THE PICTURE SO FAR

“The broader challenge is to lay down a longer-term strategy that endures after the crisis of the moment’ – Fareed Zakaria

The COVID-19 pandemic has taken thousands of lives, overwhelmed healthcare systems, upset supply chains, and distressed economic activities worldwide. For the the global insurance sector, the impact will be profound. The pandemic’s multi-faceted nature has impacted several coverage lines such as business interruption, travel, cyber liability, trade credit insurance, event cancellation etc. Apart from operational challenges, mid-to-long term profitability, portfolio returns, claims and recent business launches are adversely affected. In addition, actuarial and financial assumptions must now be re-set.

Although the industry is likely to survive the crisis as it has in the past (e.g., with SARS, MERS), insurers need to determine how best to meet the rapidly evolving needs of their customers, agents, and staff with products, financing, sales, and service that are better suited for the next normal. In this paper, we broadly discuss the impact of the pandemic on insurers, compare China and U.S.’s response to date, and suggest ideas for building sustainable and resilient management systems.

IMPACT ON INSURANCE BUSINESSES

I) Life and Annuities Data

Challenges to Getting New Business

Economic downturn, rising unemployment, and reduced incomes have lowered consumers’ willingness to spend. Thus, new business volumes, especially for high premium, complex annuity products, have dropped significantly. Players like Prudential saw their Annual Premium Equivalent (APE) sales in Asia drop by 34% in the first half of 2020, while AXA saw its life & savings gross revenues fall by 8% during the same period.

Given the interest rate volatility, carriers have taken restrictive stances on pricing, underwriting new policies, and sales of long-duration products. Further, social distancing, and stay-at-home orders or lockdowns, has meant that insurance agents are unable to visit clients. Customers are being re-directed to digital channels for information, service and queries, where possible. This has caused delays in new business application processing, reduced underwriting capacity and disrupted in-person activities such as paramedical exams, collection of medical records etc.

Impact on Existing Operations

Remote working and reduced staff in offices has incumbered claims management, call center operations, and policy administration tasks. For instance, call centers are finding it hard to maintain service levels due to increased call volumes from customers wanting to understand existing policy coverage, or ongoing claims.

Actuarial and Financial Implications

Markets have reacted strongly to the rapid spread of virus, with decline in interest rates, equity markets and widening of credit spreads. This has led to significant product, pricing, and balance-sheet challenges for insurers. Market volatility impacts earnings from invested assets as well as sales of rate sensitive products (e.g., income annuities). This combined with reduced premiums from existing policies, payment holidays, rebates from many insurers and high payouts, adds strain to capital positions. Treasuries will need to assess and provide for increased cash flow impacting financial projections. Actuaries will need to determine how to re-set assumptions in the face of market volatility, changing policyholder behavior and risk profile.

II) Property & Casualty

The pandemic has impacted several lines of commercial, personal and specialty insurance.

Directors and Officers insurance will see increased claims and litigation as business leaders may challenge the management for not developing adequate contingency plans, negligence and failure in disclosing all risks associated with pandemic on the company’s performance.

Cyberinsurance will grow due to increased vulnerability from remote working. Zurich Insurance Group, for example, has partnered with cyber-security company CYE to launch an offering that helps businesses deploy cyber risk programs, including closing security blind spots, reducing the risk and impact of security incidents. Workers’ compensation will be impacted by both C-19 infections as well as resulting economic downturn. The number of unemployed Americans increased by more than 14M, from 6.2M in February to 21M in May 20202. This, along with WFH measures and reduced work-related travel will contribute to overall decline in frequency of claims. Businesses, many of which are now operating at a lower capacity, will also have reduced the need for workers’ compensation products.

Specialty lines such as construction have faced a slowdown due to temporary suspension of construction projects. Event cancellations have been a source of large losses for the insurers. The Olympics serve as the most notable and extreme example of a significant event cancellation. While current discussions seem to indicate that it is more likely to be postponed to 2021, a cancellation would cost insurers around $2B3 with reinsurers like Swiss Re and Munich Re incurring $250M and $300M in losses4, respectively .

Personal lines of insurance such as Auto insurance saw disruption in new business as the lockdown brought new auto sales to a standstill.

Further, shelter in place orders reduced motor vehicle usage and hence motor insurance claims. ‘Give Back’ programs became frequent due to low loss ratios. The ease of spring lockdowns is driving new auto sales and premiums; however, it still remains below pre-Covid levels.

Global C-19 related losses in P&C are estimated to be ~$55B. This is slightly more than losses from natural catastrophes in 2019.

III) Health

Health insurance premiums are expected to grow as the pandemic has increased awareness about the importance of health coverage. AXA, for example, saw a 9% increase in health insurance revenues in Q2 2020, Prudential also reported that seven of their Asian markets saw an increase in their health insurance, generating 69% of their overall new business profits6. On the other hand, many Americans have been left jobless due to the pandemic and subsequently lost their employer sponsored health insurance. Some of these people will qualify for Medicaid or purchase coverage through the Affordable Care Act (ACA), but others will likely become uninsured.

This is critical to address, as the uninsured will incur significant C-19 related expenses.

INDUSTRY RESPONSE: CHINA

“When written in Chinese, the word ‘crisis’ is composed of two characters. One represents danger and the other represents opportunity” – John F. Kennedy

As insurers around the world scramble to thrive in the fast-moving pandemic era, all eyes are on China to see if there are some lessons that could be applied in their home countries. Although China claims a significant decline in new cases since March 2020, perceived risk of contracting C-19 remains high, with certain economic verticals such as travel and tourism continuing to face restrictions.

The five registered insurers in mainland China, including China Life Insurance and the People’s Insurance Company Group of China (PICC), benefited from China’s gradual return to work following the worst of the C-19 outbreak in February. In Q1 2020, combined premium income of the top five insurers totaled $134B, marking a year-on-year rise of 4%7. Majority of this growth can be attributed to the companies’ move to offering online services during the pandemic.

China Taiping’s chairman Luo Xi stated in March, that he expected the company to meet its 2020 business targets. China Life sounded a similarly optimistic tone when presenting its expectations for 2020.

The Chinese life insurance market is expected to remain strong, largely driven by a growth in household incomes, relatively low penetration rate, and a need for securing the future. Swiss Re expects global insurance premium volumes to recover to pre-C-19 levels in 2021, driven primarily by emerging markets, led by China.

Exhibit 1 shows some of the common measures adopted by Chinese insurers to combat the crisis.

Exhibit 1: Measures taken by China’s Insurance Industry

Adoption of digital tools and processes

Ping An, one of the leading insurers in China, has been particularly innovative in its response to the coronavirus crisis. Ping An’s Good Doctor, China’s largest mobile internet telemedicine platform, added nearly 350M users as of June 30. Several Chinese carriers have also found that digitizing their processes led to an increase in prospective customers.

Insurers adopted the use of video and messaging apps to enhance the customer experience. These apps facilitate customer authentication, digital face-to-face meetings, completion and submission of insurance applications. China Life, for example, strengthened online services and promoted their app. The app processed 2.8M client services and achieved an online service rate of 92% (yoy increase of 32%) in February.

The pandemic raised an unexpected sense of urgency to purchase insurance, paving the way for players to tap the vast underpenetrated market via contactless, online channels. Tencent WeSure, for example, added 25M new active users. It simplified the buying process for customers by offering curated portfolios based on individual needs. The company utilized the power of social media and ‘word of mouth’ to drive more revenue. In fact, ~33% of WeSure’s revenues were generated from social referral, 3x higher than industry average.

Investment in med-tech capabilities

Ping An’s Smart Healthcare provides comprehensive services like AI based disease prediction, medical image recognition, and AskBob, a treatment assistance tool to over 17K medical institutions. They also launched a C-19 smart image-reading system earlier this year to assist doctors with fast C-19 diagnoses. In 15 seconds and with 90% accuracy, the system is able to analyze multiple CT scan images of a single patient and measure changes in lesions11. Offering their services to over 1,000 medical institutions, Ping An’s system has been able to help doctors track the development of the virus in patients and thus formulate treatment quicker and more effectively. China Pacific Insurance Company (CPIC), another leading insurer with over 139M users, started applying a voice analytics technology and emotion detection solution to uncover fake death claims and reduce life insurance fraud.

Subsidized coverage

Chinese insurance carriers provided healthcare professionals and first responders with free or subsidized coverage. Over 70 of the country’s largest insurers offered free coverage for all frontline workers. SCOR, a global reinsurer, in collaboration with Nankai University, launched an insurance information platform to help frontline workers stay aware and informed of their rights and access coverage most suitable to them. Insurers also began offering special coverages and cash benefits. China Taiping Insurance ran a complimentary financial aid campaign offering a lump sum payment of $1,000 upon diagnosis of C-19, daily hospitalization benefits of $100 a day up to 30 days, and an additional bonus of $1,000 upon full recovery from May to July.

Affordable policies

The Banking and Insurance Regulatory Commission of China fast-tracked approval for new low-cost insurance products. These insurance products have lower premiums than standard critical illness products and are thus expected to expand the reach of insurance carriers. China Taiping Insurance is offering deferred premium payment plans for its existing life and general insurance policy holders affected by C-19, so they remain protected during the pandemic.

Overall, China’s insurers have established themselves as pillars of support during the crisis, accommodating their customers’ needs, prioritizing their convenience, with easy accessibility and enhanced products.

INDUSTRY RESPONSE: U.S.

Being the biggest economy in the world, it is not a surprise that the U.S. has struggled to revive operations while keeping safety measures in place. Insurers were hit hard in the first half of 2020, especially those writing events cancellation and workers’ compensation. P&C insurers in North America, for example, witnessed first-half losses of $6.8B related to C-19 and a drop in premium volumes14.

Exhibit 2 shows some of the common measures adopted by U.S. insurers to combat the crisis.

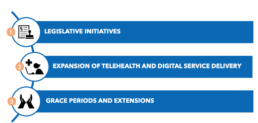

Exhibit 2: Measures taken by the U.S. Insurance Industry

Legislative initiatives

Insurers experienced an unprecedented number of new laws, regulations, directives and orders from the federal, state, municipal authorities related to the pandemic . Examples include, Families First Coronavirus Response Act, CARES Act, Paycheck Protection Program, Health Care Enhancement Act. These governmental actions required insurers to waive member cost sharing associated with C-19 testing and treatment, provide coverage for additional C-19 related services, allow longer renewal of prescriptions, extend grace periods for payments of premiums, facilitate, accelerate or advance payments to health care providers etc.

The crisis also showed how social pressure on the industry to pay claims can become a key factor in driving losses. In case of Business Interruption coverage, for example, 8 US states introduced legislations ‘which would require insurers to pay claims, mainly to small businesses, despite exclusions’15. At a fundamental level, the industry is not currently designed to address such widespread problems, if insurers had to pay all the interruption claims, the industry would most likely go bankrupt.

State governments and regulators in numerous states also expanded the scope of workers compensation coverage to include cover (medical expenses and lost wages) for emergency responders, healthcare workers and in some cases any worker deemed essential that contracts C-19. In California, employees who tested positive for C-19 within 14 days after working at their place of employment were eligible for workers compensation.

Expansion of telehealth and digital service delivery

Because of the need to limit in-person appointments while maintaining access to care, telehealth has gone mainstream. Several US states have implemented measures to ensure that coverage for telehealth is equivalent to the coverage provided for physical consultations and have eliminated barriers to accessing telehealth services (including the scope of medical services that can be delivered through telehealth).

Players like Cigna and Anthem expanded telehealth coverage to include mental health support and some physical, occupational, and speech therapy while waiving costs for in-network telehealth visits.

Many US state insurance supervisors are encouraging digital service delivery. Allstate anticipates a majority of auto insurance claims to be filed via their Virtual Assist tool, which allows a body shop to create an initial estimate and get approval on supplemental coverage as they repair a vehicle.

Grace periods and extensions

Insurers are offering extensions for policyholders that face difficulties in securing necessary documentation like registration or certification documents. They are encouraging premium payment grace periods (or payment instalments) for all lines of insurance or deferring cancellation of coverage or imposition of penalties for non-payment. For example, Allstate insurance offered customers an extension of auto insurance coverage for those using personal vehicles for commercial reasons. They also gave their customers the option to delay payments with no penalties. Liberty Mutual automatically waived late fees for their customers and continued to provide coverage to those with overdue payments. MetLife also extended premium grace periods, waived late payment fees for their customers, and loosened requirements for claim documentation.

Overall, in U.S., the insurance companies, supervisors (e.g., NAIC) and the government have focused on supporting policyholders by offering financial support in terms of payment deferrals, grace periods, renewal extensions etc. as well as adapting policies to ensure coverage is provided for costs and losses related to C-19.

THE WAY FORWARD

The pandemic has highlighted where the industry can improve and change in order to be able to better handle similar events in the future.

China’s experience shows that the insurance industry’s understanding of digital strategy is deeper than ever. Their rapid innovations, fast launches, use of big data and technology driven initiatives were instrumental in China’s fight against the virus and demonstrate how digitization and telemedicine enabled the companies to rapidly adapt to changed environment.

U.S.’s experience reinforces the need to improve policy design and wordings for business interruption coverages and the realization that a pandemic cannot be covered entirely by private insurers. It raises the importance of introducing public private partnerships that can provide protection against the financial impact of future pandemics. For instance, Pandemic Risk Insurance Act (PRIA) has been suggested in U.S., in which insurers take the first loss, with a federal backstop covering losses exceeding a threshold.

We now discuss how these learnings can be adapted by carriers to build sustainable and pandemic resilient risk management systems (Exhibit 3).

Exhibit 3: How to build a sustainable insurance system

Product Innovation

New types of coverage will be needed, such as parametric policies (which pay upon the occurrence of a triggering event rather than having to claim a specific insured property loss). There will be an increased focus on offering usage-based insurance products powered by sensor-based technologies (e.g., telematics for auto) as well as value-based services in the form of supplementary health products like remote diagnosis, treatment, medical services and pharmaceutical delivery etc.

Hybrid Distribution Models

The crisis has accelerated the digitization of sales channels with agents looking for more support from their insurer in the form of leads, product solutions, tools, and trainings. Agents must be augmented with digital tools and capabilities to enable them to interact with customers via a seamless omnichannel journey. Agents will be able to gain better insights into customer habits and tailor their offerings accordingly. Sales management practices will also need to be restructured in form of new trainings, materials, engagement programs focusing on virtual selling skills, remote advising, e-KYC etc.

Crisis Management Playbook

Risk managers need to update their response playbook based on lessons learned from the crisis. This includes building resilience upfront in the form of sufficient capital and liquidity resources, conducting scenario analysis for both setting and assessing risk appetite in a dynamically changing environment etc. Because pandemics affect so many people and businesses at the same time, they are considered uninsurable. This calls for increased collaboration and partnership between insurers and governments in determining financial protection against this risk.

Streamlined Structural Costs

Insurers must undertake firm wide cost reduction programs (e.g., zero based budgeting) not only to reduce structural costs but also release funds for faster innovation and fuel future growth. They should postpone less critical investments to free up capital and invest across product development (offer parametric policies), distribution (enhanced online capabilities), technology (increase spending on cybersecurity, shift to cloud computing) etc.

Heavier Investment in Data and Analytics

C-19 has further highlighted the need for insurers to streamline, improve and digitize operations and claims functions. Data from internal and external sources including marketing, sales, claims settlement, medical follow-ups, wearable devices, hospital diagnosis and treatment should be utilized to generate real time insights. This will facilitate quantitative models for customer segmentation, dynamic pricing, speed up underwriting and greater product innovation.

Adaptive Talent Management

Given the risk of periodic surges in C-19 infections, many insurers are likely to offer remote working options till mid or end of the year 2021. Insurers must re-think talent strategies to enable effective collaboration and maintain productivity of workers. This will include adapting hiring, onboarding, performance management practices to hybrid/virtual models. Developing interactive virtual programs to impart learning as well as supporting them with right technology tools and infrastructure.

IN CLOSING…

The pandemic has created unprecedented challenges for the insurance industry. P&C insurers have been hit the hardest given event cancellations and business disruptions. Persistently low interest rates has impacted the growth and profitability of annuities and life insurance products.

China’s insurers have stepped up to the challenge by accelerating digital adoption, improving med-tech capabilities for efficient screening, online diagnosis and treatment of patients. U.S. insurers, on the other hand, have focused on dealing with new legislations on waiving member costs, offering coverage for C-19-related services etc. Like their counterparts in China, they have also expanded digital service delivery and invested in telehealth services.

Even though the pandemic has caused severe disruption and economic fallout, it is also acting as a catalyst for change prompting insurers to accelerate their digital transformation agendas and develop bespoke, data driven product offerings to fuel growth.

Read More

Rethinking the Future of your Business

The economic climate is becoming increasingly uncertain with cautionary signals of recession, along with inflationary pressure, fluctuating currencies, and uncontrollable impact of geopolitical events. Firms need to proactively take this opportunity to refocus their future investments on high value, high potential business lines.

Technology and Healthcare

Data production in healthcare occurs in different volumes, velocities, and formats by multiple sources – EHR, diagnostic, imaging, claims, billing, medical devices to name a few.

Enterprise Cyber Resilience in a Hybrid World

Cybersecurity incidents are also not only a threat to corporations’ internal operations and bottom line; customer personally identifiable information and financial data is also at serious risk of exposure and misuse, in turn impacting customer perception and long-term brand loyalty.

Finding Growth in US Insurance

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Data-Driven Post-Merger Integration

A common misconception is that revenue synergies are illusive or “icing on the cake”, primarily because they are more challenging to quantify.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

Platformization of Health Tech

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously

Are Your Vendor Risks Under Control?

Investing in vendor risk management today can secure a future brimming with cost-effective, secure, successful and trust-worthy partnerships.

(AI)ntelligent Procurement

In a competitive business environment, high-performing CPOs are 18x more likely to fully deploy AI/cognitive capabilities. This typically leads to 92% faster demand forecasting, on average 350 man-hours are saved through automation, and there is a potential for 24/7 operations

Realizing Your Workforce Strategy

Organizations are now recognizing the limitations in their workforce programs, so are making a concerted effort to develop a contingent workforce strategy, consolidate their master vendors/staffing agencies, and extract maximum benefits from the program.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Getting the Basics Right

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Embracing Open Banking

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

Ensuring Loyalty of your Prized Clients

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Cloud-Native Paradigm

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Business Analytics in Pandemic Times

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Reshaping Wealth Tech

Before the Covid-19 inducted recession, the wealth tech sector was already experiencing a slowdown - both in the number of new startups and total capital raised. Now more than ever, investors and operators must be bold in re-inventing their Firm's long-term value proposition.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

How to Thrive in the New Normal

Now that Business As Usual is unusual, leaders are forced to re-imagine business models and build ‘winning strategies’ - to not only survive the pandemic but also emerge as successful change-makers, shaping an altered business reality.

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Trends in Digitalization of Insurance

For some, Insurance might seem a monolithic industry, but for the ones keeping a close eye on it- Insurance is revamping itself faster than ever!

From days when underwriting a simple policy would take weeks and months, to now when it can be done in seconds with a simple ‘selfie’ - there seem to be no bounds in the future of this industry.

Customer Engagement Index

While firms have found tremendous success in using these loyalty metrics to successfully grow customer relationships, they are lagging indicators and provide little help in providing immediate insight into whether or not improvements and initiatives are moving the needle.

Strategic Sourcing of a “Difficult” Spend Category

Some clients have even deemed spend reduction in procurement categories like legal services, where recourses and expertise are concentrated within humans not technology, to be intractable. At Kepler Cannon, we continuously challenge these sorts of conventional wisdom.

Third Party Information Risk Mitigation

It is well known that one way to make better predictions about how your customers, distributors and suppliers will behave, is to augment your own data with that of third parties.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Reducing Strategic Over-Dependence on IT Vendors

Over time, many firms realize that they have become so reliant on vendors/contractor for critical knowledge on key applications, that they have, in fact, ceded control of those applications to the vendors.

Are Blockchains Evolving Like Securities Exchanges?

Driven by data security concerns, a majority of financial institutions are now looking at so-called private or hybrid blockchains, rather than fully decentralized public blockchains (like the blockchain used for Bitcoin)

How Global Resourcing May Be Killing Your Company’s Efficiency

As global firms respond to the post-Great Recession regulatory and economic realities, efficiency of the back-office has become critical to ongoing success.

Third Party Vendor Risk – A Continuous Mitigation Strategy

The last thing any multinational organization wants to worry about are business and compliance risks introduced by third party vendors.

Everything You Wanted to Know About Blockchain (But Were Too Afraid to Ask)

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

Enabling Growth through Practice Management

In the world of financial advisory, growth strategies often focus squarely on the end client; after all, growth is achieved through new client acquisition or new asset acquisition from existing clients. While this logic is not incorrect, it fails to acknowledge the intricacies of third party distribution.

Reshaping the Indian Life Insurance Market

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market.

The Growing Asian Wealth Management Market: Capturing the Mass Affluent Opportunity

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry.

(Not) Selling Life Insurance in Asia

Amidst a boom in insurance business, Asian consumers remain largely underinsured.

Role Reversal: The Future of US Banks in the Online Lending Market

Following the financial crisis in 2008, Fintech startups gained a lot of prominence globally as consumers started to look for alternatives to traditional banking methods. These startups have penetrated every service area of consumer retail banking with the goal of dis-intermediating banks and becoming the new leaders of the financial services industry.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.