part of a broader set of processes involving purchase orders, invoices, payment terms, cashflow management, and accounts payable (AP) and accounts receivable (AR) departments. In order to thrive amidst growing FinTech disruption, banks and financial institutions must streamline the entire payments workflow by expanding their digital toolkit.

Exhibit 7. Bank/FI Digitization Toolkit

Dedicated Supplier Portal. Dedicated supplier portals are the foundation of a simplified B2B procurement process. By automating many of the traditionally manual steps in a B2B transaction – from issuing purchase orders to providing access to related invoices – supplier portals expedite the entire payment cycle. Portals also maintain a central log of all updates regarding a purchase order, serving as a transparent, single source of truth for both the vendor and the buyer.

Real-Time Cashflow/Data Management and Reporting. Cash flow challenges, intensified by late payments and rising inflation, pose an immediate threat to all businesses, but especially small and medium-sized businesses (SMBs). All-in-one payments platforms provide a comprehensive solution for automated reporting and working capital management. By identifying constraints in the invoicing process, businesses can realize revenue more quickly.

Enterprise Resource Planning. Enterprise Resource Planning (ERP) platforms integrate all essential functions of a business and enable data flow between them. Integrating payments via an ERP reduces IT costs, inventory levels, and payment cycle time. By reducing AP volume, 95% of businesses leveraging ERPs improved their businesses processes and 82% improved met projected timelines for the systems’ ROI.13

Simple Integrated Accounts Payable and Accounts Receivable System. Automating AP and AR functions expedites two of the most repetitive, manual processes in the payments workflow and allows for faster payment reconciliation.

Automating AP removes the need for finance teams to collect, sort, and verify transaction receipts. Similarly, Automating AR allows businesses to set certain invoices as recurring and send them automatically at particular dates, rather than having to create a new invoice each month.

Building a future-proof digital strategy

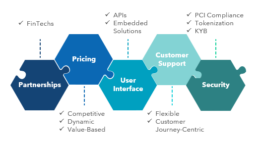

In order to successfully execute a future-proof digital innovation strategy, banks and financial institutions must consider several elements to streamline the entire payments workflow.

Exhibit 8. Digital Strategy Considerations

PARTNERSHIPS

While implementing an entirely new digital payment rail is resource and time-intensive, banks and FIs can leverage FinTech partnerships to upgrade their legacy technology. Banks and FIs should maintain a customer-centric focus when identifying what needs a potential partnership might solve. Some considerations include:

1.Which FinTechs will facilitate a streamlined payment experience or increase speed-to-market for your largest accounts? (I.e., global players seeking to execute transactions in new corridors or complex use cases)

2. What IT gaps would the partnership solve? Will the FinTech facilitate seamless data flow to your ERP?

3. Would the partnership help automate part or all of the payments workflow? (purchase orders, invoicing, AP and AR functions, etc.)

PRICING

A fundamental element to a best-in-class digital B2B payment solution is competitive pricing for buyers and suppliers. Banks and FIs should have a thorough understanding of how their value proposition holds up against disruptive market entrants seeking to capture price-sensitive customers. Some considerations include:

1.How will pricing vary by customer segment or offering? (e.g., self-service for standard clients and on-demand white glove support for strategic accounts)

2. What data/benchmarks can be leveraged to reduce leakage and improve overall pricing performance?

3. Is your commercial team upskilled enough to communicate strong value messaging and pricing considerations to customers?

USER INTERFACE

Improving the point of contact for B2B customers is a key concern for any bank or FI’s success in the age of consumerized payments. APIs and embedded solutions are essential assets to improve the customer experience, fuel innovation, and generate growth from corporate customer segments. Some considerations include:

1.What constitutes a comprehensive API strategy and road map for your customer base? (e.g., geographic and segment considerations, onboarding complexities, shifting regulation and standardization)

2. How will you align KPIs and incentives across internal functions to ensure a product-centric roll out of new API-enabled products and services?

3. How will you align front and back-office departments to provide a wholistic embedded solution? (e.g., PO numbers, AP/AR systems, ERP integration)

CUSTOMER SUPPORT

Offering elevated, proactive customer support can be a key differentiator in an ever-changing digital environment. Banks and FIs should consider optimal support a strategic advantage. Some considerations include:

1.Are the educational materials you provide customers pointed and use case-specific? (e.g., detailed onboarding guides, multi-lingual FAQs, anticipated payment timeline overviews)

2. Do you couple an easily-accessible website support portal with efficient query escalation protocols? (e.g., direct contact support line, community forums, conflict resolution KPIs)

SECURITY

Ensuring a safe, secure B2B payments process is paramount for banks and FIs. Some considerations include:

1. Have you implemented PCI-compliance checklists for employees and customers? (e.g., strong access control measures, periodic network tests, malware and antivirus protection)

2. How are you addressing regulatory standards for Know Your Business (KYB) ?

Are you offering diverse, unique tokenization technologies to protect customer data throughout the payments process?

In closing...

Accelerated digital payments adoption represents the end of cumbersome, manual B2B payment methods. Digitally-enabled disruptors that are better equipped to meet customers’ elevated expectations threaten to steal significant market share from legacy banks and financial institutions over the long term.

One dimensional digital solutions will fall short of accommodating the inherent complexity of B2B payments. Succeeding in the B2B space will require a customizable offering that streamlines the entire payments workflow.

In order to thrive in the new age of digital payments, Banks/FIs need to hit the bull’s eye in expanding their digital toolkits and executing a future-proof digital innovation strategy. Dedicated supplier portals, cashflow management solutions, Enterprise Resource Planning, and integrated Accounts Payable and Accounts Receivable systems are the digital backbone behind consumerized B2B payments. Adequately assessing the gaps in its current value proposition will prove to be a make-or-break strategic imperative for any bank or FI.

__________________________________________________________________________________________________________

- PAYMENTS

- Juniper Research

- Insider Intelligence

- PAYMENTS

- Digital Commerce 360

- J.P.Morgan

- PAYMENTS

- PAYMENTS

- FT Partners

- FIS

- Global News Wire

- Navigating the Buy Now Pay Later Era, Kepler Cannon

- PAYMENTS

Read More

Transformation Readiness

70% of all planned transformation initiatives fail to deliver tangible business value and 84% of organizations fail at tech transformations in particular.

Rethinking the Future of your Business

The economic climate is becoming increasingly uncertain with cautionary signals of recession, along with inflationary pressure, fluctuating currencies, and uncontrollable impact of geopolitical events. Firms need to proactively take this opportunity to refocus their future investments on high value, high potential business lines.

Technology and Healthcare

Data production in healthcare occurs in different volumes, velocities, and formats by multiple sources – EHR, diagnostic, imaging, claims, billing, medical devices to name a few.

Enterprise Cyber Resilience in a Hybrid World

Cybersecurity incidents are also not only a threat to corporations’ internal operations and bottom line; customer personally identifiable information and financial data is also at serious risk of exposure and misuse, in turn impacting customer perception and long-term brand loyalty.

Finding Growth in US Insurance

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Data-Driven Post-Merger Integration

A common misconception is that revenue synergies are illusive or “icing on the cake”, primarily because they are more challenging to quantify.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

Platformization of Health Tech

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously

Are Your Vendor Risks Under Control?

Investing in vendor risk management today can secure a future brimming with cost-effective, secure, successful and trust-worthy partnerships.

(AI)ntelligent Procurement

In a competitive business environment, high-performing CPOs are 18x more likely to fully deploy AI/cognitive capabilities. This typically leads to 92% faster demand forecasting, on average 350 man-hours are saved through automation, and there is a potential for 24/7 operations

Realizing Your Workforce Strategy

Organizations are now recognizing the limitations in their workforce programs, so are making a concerted effort to develop a contingent workforce strategy, consolidate their master vendors/staffing agencies, and extract maximum benefits from the program.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Getting the Basics Right

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Embracing Open Banking

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

Ensuring Loyalty of your Prized Clients

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

The Cloud-Native Paradigm

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Business Analytics in Pandemic Times

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Reshaping Wealth Tech

Before the Covid-19 inducted recession, the wealth tech sector was already experiencing a slowdown - both in the number of new startups and total capital raised. Now more than ever, investors and operators must be bold in re-inventing their Firm's long-term value proposition.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

How to Thrive in the New Normal

Now that Business As Usual is unusual, leaders are forced to re-imagine business models and build ‘winning strategies’ - to not only survive the pandemic but also emerge as successful change-makers, shaping an altered business reality.

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Trends in Digitalization of Insurance

For some, Insurance might seem a monolithic industry, but for the ones keeping a close eye on it- Insurance is revamping itself faster than ever!

From days when underwriting a simple policy would take weeks and months, to now when it can be done in seconds with a simple ‘selfie’ - there seem to be no bounds in the future of this industry.

Customer Engagement Index

While firms have found tremendous success in using these loyalty metrics to successfully grow customer relationships, they are lagging indicators and provide little help in providing immediate insight into whether or not improvements and initiatives are moving the needle.

Strategic Sourcing of a “Difficult” Spend Category

Some clients have even deemed spend reduction in procurement categories like legal services, where recourses and expertise are concentrated within humans not technology, to be intractable. At Kepler Cannon, we continuously challenge these sorts of conventional wisdom.

Third Party Information Risk Mitigation

It is well known that one way to make better predictions about how your customers, distributors and suppliers will behave, is to augment your own data with that of third parties.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Reducing Strategic Over-Dependence on IT Vendors

Over time, many firms realize that they have become so reliant on vendors/contractor for critical knowledge on key applications, that they have, in fact, ceded control of those applications to the vendors.

Are Blockchains Evolving Like Securities Exchanges?

Driven by data security concerns, a majority of financial institutions are now looking at so-called private or hybrid blockchains, rather than fully decentralized public blockchains (like the blockchain used for Bitcoin)

How Global Resourcing May Be Killing Your Company’s Efficiency

As global firms respond to the post-Great Recession regulatory and economic realities, efficiency of the back-office has become critical to ongoing success.

Third Party Vendor Risk – A Continuous Mitigation Strategy

The last thing any multinational organization wants to worry about are business and compliance risks introduced by third party vendors.

Everything You Wanted to Know About Blockchain (But Were Too Afraid to Ask)

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

Enabling Growth through Practice Management

In the world of financial advisory, growth strategies often focus squarely on the end client; after all, growth is achieved through new client acquisition or new asset acquisition from existing clients. While this logic is not incorrect, it fails to acknowledge the intricacies of third party distribution.

Reshaping the Indian Life Insurance Market

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market.

The Growing Asian Wealth Management Market: Capturing the Mass Affluent Opportunity

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry.

(Not) Selling Life Insurance in Asia

Amidst a boom in insurance business, Asian consumers remain largely underinsured.

Role Reversal: The Future of US Banks in the Online Lending Market

Following the financial crisis in 2008, Fintech startups gained a lot of prominence globally as consumers started to look for alternatives to traditional banking methods. These startups have penetrated every service area of consumer retail banking with the goal of dis-intermediating banks and becoming the new leaders of the financial services industry.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.