The Changing Landscape of Retail Banking

As BigTech and FinTech firms continue to disrupt the financial services industry, legacy banks today are witnessing their market share for banking services being chipped away due to the superior customer experiences that are offered by these tech firms.

While there have been instances when legacy banks have made large tech investments to compete, the results have not been reassuring. For example, the Chase Pay app developed to rival competition in the mobile payments was discontinued in early 2020 after receiving stiff competition from tech firms, such as Apple Pay, which provided a superior and glitch-free experience to consumers.

As tech firms foray into banking riding on their expertise in cloud computing, customer-facing artificial intelligence, and “big data” customer analytics to provide superior value to customers, banks need to rethink their strategy since it will be increasingly difficult to compete with the tech giants as they acquire significant market share.

A powerful strategy for banks is to adopt an open banking ecosystem that allows third parties, including FinTechs, to build superior user experiences on top of services offered by the banks. Open banking and the API economy allows legacy banks to embrace the tide of disruption they have been opposing for years.

Reviving the Value Proposition for Banks

When Google opened its Maps API to third party developers, it led to the development of several valuable services, such as Uber, that were built atop Google’s geolocation data. When financial institutions open their data to third parties, it is expected to bring in similar valuable products and services that customers can use to manage their finances. This will help banks create an ecosystem that will immensely expand the number of products and services available to customers, as well as the different options available to use them.

While the vast open banking ecosystem will enable innovative and digitalized services, it will also help banks be more transparent and compliant with regulations. The ability to share financial data with third-parties will also open new revenue streams for traditional banks (Exhibit 1). Digital banks in the EU and the UK such as N26 and Fidor are already trying to reinvent banking by building an app ecosystem for customers. For banks that are planning or have just started their open banking journey, an outside-in assessment of their resources and capabilities and designing a target state operating model will be key in guiding them into the new paradigm.

Examples of banks that have already adopted open banking include:

– HSBC launched its Connected Money app in May 2018 in response to the UK’s open banking regulations, allowing customers to view various bank accounts as well as loans, mortgages, and credit cards, in one place

– Barclays claims to be the first UK bank to enable account aggregation inside its mobile banking app. Its open banking feature allows customers to view their account with other banks within Barclays’ mobile app

– Yolt, created by ING, claims to be the first fintech to make a secure connection to the API of several UK banks such as Lloyds Banking Group, RBS and HSBC as well as the APIs of banks such as Monzo and Starling

Exhibit 1: Benefits of Open Banking for Traditional Banks

Open Banking is now evident

Banks have access to some of the most valuable data – customers’ finances; however, until now this vastly relevant data was not being used to benefit anyone. Open Banking encourages banks to release this rich financial data via APIs, in a secure standardized form, so that it can be shared more easily between authorized organizations online – all this while the customer remains in charge of who receives access to their financial data. While this provides a significant opportunity for FinTechs to build innovative customer centric products on top of this data, it also benefits legacy banks by significantly improving the customer experience and outreach of their banking products and services.

The open banking market is currently growing at 24.4% and is expected to reach $43.15 billion by 20261. Although this marks an inevitable shift in the financial sector, the pace has been further accelerated by the pandemic. To operate in the new open-banking paradigm, banks need to build robust and secure open APIs that are standardized to facilitate quick and easy integrations with third parties (Exhibit 2). Open Banking makes it possible to pass information securely to third parties, who can then use it to create valuable products for customers. This is likely to usher in an entirely new financial services ecosystem, in which banks’ roles may shift markedly. Financial institutions who push to be the early adopters of this new way of banking will be able to establish much larger open banking ecosystems, thereby providing customers a vast set of seamless and innovative products to choose from and a much greater value proposition.

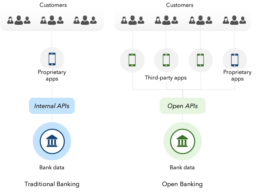

Exhibit 2: Traditional Banking (left) vs Open Banking (right)

Open Banking around the world

Exhibit 3: Open Banking is receiving significant regulatory and market push

Tenets of a Winning Open API strategy

Although banks have been using APIs for a few years now, the adoption has largely been reactive and unstructured. Moreover, the APIs being used were mostly internal to the bank. A survey conducted across 31 European countries revealed that 38% of bank APIs failed to meet EU and UK regulations(2).

To succeed in the new Open Banking paradigm, banks need a winning open API strategy. Often organizations place much focus on building technology while leaving their APIs vulnerable to poor adoption, duplicative efforts, non-reusable technology and reduced ROI.

An effective open API strategy that lays balanced emphasis on all aspects of API development and implementation (Exhibit 4) will boost a bank’s value proposition to the customer as well as their revenue. Banks that successfully leverage open APIs can see increases in revenue by up to 55%(3). Assessing the opportunity to build a robust prioritization roadmap early in the transformation journey is imperative in ensuring that the institution’s open banking implementation efforts remain focused and poised for success.

The 4 tenets of a winning open API strategy are described in more detail in the following sections:

Exhibit 4: Tenets of an effective Open API strategy

A. Adopting and API-first approach

API adoption must be a business-wide venture that touches every part of the organization, right from conceptualization to the development and delivery of different products and services (Exhibit 5). This means everyone should adopt an API-first mindset that embraces new customer value propositions and how APIs facilitate this value creation.

Without strategic steering from the leadership, API programs run the risk of fragmented implementation. Senior leaders should establish and champion the API-first concept throughout every function, at every level. Jeff Bezos, Amazon’s founder, famously mandated all systems and services to communicate using APIs with no other form of communication allowed. This declaration is attributed to instill an API-first culture which acted as the catalysis for AWS’ rapid growth to a billion-dollar business. API-first allows stakeholders to create ecosystems of applications that are modular, reusable, and extensible, like Lego blocks. This is essential for any financial institution as it allows easy and ready integrations with third-party providers as the industry moves towards the open banking paradigm.

An API-first mindset also fosters a culture of reusability. Business and design teams should always look at what can be reused before developing new services from scratch. Keeping reusability in mind while building APIs will liberate resources and reduce delivery timelines by 3-5x and improve productivity by up to 300%(4).

Exhibit 5: An API-first approach for banking products and services

B. Establishing API Governance

Proper API governance is essential for ensuring that the APIs being built and used are discoverable, consistent, and reusable. API governance also enables the implementation of best practices, such as reusable non-specific API design, which can help banks scale up their API portfolio fast. An effective API governance program should consist of:

– API Catalog and Metadata: Maintain central catalog of all active APIs available to developers. 39% of EU banks have non-responsive APIs listed in their developer portals(5). Keeping metadata for APIs ensures efficient management as the API portfolio expands.

– API Standards: Define API design and usage standards that are compliant with open banking regulations for the region (e.g., PSD2 in the UK). These should also include best practices such as documentation, API-only access to system of records, etc.

– Federated Operating Model: Establish a central team that is responsible for managing architecture and design standards, preferred practices, etc. and acts as the central design authority for all APIs developed across business units, while each business unit has its own team that works with the central team to ensure governance practices are upheld at the very grass roots.

– Performance Monitoring: Ensure the performance and operational resiliency of APIs by monitoring and reporting API utilization, queue sizes, response times and performance failures.

C. Building a Third-party ecosystem

While setting up open banking capabilities, establishing a thriving ecosystem for customers and developers is a necessary enabler to reap the benefits. Much of these benefits, both to the bank and to the customer, will be rendered ineffective if the bank fails to attract and encourage an active community of developers to use their APIs and build financial services products on top of it.

Banks should actively establish a third-party ecosystem by:

– Offering best-in-class developer portal, API sandboxes and developer tools that allow the third-party developer community seamless access to bank’s APIs. Making sure that the bank offers these functionalities is an essential step towards attracting developers to build, grow and nurture their open banking community. For example, Fiserv has built an extensive developer workspace that provides access to APIs, tools and a sandbox environment for the developers to access, integrate, configure and test the APIs.

– As banks establish their own developer workspaces, they also need to attract top developer talent to use their APIs to build and nurture an ecosystem of products and services. Banks can organize regular events, such as hackathons and knowledge-sharing workshops to attract the first few developers and further expand the third-party developer community.

– As developers start building the open banking ecosystem, it is necessary to maintain high-quality API documentation that is updated regularly and kept relevant with time, both for internal and third-party developers.

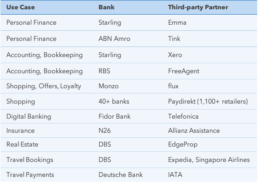

– Establishing long-term partnerships with FinTechs across various industries and use cases is another way to ensure that the bank’s ecosystem remains relevant (Exhibit 6). For example, Starling Bank’s Starling Marketplace offers investments via Wealthsimple, pensions via PensionBee, invoice insurance via Nimbla, mortgage origination via Habito and business loans via Growth Street.

Exhibit 6: Cross-industry partnerships in Open Banking

D. Monetizing open APIs available to third-parties

Open banking can cause a paradigm shift in how banks generate their revenues today. Open Banking regulations pull banks into the API economy and the broader financial services ecosystem, offering an opportunity to emulate the learnings and successes from tech platform companies and FinTechs. By monetizing APIs, Expedia generated over 85% of its annual revenue, while eBay generated over 60% of its revenue from APIs. In early 2020, Visa agreed to pay $5.3 B for acquiring Plaid, an API-driven Fintech6.

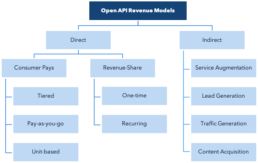

Banks can adopt a direct monetization approach in which providing API access to third-parties is directly linked to the Bank’s revenue. Alternately, banks can also opt for an indirect monetization approach where value delivered from API access is claimed in indirect other ways (Exhibit 7).

These monetization models should not be seen as a one-shot monetization strategy to implement for all bank APIs. Banks should categorize their API portfolio and adopt a monetization approach that is best suited for each API category, market, region, etc. Common ways to classify APIs is:

- Utility and Helper APIs – These APIs do not provide access to any exclusive information and hence can be offered for free as incentives for developers to onboard on developer portals and start using the bank’s APIs.

- Data APIs – APIs that share non-monetary data, such as customer profiles, etc. can be classified as Data APIs. These are also the most preferrable APIs for the indirect monetization approach.

- Transaction APIs – Transaction APIs are used to share transaction or monetary information with third-party developers. Direct monetization approaches are preferred with Transaction APIs.

- Application Integration and User Interface APIs – APIs categorized under this bucket supports data transfer between multiple apps or UIs and ensures it remains in-sync and up-to-date.

Exhibit 7: Revenue models for open API monetization

In Closing...

While Open Banking was already picking up speed across Europe and North America, the global pandemic has further accelerated its adoption. The bank’s involvement in the API economy is now not a question of when but how. Banks need to come up with wholesome open API strategies that enable them to build thriving ecosystems of products and services for their customers. At the same time, banks must identify and implement the right data monetization models to maximize their revenue streams from providing third-parties access to their APIs.

To achieve this, banks’ leadership must launch open banking programs that scope the whole value chain that they operate in – instilling reusability during API design to ensuring adoption at launch and then driving developer engagement. Furthermore, the implementation of these open banking programs and API strategies must be assured with effective program management and robust monitoring.

Banks that can move fast, boost API usage, build robust open API portfolio and establish their ecosystems early on will be industry leaders in the new open banking paradigm; in contrast, those who continue to operate via the traditional banking route will continue to lose their market share to open banking leaders and FinTechs.

References:

- Padua, Vince. “Open Banking Is Now Essential Banking”, Forbes, 8 February 2021

- Salt Edge. “Open Banking Ecosystem in Testing Mode”, Salt Edge Report, 6 May 2020

- FISPAN. “Demystifying Open Banking: Why Open Banking Matters for your Bank”, FISPAN Report, 21 October 2020

- MuleSoft. “The value of connectivity”, MuleSoft Report, 2020

- Salt Edge. “Open Banking Ecosystem in Testing Mode”, Salt Edge Report, 6 May 2020

- Subramaniam, Mohan. “The Strategic Value of APIs”, Harvard Business Review, 7 January 2015

Read More

Transformation Readiness

70% of all planned transformation initiatives fail to deliver tangible business value and 84% of organizations fail at tech transformations in particular.

Rethinking the Future of your Business

The economic climate is becoming increasingly uncertain with cautionary signals of recession, along with inflationary pressure, fluctuating currencies, and uncontrollable impact of geopolitical events. Firms need to proactively take this opportunity to refocus their future investments on high value, high potential business lines.

Technology and Healthcare

Data production in healthcare occurs in different volumes, velocities, and formats by multiple sources – EHR, diagnostic, imaging, claims, billing, medical devices to name a few.

Enterprise Cyber Resilience in a Hybrid World

Cybersecurity incidents are also not only a threat to corporations’ internal operations and bottom line; customer personally identifiable information and financial data is also at serious risk of exposure and misuse, in turn impacting customer perception and long-term brand loyalty.

Finding Growth in US Insurance

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Data-Driven Post-Merger Integration

A common misconception is that revenue synergies are illusive or “icing on the cake”, primarily because they are more challenging to quantify.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

Platformization of Health Tech

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously

Are Your Vendor Risks Under Control?

Investing in vendor risk management today can secure a future brimming with cost-effective, secure, successful and trust-worthy partnerships.

(AI)ntelligent Procurement

In a competitive business environment, high-performing CPOs are 18x more likely to fully deploy AI/cognitive capabilities. This typically leads to 92% faster demand forecasting, on average 350 man-hours are saved through automation, and there is a potential for 24/7 operations

Realizing Your Workforce Strategy

Organizations are now recognizing the limitations in their workforce programs, so are making a concerted effort to develop a contingent workforce strategy, consolidate their master vendors/staffing agencies, and extract maximum benefits from the program.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Getting the Basics Right

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Ensuring Loyalty of your Prized Clients

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

The Cloud-Native Paradigm

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Business Analytics in Pandemic Times

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Reshaping Wealth Tech

Before the Covid-19 inducted recession, the wealth tech sector was already experiencing a slowdown - both in the number of new startups and total capital raised. Now more than ever, investors and operators must be bold in re-inventing their Firm's long-term value proposition.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

How to Thrive in the New Normal

Now that Business As Usual is unusual, leaders are forced to re-imagine business models and build ‘winning strategies’ - to not only survive the pandemic but also emerge as successful change-makers, shaping an altered business reality.

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Trends in Digitalization of Insurance

For some, Insurance might seem a monolithic industry, but for the ones keeping a close eye on it- Insurance is revamping itself faster than ever!

From days when underwriting a simple policy would take weeks and months, to now when it can be done in seconds with a simple ‘selfie’ - there seem to be no bounds in the future of this industry.

Customer Engagement Index

While firms have found tremendous success in using these loyalty metrics to successfully grow customer relationships, they are lagging indicators and provide little help in providing immediate insight into whether or not improvements and initiatives are moving the needle.

Strategic Sourcing of a “Difficult” Spend Category

Some clients have even deemed spend reduction in procurement categories like legal services, where recourses and expertise are concentrated within humans not technology, to be intractable. At Kepler Cannon, we continuously challenge these sorts of conventional wisdom.

Third Party Information Risk Mitigation

It is well known that one way to make better predictions about how your customers, distributors and suppliers will behave, is to augment your own data with that of third parties.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Reducing Strategic Over-Dependence on IT Vendors

Over time, many firms realize that they have become so reliant on vendors/contractor for critical knowledge on key applications, that they have, in fact, ceded control of those applications to the vendors.

Are Blockchains Evolving Like Securities Exchanges?

Driven by data security concerns, a majority of financial institutions are now looking at so-called private or hybrid blockchains, rather than fully decentralized public blockchains (like the blockchain used for Bitcoin)

How Global Resourcing May Be Killing Your Company’s Efficiency

As global firms respond to the post-Great Recession regulatory and economic realities, efficiency of the back-office has become critical to ongoing success.

Third Party Vendor Risk – A Continuous Mitigation Strategy

The last thing any multinational organization wants to worry about are business and compliance risks introduced by third party vendors.

Everything You Wanted to Know About Blockchain (But Were Too Afraid to Ask)

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

Enabling Growth through Practice Management

In the world of financial advisory, growth strategies often focus squarely on the end client; after all, growth is achieved through new client acquisition or new asset acquisition from existing clients. While this logic is not incorrect, it fails to acknowledge the intricacies of third party distribution.

Reshaping the Indian Life Insurance Market

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market.

The Growing Asian Wealth Management Market: Capturing the Mass Affluent Opportunity

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry.

(Not) Selling Life Insurance in Asia

Amidst a boom in insurance business, Asian consumers remain largely underinsured.

Role Reversal: The Future of US Banks in the Online Lending Market

Following the financial crisis in 2008, Fintech startups gained a lot of prominence globally as consumers started to look for alternatives to traditional banking methods. These startups have penetrated every service area of consumer retail banking with the goal of dis-intermediating banks and becoming the new leaders of the financial services industry.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.