Time To Get Your Game On!

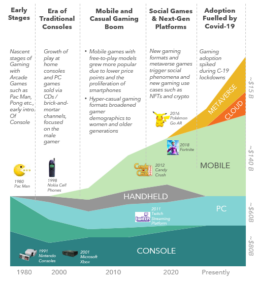

The gaming industry is a ~$300 Billion (1) giant, with a third of the world’s population playing games. The industry has now surpassed the movie and music industry combined. Highest grossing games titles such as the Call of Duty Franchise and Grand Theft Auto V are recording higher sales than big blockbuster hits. Gaming has evolved over time, coming a long way from its traditional arcade days, to grow into a social phenomenon. Several innovations have contributed to its adoption. From the classic arcade games such as Pac Man and Pong, to the original consoles such as the Odyssey and Nintendo 64, and to PC games, this industry had traditionally catered to the stereotypical middle-aged male gamer. However, the proliferation of smart phones and mobile games gave rise to casual and free-to-play (F2P) gaming formats that catered to broader demographics. Access to faster and more reliable internet sparked the shift to digital-first gaming formats and cemented mobile games as the preferred channel. Next-generation gaming titles, channels, and platforms in the Metaverse (e.g., Axie Infinity) are still in nascent stages, but are expected to redefine gaming once again.

Mobile gaming is giving rise to newer formats including social gaming, play-to-earn, metaverse & cloud gaming. An increasing number of people now participate in e-sports as players or viewers.

Platforms such as Twitch, Discord, Steam etc. along with the creator economy have given rise to gaming communities which has further increased popularity of social gaming. Gamers are spending more time than ever on these platforms playing, viewing, trading, and socializing with their peers. Some of the most popular streamers have accumulated 20M viewership hours and 18M followers.(2)

Exhibit 1. Evolution of Gaming

Era of Record Growth

The steep growth of gaming has been fueled by several factors:

- Pandemic: The pandemic brought gaming to a tipping point due to increased digitization & need for social interaction

- Smartphone & Internet Proliferation: Consumers now have more gamer-friendly phones with better access to faster internet services such as 5G

- Social Games: Gamers now have access to better games & formats that before. Rise of social & hyper gaming formats have led to expansion in demographic appeal

- Digital Distribution: Games are not distributed online increasing ease of access to different gaming formats

- Acceptance of Local Payment Methods: Most gaming platforms are now diversifying their acceptance solutions to include APMs and local payment methods such as wallets, prepaid cards etc.

- Creator Economy: There is a rise in live streaming & e-sports viewership due to the increase in influencer/ creator led marketing

The gaming industry now presents a largely untapped opportunity for

Financial Institutions. As gaming diversifies from traditional channels such as mobile, PC & Console into cloud gaming,

Augmented Reality & Metaverse, the opportunities to monetize on sizeable payment flows by targeting a new younger customer segment increase significantly. There are successful examples from around the globe for gaming-related payment products not limited to but including cards, credit solutions, alternative payment methods etc. designed especially for gamers.

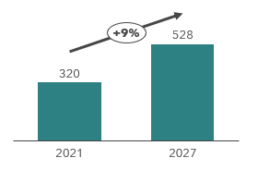

Exhibit 2. Global Gaming Revenue (in US$ B)

Designed for Everyone

The number of gamers worldwide is expected to reach ~3.8 billion by 2028. While gaming is the most popular leisure activity for Gen Z and Millennials, an increasing number of Gen X and Baby Boomers are taking up gaming making the gaming audience extremely diverse.

Different generations have different motivators for playing games, for example, Gen Z plays to compete & develop skills while Gen X plays to unwind. The motivators also translate into different spending habits, time spent and subsequently different opportunities for each generation of gamers. With the popularity of newer gaming channels such as mobile and metaverse-related games, gaming companies are increasingly experimenting with newer types and genres including strategy, puzzles, sports, shooter, survival, rhythm, musical etc. to target new segments. These newer models also cater to the female demographic, with ~48% of gamers identifying as female in 2022. Moreover, gamers are spending more time in gaming platforms then ever. Individuals now also play to stay connected with their friends and family while enjoying their leisure time.

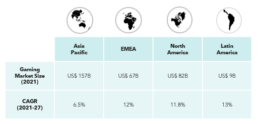

Exhibit 3. Regional Gaming Revenue

Exhibit 4. Gamers by Generation (3)

Hence, online multiplayer games offering immersive experiences are gaining popularity among gamers of all age groups. Each generation of gamers has some attributable traits:

1.Gen Z: Comprising the highest share of hardcore gamers, Gen Z spend the highest time gaming split mostly equally across Mobile, Console & PC. They show the most interest in Metaverse, which is expected to define the future of gaming, due to an underlying interest in social activities such as getting together with friends & hosting events.

Most popular games enjoyed by Gen Z includes Battle Royale, Sandbox & other multiplayer online battle arena games & non-crypto metaverse such as Roblox & Fortnite.

2.Millennials: As most millennials are social gamers with limited prevalence of hardcore gamers, they spend a considerable amount of time gaming across Mobile, Console & PC. They have strong preference for role-playing, strategy & adventure gamers.

3.Gen X: Most Gen X consumers are casual gamers and prefer playing gamers on mobile platforms, followed by PC and lastly console. They are casual players who like to play puzzle, shooter or sports gaming genres.

The Next Big Thing In Gaming- The Metaverse

The global metaverse market is expected to reach US$ 430 billion in 2027, growing at a CAGR of 47.6%(4). This growth significantly contributes to the increase in uptake of online video gaming as a direct consequence of Augmented Reality/ Virtual Reality technologies. While Metaverse has many use cases including social interactions, entertainment, social commerce etc., gaming remains the most lucrative use case that is being adopted by millions of users worldwide as a gateway to the Metaverse. The virtual gaming world has been backed by blockchain technologies including multiplayer & interactive games.

The introduction and rise of cryptocurrencies have enabled a change in the gaming paradigm. Centralized metaverses such as

Fortnite were the latest evolution in the gaming industry up until

a few years ago. Decentralized Metaverse is now expected

to define the future of gaming as the digital world gets decrypted.

Metaverse has become popular & is expected to grow because of the following gaming opportunities presented within it:

- Social Gaming: Metaverse is a social platform where multiple people can engage with each other at once promoting massive multiplayer games on the metaverse

- Play-to-Earn: Earning while playing is probably the biggest motivator/ incentive for gamers. Players can cash in profits via NFTs, competitions, in-game assets etc. which can be exchanged for cryptocurrencies or fiat

- In-Game Assets: In game assets are items such as skins, avatars and other goods that enhance gameplay. The in-game assets help gamers compete and win against other players

As the popularity of Metaverse rises, gaming revenues are expected to rise significantly both in the breadth and depth of new & existing revenue streams. Financial institutions can position themselves as next-gen and benefit from first-mover advantage by entering the Metaverse.

Exhibit 5. Development of Gaming & Metaverse

The Complex Ecosystem of Payment Flows

The Gaming ecosystem broadly consists of three main categories of stakeholders, i.e., (i) Gamers, (ii) Gaming Companies and (iii) Gaming Communities, each with multiple revenue streams. Understanding each stakeholder & payment flows will be foundational in capturing gaming-related payment volumes & facilitate meaningful partnerships.

(i)Gamers: Financial Institutions are capturing gamers’ payment flows by introducing gamers’ cards, alternative payment methods such as prepaid cards, wallets etc. that can be easily integrated on online gaming platforms & used for P2P transfers

(ii)Gaming Companies: Financial Institutions have been partnering with gaming platforms to provide acquiring solutions, pay-out automations, seamless payment journeys etc.

(iii)Gaming Communities: Like gaming companies, gaming communities such as e-sports/ streamers, creators etc. have regular gaming in-flows. Financial institutions have been providing acquiring solutions, seamless checkouts etc. in addition to managing commission pay-outs

Exhibit 6. Gaming Ecosystem (5)

There are some gaming payment flows which are expected to record stronger growth compared to others, such as –

In-app purchases (IAP): As mobile gamers dominate gaming, in-app purchases are expected to record strong growth. IAP allow users to

pay real money for features or items while playing a mobile game. Depending on the game type, that can be anything from extra

lives, coins, weapons, unlocking levels, etc.

Subscriptions: As cloud gaming formats increase, subscription-based games & e-sports tournaments are expected to gain popularity. Subscriptions are fixed fees paid to access a game at regular

intervals. Platforms such as Xbox Live, Twitch (Streaming Platform)

offer subscriptions to gamers

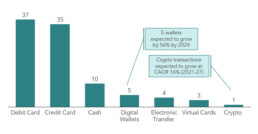

Preferred Payment Methods

Gamers are largely dependent on debit/ credit cards for making their purchases, however, alternative payment methods such as E-wallets are gaining preference. Most gamers make online transactions for in-app purchases to level up or buy skins, avatars, game currencies etc.

Exhibit7. Gamers’ Preferred Payment Methods (6)

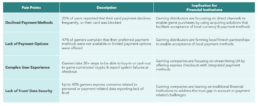

Payment Pain Points

Payment methods amongst gamers are faced by multiple pain points that act as significant blockers for gamers who want to spend on games. Financial institutions can act as a catalyst in addressing payments-related points of gamers by adding legitimacy and efficiency to gaming platforms thereby driving spend.

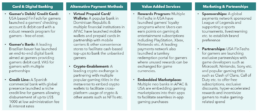

Monetizing the Gaming Ecosystem

Multiple financial institutions, especially new age & neo-banks around the world are introducing retail payments offerings designed for gamers. These offerings are designed to increase existing gaming payment volumes or create new payment flows. While most offerings can be classified into payment products, there are some collateral offerings such as gamification of digital banking, loyalty programs among other value-added services that have a positive cascading effect in driving payment volumes. While alternative payment methods can be used to tap unbanked & younger generations, traditional banking products can be used to drive additional payment volumes. Select product opportunities include–

Every Financial Institution Needs a Gaming Strategy

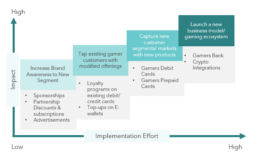

Based on examples of global players’ & their gaming-related offerings, there are multiple opportunities that financial institutions can capitalize on after identifying their objectives, strategic appetite & organizational capabilities. Financial institutions will have to look inward to establish their goals & potential outcomes from gaming related products while aligning with their current strategy.

There are multiple in-roads to capturing payments in gaming, each with different levels of ease of implementation & potential impact. Initiatives to tap into the gamers’ segment can vary from something as low effort as a marketing campaign via partnerships to increase brand awareness or a more radical approach of introducing a new product such as a gamers debit card which will drive significant impact.

As a most recent example of introducing a gamers’ debit card, USA based FinTech for gamers launched a gamers’ checking account & debit card with a robust rewards program for gamers – free of cost. Users can earn points on gaming & entertainment subscriptions including PlayStation, Xbox, Nintendo, EA Play, Amazon Prime and redeem points using an in-app marketplace on items such as video games, gift cards & hardware. All of this has been facilitated through partnerships with popular gaming companies such as Call of Duty, Logitech, GameStop, Nintendo etc.

Exhibit 8. Potential Gaming Strategy(s) (5)

Rewards extend to gamers’ lifestyle based spend including entertainment, restaurants, retail via partners such as Best Buy, Dominos, Spotify, Netflix etc. They recorded more than 50,000 waitlist participants in their initial days of public beta launch.

A top-tier Brazilian commercial bank introduced a net new business model and banking service under another name – designed especially for gamers. They launched a suite of products for gamers from a checking account, a credit card, a debit card and online gamers communities. They facilitated this via multiple partnerships with top gaming titles in the region, an exclusive partnership with an E-Sports platform and integrations with local payment methods such as Pix. They also developed an in-app gaming marketplace with 100+ brands to facilitate easy rewards redemption and seamless purchases. In a short span of time, the bank has managed to establish brand preference among gamers and partnerships with 20+ organizations such as Gamers Club, Nuuvem, Acer, Loja Flakes, Ubisoft, PlayStation, Xbox etc.

There are some key considerations that FIs need to consider while creating a go-to-market strategy for gaming. There are multiple pillars of decision making to build a successful gaming strategy –

Exhibit 9. Pillars of decision making to build a successful gaming strategy (5)

In Closing...

The Gaming industry currently presents a huge opportunity for banks and financial institutions. Gaming has continuously evolved in terms of formats and revenue from traditional arcade and console gaming to mobile, cloud gaming, and the metaverse. Smartphone and internet proliferation has led gaming to become a social phenomenon with digital distribution and adoption. There’s now a game for everyone.

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

With a plethora of largely untapped opportunities in the gaming industry, its time for financial institutions to start developing their gaming strategy in alignment with their objectives and capabilities. The success of financial institutions will be dependent on the development of a cohesive go-to-market strategy for gaming products of suitability, complete with competitor analysis, target market needs study, product design, and effective implementation after taking into account all the necessary pillars required to not only launch a successful product but also beat competition.

__________________________________________________________________________________________________________

- Newzoo

- Newzoo

- Newzoo Generation Report

- Global Newswire

- Kepler Cannon Research

- Ebanx

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.