The BNPL Revolution

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

BNPL payments have gained significant traction in recent years across the globe. Despite its popularity, the market is still in a nascent stage of adoption. Current BNPL spend stands at <US$ 100B annually, compared to over US$ 10T processed by credit cards (1). Today, a large portion of demand for BNPL is being met by pureplay consumer fintechs. Traditional FIs on the other hand have been slow to roll out their version of BNPL solutions.

Amidst the rapidly changing environment and growing demand for BNPL, FIs must quickly define their place in the ecosystem. With increased competition, not offering this capability to customers can become costly in the longer run. Traditional FIs have many inherent strengths including presence of extensive data assets, having deep customer trust and loyalty, among other things, that can help them develop a highly compelling solution.

However, several areas need to be carefully thought through before rolling out a BNPL solution. For example, while historically BNPL has stayed outside the purview of regulations, authorities across the globe have tightened scrutiny over such offerings and are developing governing laws. Many regulators believe BNPL payments are non-customer friendly and encourage high levels of debt among young consumers. Moreover, they come with enormous late payment charges – significantly more than credit card interest payments – and can impact consumer credit scores negatively. Thus, FIs will have to carefully tread on the BNPL path and adopt business models keeping consumer interest and regulatory laws at the forefront. In addition, to truly differentiate their offerings, FIs will need to incorporate best-fit product features, design next-gen customer experiences, and choose the right set of partners from a plethora of merchants to develop a sticky BNPL product.

There is a massive opportunity for traditional FIs, if only they can figure out the best way to tap into it!

Growing Ubiquity

BNPL is gaining strong momentum and fast becoming one of the most demanded financing options. While some call it an alternative to credit cards or a new version of the overdraft facility, BNPL has created a market for itself. Today, pay later solutions are increasingly being used by credit card as well as non-credit card users to finance their purchases. Simplicity of models like ‘Pay in 4’ has helped strengthen the value proposition for such offerings. In addition, several market developments have helped build a conducive environment for BNPL payments e.g.,

Rising e-commerce transactions. Retail e-commerce sales amounted to ~US$ 4.9T worldwide (2021) and are forecasted to grow by 50% over the next 4 years, reaching US$ 7.4T by 2025 (2)

Low penetration of credit cards in several markets. Barring a few mature markets like the US, UK, credit card penetration remains significantly low across the globe. For example, in LAC, on average, credit card penetration accounts for only 15% of the population (3)

Growing mistrust in traditional card financing products. Younger demographics are increasingly moving away from using credit cards due to their opaque nature, ambiguity in repayment schedules and high interest costs on revolving balance.

Moreover, the benefits offered by BNPL to all parties involved (see exhibit 1) has further added to their appeal, including:

Consumer Benefits

Access to easy credit, especially for consumers with limited means/ low credit scores, to make purchases that otherwise would not be within their budget

Repayment convenience via predetermined schedules unlike credit card debt, for which consumers need to stay on top of their own repayment plan

Means to build a credit file for new-to-credit users as some BNPL providers have begun offering programs for users to submit their repayment behavior to a credit bureau

Lower initial cost compared to credit cards as interest rates on revolving balance can far exceed the low/ no APR on BNPL payments

Exhibit 1. Benefits offered by BNPL Payments

Merchant Benefits

Lower cart abandonment and an increase in repeat business as goods and products become more attainable for new customers

Increase in transaction value as existing customers’ propensity to purchase is increased

Easier sales settlement processes as BNPL firms assume the risks of chargebacks and fraud

Access to marketing services via the service provider’s app making merchant’s offer available to consumers

FinTech / Service Provider Benefits

A percentage of the transaction value from merchants

Improved Net Promoter Score by more holistically solving the needs of existing customers

Higher customer stickiness (especially for banks/ traditional players) by providing BNPL within existing product or service flows

A Global Phenomenon

Exhibit 2. Maturity of BNPL across the world

A Different Stroke for Different Folks

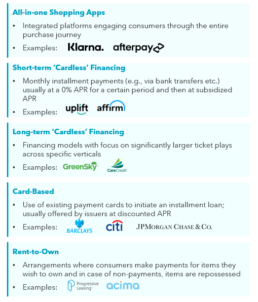

Several models have emerged to support installment based/ split payments. Today, five core models exist (see exhibit 3), differentiated by type of transactions supported by them.

All-in-one Shopping Apps refer to one-stop platforms hosting a diverse set of merchants offering BNPL options. They aim to engage consumers through the entire purchase journey, i.e., from when they decide to make a purchase to the time, they execute it. Players like AfterPay and Klarna are popular in this segment and are focused on building super apps to offer more than just financing solutions.

Short-term ‘Cardless’ Financing Solutions involves using non-card-based methods. This payment method can involve bank transfers and usually entails paying monthly installments at a 0% APR (annual percentage rate) for a certain period and then at subsidized APR. Players like Uplift and Affirm are popular in this category. Such methods cover a broad range of merchants such as electronics, furniture and home goods, sports and fitness equipment, travel etc. Most purchases on these apps are of a lower ticket value.

Exhibit 3. Existing Models for BNPL solutions

Long-term ‘Cardless’ Financing Solutions involves financing models which focus on significantly larger ticket plays across specific verticals. They are popular for industries such as elective and non-elective healthcare, veterinary, power sports, and home improvement etc.

Card Based Solutions involves use of existing payment cards, especially credit cards, to initiate an installment loan. Such a solution is offered by issuers at a discounted APR (less so at 0% APR). While most other BNPL solutions are offered at the time of check-out, most card linked installments are offered as post-purchase installments i.e., once the transaction has been made using the payment card. The transaction value is mostly linked to a person’s credit limit.

Rent-to-Own Solutions involves arrangements where consumers make payments for items they wish to own. In case of non-payments, items are repossessed by sellers. ~80% of use cases in this segment are for categories like home appliances, mattresses, furniture and electronics.

BNPL Ecosystem Today

Today, the BNPL ecosystem consists of diverse participants (see exhibit 4) ranging from pureplay consumer fintechs to other new age neobanks/ loan providers that are beginning to expand their portfolio. In addition, there also exist traditional issuers, payment networks building out their solutions as well as tech providers assisting merchants in launching their programs. Despite emergence of multiple players, BNPL has become mainstream due to the presence of pureplay fintechs like Klarna, Affirm, AfterPay, and Sezzle,etc. Growth of these fintechs have encouraged others around the world, especially in emerging economies, to test out and develop business models for a large base of new to credit customers.

Despite increase in number of fintechs, pertinent challenges have impacted their growth, especially in emerging economies. Lack of data for risk assessment owing to high levels of informalization and limited penetration of credit products has hindered pureplay BNPL fintechs from building borrower credit risk scoring models. Some players are adopting the integrated app route as a way to build a data repository of their users, but at large, most players continue to struggle with underwriting and accurate risk assessment and affordability checks.

Exhibit 4. BNPL Market Map

Financial Institutions & BNPL

BNPL is forecast to continue its rapid growth over the next decade. To continue to maintain prominence and truly differentiate from competition, FIs and traditional payment players need to catch up fast as non-adoption can come at the cost of growth and revenue.

Firstly, card networks and traditional banks risk losing a portion of their revenue from existing customers choosing BNPL products and routing payments via ACH networks/ debit cards. In fact, fintechs have already redirected US$ 8-10B in annual revenue away from banks (5). Additionally, ~40% of existing BNPL users also plan to eventually replace their credit cards (6). Secondly, FIs also risk losing new customers, especially highly engaged younger demographics who find BNPL solutions more appealing due to its faster approval process, flexible financing options, transparent terms, and lower/ no upfront interest fees.

To date, few traditional banks and payment networks have fully established themselves in the BNPL space. For example, while several issuers offer post-purchase installments that help convert a single purchase into equal installments after the transaction has been made, most consumers have not preferred them over financing offered during checkout.

Exhibit 5. FI strengths making BNPL lucrative

In reality, traditional players can develop a stronger value proposition and a more robust offering due to their inherent strengths and long experience in serving customers and navigating regulations. Some of these include:

Pre-existing relationships with customers with detailed understanding of their spending patterns, payments, finances etc. provides banks the ability to offer highly tailored solutions/ experiences (e.g., wider optionality to pay from multiple bank accounts, moving credit card payable amount to BNPL). In fact, surveys indicated that ~60% BNPL users want their traditional FIs to offer such features.

Access to vast data assets on consumers/ merchants via existing products in circulation (e.g., debit, credit cards, merchant accounts) helps FIs have stronger underwriting capabilities and lower defaults due to comprehensive and granular view of consumers

Lower operational costs with advantageous capital costs, deep risk assessment expertise, robust experience in collections etc. lowers risk of default, which is a big pain point for most other providers. Moreover, deeper pockets can enable banks to offer installment loans on potentially far larger amounts than most pure-play BNPL brands.

Banks enjoy high levels of consumer trust via their established brand position and diversified product portfolio. As regulations begin to redefine the industry/ business model, banks will be able to maintain consumer trust easily due to their extensive experience complying with regulations.

Building a Future Proof BNPL Offering

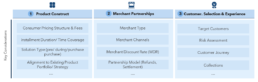

Multiple ways exist for traditional FIs to participate in the BNPL space. From partnering with BNPL providers, to acquiring them or building out their own solutions in partnership with tech providers, FIs need to determine the best way for them to play. It is essential to think through different components of the BNPL solution before deciding on the implementation. From navigating regulations to deciding the right product features to customer experience, FIs need to be on top of different components; some questions they need to answer include:

Exhibit 6. Considerations to build a BNPL Strategy

1. Product Construct

FIs need to plan product functionalities based on existing customer needs and market demand. Competitive offerings should also be evaluated to decide on the right product features. Some considerations include:

What pricing/ fee structure should be adopted? (0% APR vs. a fixed interest rate plan)

At what stage of the consumer journey should the BNPL solution be offered? (pre-purchase, during purchase and/or post purchase)

What coverage period should the BNPL solution support? (# of installments and duration between payments)

How will the BNPL solution align with existing product portfolio/strategy? (e.g., balance between BNPL solution and credit cards offered by an issuer bank)

2.Merchant Partnerships

Merchant partnerships have a critical impact on adoption of BNPL solutions. Getting the right merchant partnerships is crucial to increase usage and create sticky consumer relationships. FIs should focus on identifying the right niche or whitespace in BNPL crowded markets when it comes to tapping different merchant categories. Some considerations include:

Which merchants should be partnered with/ will be eligible for offering consumers the BNPL solution? (merchants supporting low ticket value purchases like grocery and everyday items vs. those supporting larger ticket plays)

What channels will the solution support? (e.g., online websites and/ or physical storefronts)

What will the MDR/ price charged from merchants look like?

3. Customer Selection & Experience

Targeting the right set of customers is key to increase acceptance of the BNPL offering. Moreover, as more players begin to crowd the BNPL space and start offering similar solutions, customer experience will become a key differentiator for success. Offering a smooth and quick customer journey is imperative to retain consumers. Some considerations include:

What customers will the provider target? (e.g., existing customers of merchant/ issuers)

How will credit risk assessment take place? What data assets/ models will be leveraged? Will partnerships with 3rd party providers be needed to enhance data coverage/ credit risk algorithm?

What will the consumer journey look like throughout the purchase lifecycle? (e.g., preapproval process, provision of digital portal for viewing details on installment plans, auto pay features etc.)

`How will collections be optimized? What channels/ methods will be used? (e.g., digital reminders, blocking purchases on select merchant sites etc.)

In addition to the above, another crucial consideration involves navigating through existing as well as potential regulations. Authorities like FCA cracking down on firms like Clearpay, Klarna, Lazybuy and Openpay in the UK for their unfair and unclear terms. Several markets are planning on rolling out laws soon. Hence, it is essential to make adjustments right away to best meet expected regulatory requirements. Regulators’ main concern includes non-consumer friendly practices, improper disclosure of terms and conditions, and increasing debt burden for young consumers. To avoid legal action, service providers must be transparent with consumers at the time of extending the service. They should lay out all terms and conditions and associated implications including penalties upon non-payments, impact on credit scores etc. to help users make an informed choice. In addition, they must carry out extensive checks to ensure credit is extended to only those consumers who have the means and ability to repay. Today, a lot of BNPL providers conduct soft credit checks that are unreliable and can result in higher defaults.

In Closing...

BNPL has emerged as the go-to source of financing for customer purchases worldwide. This is driven by rising aspirations of younger consumers, strong growth in e-commerce, and limited access to traditional financial products, among other things.

While pureplay fintechs have played a pertinent role in popularizing BNPL payments and have seen massive consumer adoption, their business models have not fared well under regulatory scrutiny. Loopholes in customer centricity and risk management may make such solutions unviable in the future. On the other hand, FIs have been slow to roll out solutions and their current post purchase installment plans have not received much customer love.

With the rapidly growing consumer demand and recent setback experienced by BNPL players, traditional FIs must quickly develop a future-proof BNPL strategy. This includes developing business models in line with current and future regulations. Alongside, careful thought needs to put on deciding the right product features, choosing the right target customers, designing a customer journey, and partnering with the right merchants to truly create value for consumers and drive lng term usage and stickiness.

__________________________________________________________________________________________________________

- ACI Worldwide ‘Keeping Pace with Innovation in Real Time Payments

- Visa 2020 Investor Day Presentation

- Modern Treasury ‘Real Time Payments around the world

- WorldPay

- BankingDive, ‘Banks risk 5% loss in revenue to fintechs if they don’t change’, 2020.

- CRResearch, 2020

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.