The Nine Lives of Credit

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. Much like cats’ nine lives, the nine lives of credit ensure that credit perseveres as a foundational component of financial offerings, even as it faces ongoing reinvention and repurposing.

Before there were complex investment products, insurance, Forex (FX), and Peer-to-Peer (P2P) lenders, extending credit to clients was banks’ core value proposition. All bankers were put through rigorous and extensive credit training—rating and capital structure analysis, loan structuring, loan documents drafting, and so on. Expertise in credit analysis served as a differentiator for a bank that had the ability to identify creditworthy clients.

The continued growth of financial services saw products like capital-raising, FX, and investment come to the foreground, leading to the commoditization of credit products. Even so, credit continues to be a foundational component of banks’ value proposition, although not the dominating factor. Challenges around credit weren’t about expertise; the challenge was around the swift identification of prospects and distribution of credit as banks worked to find a balance among quick decisions, maintaining acceptable risk levels, and avoiding impairment.

While the credit product has seen standardization, the delivery of the product and its value chain has evolved with the emergence of advanced digital capabilities, challenger banks, and online lenders. These new business models offer seamless onboarding, near-instantaneous decision-making, and convenient customer care—all delivered through a fully digital, end-to-end (E2E) experience. What once took banks months to train bankers to do can now be achieved with a computer.

Now traditional banks find themselves at the cusp of change once again as credit approaches its next set of challenges: How can they transform the credit model to differentiate themselves against peers and grow their loan portfolios? Do existing systems and processes need to be completely overhauled, or can they be reengineered to support the vision of the future state? How do they digitize the credit value chain such that clients’ and employees’ experiences are revolutionized?

The Credit Process Today

Let’s break this down. What chain of events does the dissemination of credit entail? What happens after credit has been extended? How does the current state stack up against the vision of the future state for this offering or against evolving consumer expectations?

The credit value chain comprises the key components identified in Figure 1, most of which are often facilitated through a relationship manager (RM), which adds an extra layer of complexity:

1. Customer Engagement and Prequalification: Some banks create client-facing portals to help engage prospects in the application process for a financial product, while others create product-agnostic apps to engage prospects without having a direct sales motive. Whatever the chosen strategy, the goal is to create a new channel for interaction. A credit-specific route may be to create automated, simplistic “prequalification engines” that can help banks identify a narrower set of targets for sales outreach. Prequalification also prevents low-credit clients from expending unnecessary effort and cuts application-processing costs for banks.

2. Credit Application: Aside from the relatively standard information about the facility, required data about the applicant can vary from bank to bank, but in wholesale banking it usually includes detailed financials and other public information. In fact, the application can require upward of a hundred data points, many of which are not required universally for all applicants or products. Relationship managers must work extensively with applicants to collect this data, and this dependence on clients can trigger substantial delays.

Figure 1: The Typical Wholesale Credit Process

3. Credit Approval: Especially for retail and SMB lending, credit decisions are moving toward algorithms that mimic the knowledge credit officers once held. However, in wholesale banking, this process continues to be unnecessarily complex and manual. Instead of following a definite set of rules, making decisions is treated as an art practiced by credit officers who use their judgment. This process often creates a bottleneck in the credit origination E2E turnaround time (TAT) since the application may be funneled through multiple levels of approvals. Such is especially the case with borderline or complex cases where opinions are subjective.

4. Documentation: Documentation is another step that continues to be largely manual in wholesale banking. Despite the use of templates, the process of creating credit facility letters is tedious, with multiple manual iterations back and forth. In addition, the value chain often gets “stuck” here, especially in cases that require manual approvals before and after negotiating with the client. The letter is often passed around to multiple parties for their opinions, with the process repeated for each iteration of the letter, so the process has the potential to go into what feels like a never-ending loop.

5. Funding and Monitoring: Data from credit applications must then be conveyed to the product-servicing platform, and although it sounds simple and seamless, insufficient systems integration can turn this into one that is resource- and cost-heavy.

After the transfer, ongoing monitoring is conducted to look at covenants and collateral and identify clients who fall below requirements or fail to meet their end of the deal. This prescriptive approach continues to prevail over a predictive analytical approach to pre-empt potential issues.

6. Portfolio Management: Banks must constantly manage their credit portfolios to ensure they are optimized for low risk and high profits. Banks may syndicate loans or perform secondary trading of syndicated loans to manage risks, restructure or redistribute products, and/or adjust their underwriting strategy. However, in each case, banks often struggle because of the absence of insightful and dynamic portfolio reporting under varying lenses (market, manager, borrower etc.). Once more, poor systems integration rears its ugly head, often resulting in myopic views into loans’ health, and soaring risk levels.

Common Pitfalls

With all the innovation in retail banking, one would expect wholesale banking to be even farther ahead of the curve—after all, the clients are so much bigger and the stakes so much higher! However, most wholesale banks continue to be plagued by limitations carried forward through inertia. These limitations come in many forms, but there are four key reasons that processes and systems fail to create optimized experiences today:

-

Workflows are cumbersome and manual:

Technology can allow simpler approvals to be automated and eliminated from workflows entirely, yet processes usually don’t use these opportunities, resulting in workflows that include multiple redundant handoffs. Because of the value once placed on credit training, there is still significant inertia in treating approvals as standardized, algorithmic processes. The involvement of multiple non-critical stakeholders in manual approval can also cause process loops to come into play, so the process can quickly turn into a time-consuming monstrosity.

-

Systems aren’t fully integrated:

Disintegrated systems are a critical roadblock given the number of systems and groups the value chain involves. Improper systems integration can create the need for low-value-added manual labor at every junction. Moreover, the absence of a well-defined data architecture can prevent internal processes from leveraging all of the data an organization has on its clients. Many banks are also plagued by legacy systems that bog down the entire ecosystem, are difficult to integrate, and are even harder to replace.

-

Data gathering is unstructured:

Whether it’s the application, onboarding, collateral verification, or monitoring, there is always white space in data collation. Instead of being predetermined, the data sources to be used are treated on an ad-hoc, case-by-case basis. Data is arguably the most powerful resource in today’s technological setup—taking processes from art to science will be critical in moving the value chain forward.

-

Digitization is still stigmatized:

Fear of robots eliminating humans isn’t restricted to dystopian sci-fi movies, although there is a key difference: the real-life version isn’t fear for one’s life but one’s livelihood. Banks are still a long way from eliminating the need for human intervention, but those who perform low-value-added tasks are quickly becoming redundant. Moreover, certain high-value tasks are undergoing automation—receiving severe pushback from multiple parties—and credit is no exception. While we don’t expect credit offices to be posting “Humans need not apply” signs anytime soon, digitization will have an impact on the workforce. Whether the workforce is repurposed or not depends on individual banks, but just the possibility of unemployment can generate substantial dormancy.

To monetize opportunities created by gaps in the credit value chain, firms need to take advantage of their own unique knowledge to reinvent credit without “reinventing the wheel.”

Today's Shifting Landscape

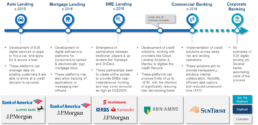

Digitization has already moved from the smallest echelons of retail banking to business banking, making its way into mainstream commercial banking.

In retail banking, credit has seen significant E2E digitization in auto loans and home mortgages.

Business banking has also seen large strides in digitization, with the emergence of P2P lending and online lenders like OnDeck and Kabbage shaking and stirring the competitive landscape.

Flux in the environment has pushed traditional lenders to form strategic alliances and offer loan decisions in a matter of minutes, which they accomplish by moving the application and documentation process online and using auto-decision-making capabilities.

A trend is clearly emerging: digitization is steadily moving upmarket and is poised to break into corporate and institutional banking. The corporate banking sphere is still relatively unexplored, and examples of digitization are limited to transformations that are still in their nascent stages. Opportunity to leap ahead of the competition still exists but is fast dwindling.

New competition isn’t the only source of flux; numerous regulatory changes in recent years will impact credit. While the nature of the impact varies from regulation to regulation, the implication for systems and processes is consistent: faster, more robust solutions with enhanced auditability and data quality are needed.

Figure 3: Digitization of Credit Across Banking

How Can Wholesale Banks Go Digital?

While becoming a digital bank is a tall order, we recommend an agile approach, full of baby steps that can be exposed to clients fairly quickly:

TEMPLATIZE THE CREDIT APPLICATION

If the application requires only data that is relevant to the specific client and product, and data-gathering is automated so all necessary and available information is instantly and accurately collated, then all subsequent steps would benefit. Digitization today can help achieve this vision of a future state in several ways:

-

Using Templates in the Application:

The decision drivers of a small commercial banking client residing in Cambodia will naturally be very different from those of the Coca-Colas of the world. To optimize efficiencies for all, credit applications should account for this inevitable variance instead of blindly following a one-size-fits-all approach. Application templates can be defined by bespoke business rules that are based on the client’s size, type, credit limit, and credit history, as well as the product, the market, and so on. Moreover, many solutions available today allow templates to be easily refined or built without writing code so changes can be quick and sustainable, and templates can evolve as required.

-

Using Modules in Applications:

Refer-backs are unavoidable in complex application, but the back-and-forth between application modification approval can be smoothed by breaking the application into modules to simplify the rework. Approved modules can be sent forward for processing, and the remaining modules sent back for revision, which declutters the rework and supports parallel processing.

-

Auto-sourced Data Pre-population:

– Internal Systems: Banks carry a wealth of data on clients and prospects that usually reside across key systems like customer relationship management (CRM) and

onboarding. Today’s solutions can leverage this data for credit applications by integrating it across systems, enabling automatic data extraction.

– Third-party sources: A wealth of public data can and should be leveraged for credit evaluation. Today, off-the-shelf solutions are primarily focused on integration with credit bureaus for ratings and credit reports. This is an area of rapid growth with much more to follow.

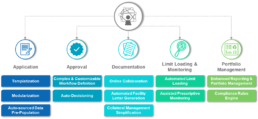

Figure 4: Primary Nodes of Digitization Within Commercial & Corporate Banking

AUTOMATE OR FACILITATE APPROVALS

Credit approval has seen momentous development in recent years. Given the involvement of high-risk, high-value transactions in wholesale banking, there is still hesitation in automating approvals. Technology can not only help to automate the decision but can also facilitate workflows for elements that continue to be manual:

-

Complex and Customizable Workflow Definition:

Workflows in legacy systems often break down in processing applications that require multiple iterations and approvals; systems don’t know how to redirect the workflow, and the process becomes manual.

Like application templates, workflow can be defined without any coding; process owners can tweak and refine workflows as their understanding grows, and common hurdles can be built-in when they’re identified.

Specific workflows can also be defined that correspond to each application template, account for nuances around each market/product/client segment combination, and enforce service-level agreements (SLAs).

Solutions may also support collaboration by incorporating digital committee’ meetings, which can be auto-scheduled based on the definition of manual-approval workflows.

-

Automated decisions:

Automating decisions has the potential to

– Reduce credit TAT to a matter of days or hours, especially for smaller loans

– Enable more consistent, arguably fairer, decisions

– Reduce FTE requirements

Even so, widespread adoption of algorithmic decision-making has not been realized. Many solutions carry simplistic, customizable decision-making capabilities that focus on defining a clear hierarchy of rules. These solutions can facilitate quick decision making for smaller products and redirect to a manual approver when the rules fail.

Documentation is one leg of the process which can benefit from a specialised tool.

BRING DOCUMENTATION ONLINE

Often neglected because of the seemingly rudimentary nature of the task, documentation can turn into the biggest bottleneck in the value chain owing to multiple stakeholders, back-and-forth client negotiations, and exchanging documents into the dozens. Technology today can help smooth the process in several key ways:

-

Collaborating and Negotiating Online:

Online document exchange with clients has a tremendous impact on the client experience, so given the limited opportunities to differentiate oneself, this capability is key. Internal exchange of documents is also often done manually, causing inefficiencies in already complex workflows while masking the point at which the process breaks down. Bringing documentation online can help to orchestrate the process, define workflows, and maintain SLAs.

-

Automating Generation of Facility Letters:

Drafts of facility letters can be generated automatically using information captured from credit applications and customized to the market/client/product type. Without automation, the manual rework and review required can span several days. Automation eliminates not only manual editing and customization but also the need to have multiple levels of internal approvals, barring exceptional circumstances. Comprehensive sanity checks can be pre-baked into the business rules.

-

Simplifying Collateral Management:

Present-day solutions can simplify collateral management by automatically generating the list of documents required and issuing reminders about when these documents should be renewed or manually verified.

Documentation is one area where one may leverage a separate solution, assuming it is fully integrated into the origination platform. In large banks, documentation requirements extend far beyond the credit organization to such departments as legal and compliance. While the documents themselves often differ for different user groups, the underlying functionalities overlap considerably. In this case, having documentation capabilities buried in a credit system (or worse still, in multiple systems disparately) could be highly inefficient.

Documentation is one area where one may leverage a separate solution, assuming it is fully integrated into the origination platform. In large banks, documentation requirements extend far beyond the credit organization to such departments as legal and compliance. While the documents themselves often differ for different user groups, the underlying functionalities overlap considerably. In this case, having documentation capabilities buried in a credit system (or worse still, in multiple systems disparately) could be highly inefficient.

STREAMLINE FUNDING, MONITORING AND PORTFOLIO MANAGEMENT THROUGH COMPREHENSIVE INTEGRATION

Given the relatively small TAT associated with this step, it is often neglected. However, as credit moves toward its next chapter, nothing can be left on the sidelines:

-

Automated Limit Loading:

Solutions can automatically publish data from applications to product-servicing platforms to generate operational efficiencies. Many solutions come with both credit origination and loan servicing modules. Although it’s not always desirable to leverage the same vendor/platform from origination to fulfilment, doing so can ensure smooth and reliable data transfer, enhance continuity, and enable E2E loan tracking. However, given the agility of today’s systems, it’s certainly possible to leverage separate solutions.

AI is Corporate Banking’s best bet at achieving end-to-end automation.

-

Assisted Prescriptive Monitoring:

Automatic reminders for updating documents and covenants and auto-alerts for breaches or suspicious activity can help improve monitoring efficiency. Significant progress is happening here, as the capabilities offered today represent only a portion of what we expect to see in the next three to five years.

-

Enhanced Reporting and Portfolio Management:

Key functionalities supported by well-integrated systems include:

o Command-based, automated ad-hoc and scheduled reporting

o Lifecycle tracking of loans

o Consolidated views on dashboards

o Customizable risk-analysis modules to help assess risk exposure and issue alerts or notifications based on findings

-

Compliance Rules Engine:

An overarching engine can help reduce the involvement of compliance staff, thus reducing the chance of manual errors. In the evolving regulatory landscape, such a compliance engine will be invaluable in enhancing large banks’ auditability, allowing them to avoid large penalties and run-ins with regulatory authorities.

Where does this all lead to?

The transformation in this field isn’t limited to the momentum we’ve already witnessed. We’ve barely dipped into “the art of the possible.” Banks and providers of credit solutions haven’t finished innovating yet, so where is credit headed next?

LEVERAGING CUTTING EDGE TECHNOLOGIES

Digitization is rampant in the credit space, yet the use of breakthrough technologies like Artificial Intelligence/ Machine Learning is limited. We expect this to change soon:

-

Making Credit Decisions with Artificial Intelligence:

AI/ML can be used to create a decision model that incorporates the knowledge of credit officers while also learning and evolving with every decision, much as a credit officer would. Every new decision acts as a new data point from which the model can learn, so even decisions that are manual today may be automated once the model has learned from sufficient additional data points. In theory, AI/ML can automate a wealth of credit decisions since, as the model “grows,” the size of the clients and products it can handle also grow. Therefore, AI/ML is corporate banking’s best bet at automating the larger end of their credit spectrum, so it presents an opportunity to demolish wholesale credit as we know it. No more will a two- to three-month TAT be acceptable; instead, clients will receive near-instantaneous decisions even for large, complex loans.

AI/ML can not only decrease TAT but also generate savings from operational efficiencies and more accurate credit decisions. Enhanced decision-making will also allow corporate banks to extend more credit, giving them an opportunity to grow revenue.

-

Predictive Analytics for Monitoring:

A significant drawback of legacy procedures that flow into the modern landscape lies in monitoring, which leads to the question concerning how beneficial it is to capture a breach or impairment after it has already been committed. Credit monitoring must identify signs of impending breaches instead of ensuring breaches are identified after they are committed. While anticipating the future will never be an exact science, a predictive approach can help banks focus on minimizing impending losses. The use of AI/ML here can ensure that the accuracy of the predictive analytics improves with time.

The opportunities for AI/ML extend beyond these two use cases, but we expect the revolution in credit to start here. Banks will need to build out their data

science capabilities either in-house or through partnerships with or investment in data science firms. First-movers in this space will have a distinct opportunity to increase their market shares by using the self-learning capabilities of ML to automate increasing numbers of processes and deliver ever-improving employee and customer experiences.

Blockchain can also impact credit significantly, beginning with the syndication and secondary trading of loans before seeping into other spheres. However, its large-scale application may still be some way away, given its somewhat embryonic nature.

AUTOMATING LOW VALUE ADDED BUT CRITICAL TASKS

So much work has been done to automate the process and bring it online—but we’re not at the finish line yet! Some of the tasks that are yet to be automated by off-the-shelf solutions today include:

-

Data Sourcing for Credit Application:

Sourcing of financial information from large playbooks like D&B and tax data from players like Avalara can be used to auto-populate applications. Non-traditional data like borrowers’ account information can also be automatically sourced from players like DecisionLogic.

-

Collateral Management:

Third parties like Blackbook can allow automatic extraction of data on market-valued collaterals.

-

Population of Covenants:

Auto-sourcing of financial data can be extended to automate the updating of financial covenants. Non-financial covenants and transaction behavior can be tracked by leveraging alternate data sources and integrating the credit solution with relevant product-servicing systems.

Each of these tasks is critical, but the value added from performing them manually is low, making them ideal candidates for automation.

INTEGRATING ALTERNATE DATA SOURCES

Disruption can (and, we daresay, will) come in various forms, but given the value of data today, solutions that can use non-traditional data for decision-making may lead the pack in adding entropy to the landscape. We can already see examples of such decision-making in retail banking’s bringing forth new strategies.

Zest Finance is an underwriting platform that banks use. Zest’s models aren’t restricted to traditional assessment methods but scrape public data to use ~20 times the data inputs as traditional methods. Using ML helps improve the accuracy of credit assessment over time. Since credit bureaus cover only ~20 percent of Chinese citizens, JD.com, China’s second largest e-commerce company, leveraged Zest to incorporate non-traditional data like web browsing and order history information into their credit model, helping them to increase their approval rate by 150 percent.

Amazon Lending has been using the big data in its possession to assess sellers’ business and creditworthiness. Once creditworthy sellers are identified, Amazon “invites” them to borrow. (Successful sellers, of course, get better rates.) In doing so, Amazon leverages the data collected from one part of the organization to deliver results in another part of the organization, speaking again to the need for robust integration. Simply having a capable credit solution is not sufficient; improper integration across key systems can prevent the solution from delivering maximum benefits.

Banks are slowly realizing the wealth of data they already have or can get, so the next phase of credit will see monetization of this wealth of data, with enhanced decision-making as a starting point.

STARTING YOUR JOURNEY

How was there room for Coke Zero when Coke Light was already available? How do Pepsi and Coke thrive in the same market? Why do new cola companies keep launching what is essentially the same product with slightly different tastes or recipes? You guessed it: one size does not fit all.

An E2E solution is not ideal for all. Some banks may have a mature decision-making tool, some may have a pre-built workflow tool, and so on. In any case, a review of the E2E credit value chain is imperative to determine where gaps exist and where investment is required.

Whether the credit solution covers all or just a subset of the value chain is less important than the richness of the functionalities it offers. Banks must zero in on the areas that need attention for their specific priorities and go from there.

Businesses have always had to identify the outcome they want to achieve from their credit transformation and put them in order of priority. Improved client experience? Faster turnaround? Increased revenue? Lower costs? Once these priority outcomes are identified, each bank will have its unique set of challenges against these goals. Identifying the challenges will help to pinpoint the capabilities that are best suited to address them.

Once all of these steps are completed, the build vs. buy decision can be made, and the credit transformation can commence. Then it’s “simply” a matter of following through, and the real work can begin!

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.