Reshaping the Indian Life Insurance Market

Introduction

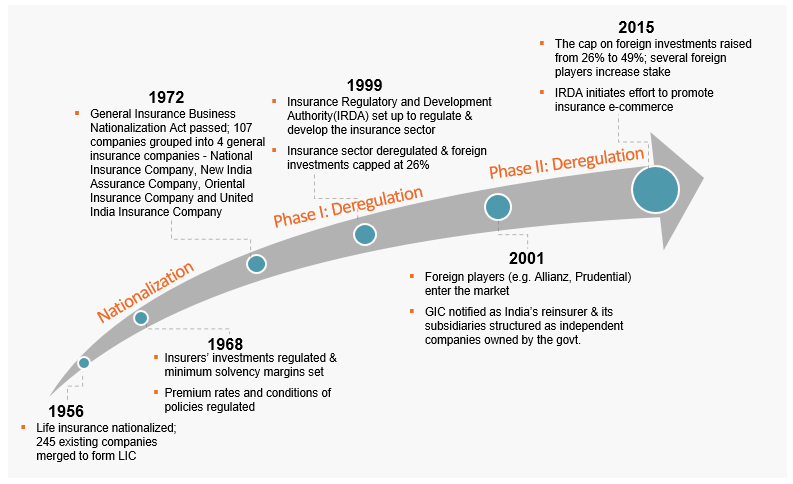

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market. Over the last 60 years, India has transitioned from tight state control over its insurance industry to much more market friendly conditions (exhibit 1). And as the industry anticipates growth following the latest push toward deregulation — which has occurred gradually over the last 15 years — there are four key trends that will shape the Indian life insurance market over the next decade.

Exhibit 1: Deregulation of Indian Insurance Industry

1. THE EMERGENCE OF DIVERGENT INCOME SEGMENTS

At 26%, India has experienced the highest growth in high net worth individuals in the world, and with increasing consumer appetite for insurance products, insurers and wealth managers are attempting to keep pace with the growing interest of demanding investors. From a service delivery standpoint, the industry is slowly pivoting toward more customized services, digital contacts, real time reporting and filtered communication, critical to the success of these companies. Insurers and wealth managers are also making inroads into the home turf of Chartered Accountants and Tax Consultants by transforming their client service model; the older, almost doctrinal approach of wealth maximization is being replaced by a more goal-based investment and protection approach, with special focus on major customer milestones including marriage and retirement.

However, market opportunity is not limited to HNWIs — another emerging market exists at the other end of the spectrum. Although low income families comprise the largest consumer population in India, life insurers have historically avoided them due to low operating margins, difficulty in building scalable business models, and challenges with finding effective distribution channels. While much of this remains true today, regulators now mandate that 7% of all life insurance business come from the rural sector in the first financial year, which is in turn aggrandized to 18% by the sixth financial year. As a result of this regulatory nudge, the number of micro-insurance policies sold increased by 218% from 2007 to 2010.

In order to penetrate the rural market and achieve scale, insurers are now moving toward localizing distribution through community banks, microfinance, and self-help groups and affinity groups such as mahila banks, while also introducing new, more targeted, products to cater to rural needs, including weather insurance, rainfall index insurance, and hybrid micro-insurance.

2. DIGITAL IS A LOW COST POINT OF SALE

From 2008 to 2013, search queries related to life insurance grew by a factor of 4.5, and it is estimated that 3 out of 4 policies will be influenced online by 2020 across pre-purchase, purchase and renewal stages. While the rise of the digital channel is well noted, its disruptive impact across the insurance value chain — originating with sales and marketing down to post-sale service and claims management — is not fully understood or leveraged.

As customers become increasingly digital, companies must move away from simple ‘vanilla’ products to enhanced offerings that provide a greater degree of customization, including allowing customers to add riders and purchase bundled and hybrid products. Companies like ICICI Prudential and Metlife have begun selling simple Direct Purchase Insurance (DPI) products online. Moreover, with the rise of online aggregators with transaction capabilities that offer policy comparison services (e.g. policybazaar.com), the need to differentiate products in a competitive and consumer friendly market will increase.

3. INDUSTRY WILL SEE A STEEP SHORT-TERM INCREASE IN FDI VIA BANCASSURANCE PARTNERSHIPS

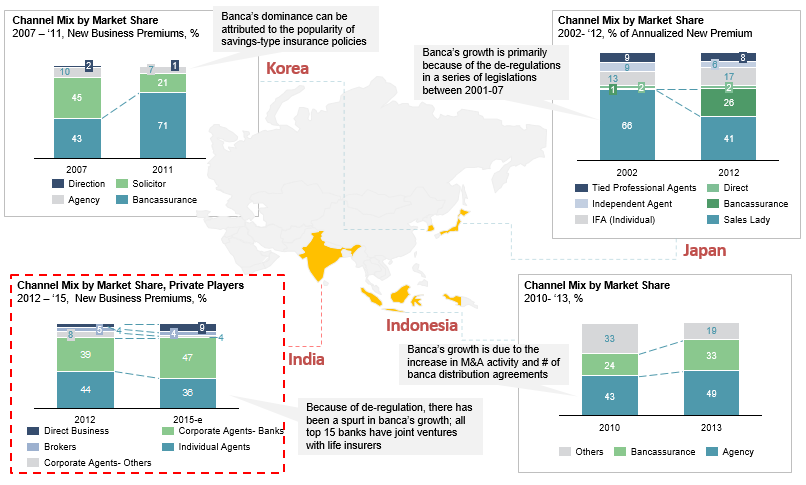

Over the last decade, several Asian markets have seen the rise of bancassurance as a dominant distribution channel (exhibit 2). While the share of bancassurance has been steadily on the rise in India, as well, it is likely to see a sharp increase in the next few years because of this latest deregulation drive.

Exhibit 2: Rise of Bancassurance in Asia

The cap on FDI has been increased to 49% from the earlier 26%, and major foreign players like Sun Life, AXA and Dai-ichi Life have increased their investments. It is likely that new insurers will follow suit. Twenty-one out of the 24 life insurance firms in India are profitable, and the average time to break even in the Indian market is seven years, lower than the global average of eight to ten years. Moreover, banks have now been permitted to partner with up to three insurers under the new open architecture policy. The market should expect to see a rise in partnerships in an effort to lower costs, create greater operational synergies, diversify products, and close the gap on thinning margins in other product lines, all while becoming a one-stop shop for all financial needs.

4. MOVE TOWARD CUSTOMER-CENTRIC SERVICE MODEL

Today, the pre-sales experience is in its nascent stages, in spite of insurers’ efforts to provide product transparency. However, firms are actively streamlining their sales process. Issues associated with legacy platforms are being ironed out, while leaner technology is being deployed to streamline KYC validation and to make near-real time underwriting and policy decisions. For ICICI Prudential, 93% of new business applications were initiated using digital platforms, while a subsequent 69% service transactions were processed through the web, SMS, and IVRS.

Additionally, there is a growing emphasis on more frequent touchpoints post-sale to improve customer retention. Insurers have begun organizing revival campaigns, actively pitching policy continuance, and implementing other initiatives to increase customer awareness on the benefits of policy continuance. There is also new focus on improving the convenience of paying renewal premiums, which has been achieved in part by establishing more branch locations, while insurers are also innovating existing infrastructure to improve the customer experience. For example, HDFC Standard analyzes which customers are most likely to surrender their policies and proactively emails them through financial experts. To promote cross-selling, HDFC has set up a lead warming center to increase share of wallet among its existing customer base.

It’s worth noting that analytics has been a key enabler of customer centricity across the sales life cycle. Insurers have deployed data to better promote cross-selling, improve persistency rates, and mitigate risk. HDFC Standard in particular has distinguished itself through improved cross-selling and up-selling ratios using this approach, in addition to targeted marketing campaigns and and growth in the direct channel via frontline sales and tele-sales resources.

Conclusion

As India’s life insurance market has matured and moves into its next phase of deregulation, insurers and wealth managers will continue to seize on the newfound opportunities presented by this enormous market. With customer appetite across the wealth spectrum, and with growth spurred by technological innovation, insurers should expect to see continued room for expansion. In turn, Indian customers should expect an increase in both financial partnership opportunities among their insurance providers and customized outreach by these firms.