Data likely to Unlock Next Phase of Growth

‘5 exabytes of information was created between the dawn of civilization through 2003, but now that much information is created every two days.’ – Eric Schmidt, Executive Chairman, Google

Industry leaders are constantly looking to maximize benefits from what they already have. One way to remain relevant is to utilize a resource ubiquitous, especially for FinTechs & financial institutions i.e., data. Firms have a plethora of rich, growing data on customers, merchants, transactions, products, interactions etc.. This data can be used to improve decision making, customer loyalty, expose new revenue streams, and operate more efficiently.

Firms who prioritize this and find ways to monetize this asset will stand to separate themselves from the pack, as well as solidify existing customer relationships. Even though monetization of data was important pre-pandemic, the ‘new normal’ has multiplied its potential benefits, amplifying both need and opportunity. Here are some trends that explain why now is the right time to invest in a robust data monetization.

Tighter Margins. Traditional sources of revenue, such as core transaction processing fees, are becoming increasingly commoditized, and margins are getting squeezed by inflation, spurring the need for alternative revenue streams.

Unprecedented Digitalization. The last couple of years have led to dramatic acceleration in digital commerce. Businesses are increasingly willing to pay a premium for commerce-enablement services, such as loyalty programs, business intelligence, performance improvements such as enhanced authorization rates, cart optimization, chargeback mitigation etc.. This has created an opportunity to leverage rich financial data in providing such value-added services.

Rise of Embedded Finance. Financial services, rather than being offered as a standalone product, are becoming seamlessly wrapped/embedded into other services, products or technology. Examples include Apple card, Shopify, Amazon Pay, Grab pay etc. In such an ecosystem, financial institutions will need to draw richer insights from customer data tailor offerings/services and remove points of friction.

Digital technologies driving data proliferation. Digital technologies are enabling firms to build entirely new capabilities. For example, mobile devices offer customers anytime, anywhere services providing more context and closer engagement with customers, cloud computing enables firms to launch and scale up services rapidly, open technologies like APIs enable exchange of real time data, AI helps with faster data processing and decision making. This translates to proliferation in data and more avenues and opportunities for monetizing data.

Regulatory challenges. Regulations such as PSD2, Australia’s customer protection laws, consumer-authorized financial data sharing in the U.S., are giving customers more control over their data, forcing transparency, and making a plethora of additional data available to firms who service clients. Open, portable data will erode competitive advantage of incumbent data rich financial institutions. Now is the time for incumbents to rethink how they can monetize internal data, as well as that available through external partnerships, in ways that help them leapfrog the upcoming competition.

Today’s Gold Mine. The estimated market associated with data monetization is expected to be around $11.7B by 2026, a 47.9% growth from $0.7B in 20191. A Forrester Research study also indicated that top-performing companies are 3x more likely to seize new data monetization opportunities than those struggling to grow. This is evident by the numerous mergers and acquisitions of data aggregators such as Nasdaq’s acquisition of Quandl (2018) or London Stock Exchange Group’s whopping $27B acquisition of financial data provider Refinitiv (2021).

While other financial firms, such as banks, are aware of the benefits, most of them have been slow to monetize their data. This is primarily because financial firms have traditionally viewed the custody/protection of their customers data as a responsibility, rather than an asset to be commercialized. This is due to several reasons such as complexities around data sharing (risk and permission-based, audit trails), regulations and compliance (e.g., GDPR, GLBA, CCPA), fear of compromising user privacy, reputational risk and a lack of data monetization expertise.

Knowing Monetization

Data can be monetized directly or indirectly:

Direct Monetization

Direct monetization involves using data to directly generate revenue, either by selling the data itself or selling insights from the data. Although top line driven, direct monetization is less common and all too often overlooked, primarily due to the presumed fear of potential regulatory violations. Some of the common ways of directly monetizing data are:

- License / Sell Data: Provide data access (e.g., aggregated transaction data) to others (own customers or third parties) via data sharing APIs. The buyer can use it for their own analytical efforts, product / service development and research

- Develop New Products / Services: Create new products and services based on aggregated customer data (e.g., Bloomberg’s Evaluated Pricing service, BVAL which supplies pricing daily for over 2.5m securities across all asset classes)

- Sell Insights: Sell processed analytical insights (e.g., Transaction signals can be sold to investment firms; customer purchase trends / analysis to corporations looking to expand business)

- Enhance Existing Product & Services: Leverage data analytics to provide surround products / services with existing offerings (e.g., Mainstreet Insights by Fiserv leverages analytics to optimize businesses of its merchant customers by providing performance reports, sale trends, customer purchase behavior tracking etc.

Exhibit 1. Types of Data Monetization

Indirect Monetization

By contrast, leveraging internal performance data (supplemented with / without external data) to optimize and grow own business is referred to as indirect monetization. It is usually bottom-line driven and helps enhance operational efficiency, improve user experience, reduce risk and compliance issues. This approach is more popular, since businesses of all sizes can make marked operational improvements, and there is usually no red tape to navigate. Some of the ways in which data can be indirectly monetized are:

- Enhance Customer Engagement / Reduce Attrition: Cross sell / up sell products based on analysis of current consumption, customer churn analysis to identify attrition factors, proactively predict at risk customers, design outreach campaigns

- Reduce Risk / Fraud: Test adequacy of risk models, use ML based pattern identification to improve compliance processes, identify fraud opportunities or fraudulent events in progress

- Improve Operations: Tracking of operations KPIs and SLAs to track efficiency, improving product design and processes based on internal performance, customer feedback

- Enhance Acquisition: Enhance targeting for high value leads, increase effectiveness of campaigns, identify new market to grow business

The ideal way to strike the right balance is to start from the source and move to the receiver, i.e., first secure the buy-in from the entity providing the service to the entity consuming the service.

Demystifying Monetization

‘Errors using inadequate data are much less than those using no data at all.’ – Charles Babbage, English Mathematician

By and large, most firms fail to embark on the data monetization journey due to the lack of expertise. While the concept of using data is not new, monetizing data in a strategic and coordinated fashion without exhausting firm’s resources and yet delivering a competitive advantage is the new emerging frontier. Here are critical steps to understand when evaluating a potential data monetization strategy:

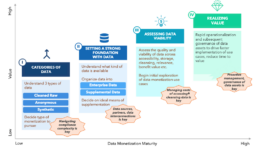

Exhibit 2. Data Monetization Stages

I. Categories of Data

A data monetization strategy must consider potential compliance issues inherent to certain data types:

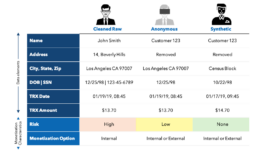

- Raw data may contain personally identifiable information (PII) (e.g., data on where and how a specific person shops at a specific time). It is the most valuable type of data but also has highest risk for threat or misuse

- Anonymized data is the next-most valuable type and has had PII removed. This type of data is much more general than raw data and lacks consumers’ specific details, but it has fewer risks

- Synthetic data is often the ideal data set for monetization as it contains ‘fake data sets that cannot be tracked to the original consumer or firm’. Synthetic data will lack gender information of consumers and will not offer accurate, specific times of purchases, among other factors, but it does provide more data points than anonymous data

The decision to go ahead with direct or indirect monetization will inform the data type to be used. Since direct monetization is external it involves using anonymous/synthetic data whereas indirect monetization can use all three types of data keeping in mind that using cleaned raw data comes with high risk

Exhibit 3. Data Types

II. Setting a Strong Foundation with Data

Not all data available is valuable or saleable in its raw form; it typically requires harmonization with other sources (e.g., market share, meteorological or satellite imagery, commodity markets) to yield valuable insights. Hence, it is important to understand what kind of data is available and how it can be primed for monetization. Once data is identified, they should be mapped to the organizational value chain to explore interconnections, potential opportunities, and risks.

After mapping, data can be organized usually in the form of enterprise-level data (consists of customer/client-generated data, internal performance data) and supplemental data (drawn from external parties/sources). Supplemental data can be added to existing data through various means, such as:

1. Leverage non-traditional alternative data sources to strengthen use cases (including web behavior, mobile-session data, public blogs, social media, and weather forecasts)

2. Use partnerships, platform providers/collaborators to add value to existing data (e.g., Banks can partner with third-party providers like D&B, and Experian to expand merchant industry coverage, and strengthen prospecting, and compliance use cases)

3. Run hackathons and contests to generate new ideas, models, and techniques (e.g., BNP Paribas, Prudential Financial, and Santander sponsor competitions on Kaggle, a data-science hackathon platform)

4. Based on the natural state of the data and the ideal means of supplementation, firms can identify partners who can enhance internally farmed data and prepare it for monetization. For instance, financial services firms have data on consumers/merchants that may not provide a monetization opportunity individually, however when considered in sync with another data set can become more valuable. E.g., Visa and Facebook’s collaboration for P2P payments and e-commerce on WhatsApp provides more excellent data coverage of consumers’ current and potential spending.

Exhibit 4. Monetizable Data with Financial Institutions

III. Assessing Data Viability

After outlining the available data and enriching its value, it is important to evaluate data’s viability for direct / indirect monetization against some of the following questions: (exhibit 5). At this stage, costs of storage, cleaning, governance, consumption and processing of data must be managed against the ever growing and accelerating volume / variety of data.

Once data’s quality has been assessed, the firm can start exploring initial data monetization use cases. Pilots can be conducted on well-vetted use cases to test, learn and gain experience before launching an organization wide data monetization effort.

Exhibit 5. Data Viability Levers

IV. Realizing Value

Once sufficient hands-on experience has been gained, firms can move into rapid operationalization and subsequent governance of data assets to drive faster implementation of use cases, reduce time to value. Acceleration in value will require pro-active management of firm’s data and analytic assets, enhancements as well as strong collaboration and commitment from business and technology.

Industry Success

Both incumbents and growing fintechs are already pursuing innovative data monetization strategies, for example:

Final Thoughts...

Firms need a tailored roadmap to be able to exploit value from data – an asset that never depletes and can be used across an unlimited number of use cases at near zero marginal cost. They must transition from considering data as a cost-accruing asset (with high upkeep linked to storage, data management platforms, etc.) to a revenue-generating asset (either directly contributing to top line or indirectly by using data to improve products/services). Some guiding principles are outlined in Exhibit 6 below:

Exhibit 6. Guiding Principles

...and Considerations

- Navigate Compliance Complexity: Obtain deep understanding of privacy/ compliance requirements (GDPR, CCPA regulations, etc.); work closely with experts when designing new products/ services

- Data Overload / Exhaust: Often companies have too much widely distributed data that it becomes difficult to organize it. Ensuring an appropriate governance and infrastructure in place is key to avoid dealing with data exhaust

- Build the Right Talent Pool: Identify new roles, responsibilities, metrics and risk controls in order to build effective cross-functional collaboration across teams. Also, ensure availability of critical talent including data scientists, data engineers and product managers

- Adopt a Networked Partnership Model: Consider partnerships to enrich data, leverage external analytical expertise and expand use cases and distribution channels

- Consider ROI: Compare the cost of cleaning/sanitizing data and scaling/performing analytics to the expected return. Also, assess the consistency and replicability of those intangible or tangible benefits

- Start Small: Start with a series of small tests / experiments to better monitor customer feedback and sentiment. This will encourage continuous improvement, learning, and fine-tuning of the solution

__________________________________________________________________________________________________________

Read More

Transformation Readiness

70% of all planned transformation initiatives fail to deliver tangible business value and 84% of organizations fail at tech transformations in particular.

Rethinking the Future of your Business

The economic climate is becoming increasingly uncertain with cautionary signals of recession, along with inflationary pressure, fluctuating currencies, and uncontrollable impact of geopolitical events. Firms need to proactively take this opportunity to refocus their future investments on high value, high potential business lines.

Technology and Healthcare

Data production in healthcare occurs in different volumes, velocities, and formats by multiple sources – EHR, diagnostic, imaging, claims, billing, medical devices to name a few.

Enterprise Cyber Resilience in a Hybrid World

Cybersecurity incidents are also not only a threat to corporations’ internal operations and bottom line; customer personally identifiable information and financial data is also at serious risk of exposure and misuse, in turn impacting customer perception and long-term brand loyalty.

Finding Growth in US Insurance

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Data-Driven Post-Merger Integration

A common misconception is that revenue synergies are illusive or “icing on the cake”, primarily because they are more challenging to quantify.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

Platformization of Health Tech

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously

Are Your Vendor Risks Under Control?

Investing in vendor risk management today can secure a future brimming with cost-effective, secure, successful and trust-worthy partnerships.

(AI)ntelligent Procurement

In a competitive business environment, high-performing CPOs are 18x more likely to fully deploy AI/cognitive capabilities. This typically leads to 92% faster demand forecasting, on average 350 man-hours are saved through automation, and there is a potential for 24/7 operations

Realizing Your Workforce Strategy

Organizations are now recognizing the limitations in their workforce programs, so are making a concerted effort to develop a contingent workforce strategy, consolidate their master vendors/staffing agencies, and extract maximum benefits from the program.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Getting the Basics Right

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Embracing Open Banking

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

Ensuring Loyalty of your Prized Clients

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

The Cloud-Native Paradigm

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Business Analytics in Pandemic Times

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Reshaping Wealth Tech

Before the Covid-19 inducted recession, the wealth tech sector was already experiencing a slowdown - both in the number of new startups and total capital raised. Now more than ever, investors and operators must be bold in re-inventing their Firm's long-term value proposition.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

How to Thrive in the New Normal

Now that Business As Usual is unusual, leaders are forced to re-imagine business models and build ‘winning strategies’ - to not only survive the pandemic but also emerge as successful change-makers, shaping an altered business reality.

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Trends in Digitalization of Insurance

For some, Insurance might seem a monolithic industry, but for the ones keeping a close eye on it- Insurance is revamping itself faster than ever!

From days when underwriting a simple policy would take weeks and months, to now when it can be done in seconds with a simple ‘selfie’ - there seem to be no bounds in the future of this industry.

Customer Engagement Index

While firms have found tremendous success in using these loyalty metrics to successfully grow customer relationships, they are lagging indicators and provide little help in providing immediate insight into whether or not improvements and initiatives are moving the needle.

Strategic Sourcing of a “Difficult” Spend Category

Some clients have even deemed spend reduction in procurement categories like legal services, where recourses and expertise are concentrated within humans not technology, to be intractable. At Kepler Cannon, we continuously challenge these sorts of conventional wisdom.

Third Party Information Risk Mitigation

It is well known that one way to make better predictions about how your customers, distributors and suppliers will behave, is to augment your own data with that of third parties.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Reducing Strategic Over-Dependence on IT Vendors

Over time, many firms realize that they have become so reliant on vendors/contractor for critical knowledge on key applications, that they have, in fact, ceded control of those applications to the vendors.

Are Blockchains Evolving Like Securities Exchanges?

Driven by data security concerns, a majority of financial institutions are now looking at so-called private or hybrid blockchains, rather than fully decentralized public blockchains (like the blockchain used for Bitcoin)

How Global Resourcing May Be Killing Your Company’s Efficiency

As global firms respond to the post-Great Recession regulatory and economic realities, efficiency of the back-office has become critical to ongoing success.

Third Party Vendor Risk – A Continuous Mitigation Strategy

The last thing any multinational organization wants to worry about are business and compliance risks introduced by third party vendors.

Everything You Wanted to Know About Blockchain (But Were Too Afraid to Ask)

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

Enabling Growth through Practice Management

In the world of financial advisory, growth strategies often focus squarely on the end client; after all, growth is achieved through new client acquisition or new asset acquisition from existing clients. While this logic is not incorrect, it fails to acknowledge the intricacies of third party distribution.

Reshaping the Indian Life Insurance Market

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market.

The Growing Asian Wealth Management Market: Capturing the Mass Affluent Opportunity

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry.

(Not) Selling Life Insurance in Asia

Amidst a boom in insurance business, Asian consumers remain largely underinsured.

Role Reversal: The Future of US Banks in the Online Lending Market

Following the financial crisis in 2008, Fintech startups gained a lot of prominence globally as consumers started to look for alternatives to traditional banking methods. These startups have penetrated every service area of consumer retail banking with the goal of dis-intermediating banks and becoming the new leaders of the financial services industry.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.