Why Aren't We There Yet?

Despite a big wave of RPA implementations, the back-office is often left behind in enterprise-wide digital transformations. Today, back-offices continue to be plagued by manual, repetitive processes. The complexity of these operations is now further compounded by the exploding data generated, stored, and consumed. Fortune 500 firms lose an average of $480 billion a year due to inefficiencies, mostly in the back-office.(1) So what is preventing so many financial institutions from digitizing their back-office?

The status quo: Focus on customer experience over satisfaction

Simply put, industry dynamics have forced investments to be focused on “above the glass” enhancements to customer experience while postponing much-needed digital back-offices. Frequently, financial institutions tend to fall victim to the misconception that there is no immediate business case for back-office upgrades. This assumption fails to fully consider the immediate benefits of redeploying personnel, improving efficiency, and optimizing processes.

Exhibit 1. Shrinking Investment in the back-office

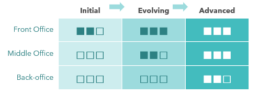

Market Digitization Landscape

There is a broad spectrum of both progress towards and commitment to end-to-end digitization within the market currently:

1. Initial digitization: These firms have typically completed some level of customer-experience-focused transformation (e.g., digital interfaces) in their front office, but are still characterized by mostly manual middle and back-offices. This often entails manual processes such as emails being sent back and forth and/or physical paper being scanned to share information. These processes are time-consuming, repetitive, and require multiple systems and touchpoints.

2. Evolving digitization: Like initial state FIs, these institutions tend to have fully digital front offices with enhanced CX, and often have some degree of digital tool use in their middle office (e.g., API connectivity between systems, automated translation of customer inputs and requests from digital channels) as well. However, their back-offices remain manual, posing the risk for delays and re-submissions that can impact customer satisfaction.

3. Advanced digitization: Advanced stage FIs are almost completely digital as it pertains to customer touchpoints and have significant digitization in their middle and back-offices. There is limited paper being used, API connectivity between system and applications, and almost no manual keying in of input by personnel. Document creation is either natively digital or involves instant digitization, ensuring a satisfactory customer experience from end to end.

Exhibit 2.Stages of Digitization

Customer Experience Vs. Customer Satisfaction

It’s important to delineate between customer experience (CX) and customer satisfaction. Digitization has thus far indexed heavily on customer experience, which refers to the impression left on the customer based on interactions with financial institution.

This includes digital interfaces, savvy UI, and seamless transitions between form factors.

While customer experience is no doubt important, customer satisfaction typically plays a more profound role in the overall relationship, as it refers to a customer being satisfied with the comprehensive outcome, as opposed to individual interactions.

For example, an FI may have a delightful user interface, but if underlying data is not tagged and leveraged in a compliant yet shareable manner across the enterprise, the customer will have to resubmit the same documents, and their overall satisfaction will likely be low. As such, investments focused only on front office digitization fail to consider the larger picture.

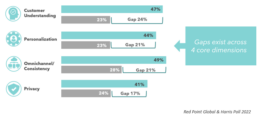

Exhibits 3 & 4 demonstrate the gap that often exists between internal and external perceptions of customer experience delivery.

This gap is largely due to the fact that customers index on customer satisfaction, evaluating their overall experience in a more comprehensive manner.

Exhibit 3. Legacy FI Customer Experience Gap

Exhibit 4. Gaps across key dimensions

What Does The Prize Look Like?

While digitally transforming the back-office may pose some challenges, the benefits far outweigh the costs; digitizing, automating, and optimizing document-related workflows is estimated to reduce costs by more than 35%, reduce time spent on document-related tasks by 17%, and reduce errors by almost 52%.(2)

Considering that over $600 billion in costs across industries can be attributed to data entry errors, a 52% reduction has a noticeable impact.(3)

Further, banks that have undergone successful digital transformation have seen up to 4x acceleration in the delivery of new products and services, which is a direct result of noticeable (20-30 points) improvements to customer satisfaction scores.(4)

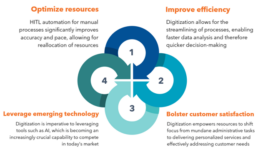

These back-office digitization benefits are quantitative, significant operational expenditure and revenue expansion opportunities.

The advantages can be bucketed into four main categories as outlined in Exhibit 5 to the right.

Exhibit 5. Advantages to Back-Office Digitization

But it ain't easy

Exhibit 6. Back-office Digitization Challenges

If the impact to customer satisfaction is so clear, what is preventing FIs from investing in digital transformation? The heterogenous nature & structure of inbound channels makes progress inherently difficult for many reasons:

1. Customer data intake often occurs in an omnichannel fashion through a difficult-to-streamline mix of physical and digital sources. For example, an onboarded customer may fill out a digital intake form but provide a photo of their ID via email.

2. Data intake often entails complex, multi-touch routes For example, to process a single auto loan, a bank must coordinate with the dealer and customer to receive a loan application, verify documents, underwrite loan risks, communicate loan terms, disburse loan funds, transfer vehicle title to the customer, and set up loan payments. These complicated processes are incredibly paper-heavy, manual, and therefore time-consuming.

3. There are ever-increasing regulatory compliance guidelines (e.g., BASEL, AML, NIST, GDPR, ISO-27001) that are already estimated to account for 10% of a typical bank’s overall operating costs(5); therefore, further compliance penalties resulting from process change management can be understandably deterring.

How Should You "Not" Approach It

Typically, organizations embark on their digitization journey with a myopic focus on ROI, employing a cost-to-savings matrix approach to segregate initiatives.

While the cost-to-savings matrix approach may yield quick wins in the form of incremental efficiency gains, it is fraught with several inherent drawbacks that undermine its long-term viability:

Enterprise ROI Optimization:

Attempting to avoid siloed optimization, businesses often focus on maximizing organizational level ROI from day one, considering enterprise-wide solution applicability to individual business units secondarily.

However, counterintuitively, we have seen lower success with firms succeeding in this sequence, as it fails to consider the challenges in obtaining LOB-specific stakeholder buy-in, aligning financial budgets across LOBs, and deployment constraints.

Prioritization based on Misleading Indicators:

Rather than using broad indicators as signals to shortlist processes and then methodically arrive at processes with ROI for digitization, enterprises often hastily digitize processes with a high degree of paper jams or human efforts involved.

This fails to consider other key parameters, such as impact on end-customer experience, criticality to business, applicability/scope of expansion to other business units, etc.

Deferred Transformation:

Although there is clear consensus on the high ROI potential of long-term initiatives, they often get relegated to the backseat due to the sheer costs involved, time to realize benefits, and level of foundational changes required. Most often, these transformational initiatives are what stands between delivering good customer experience in bits versus ensuring high overall customer satisfaction. This shortsightedness not only stifles future growth, but also increases the complexity and cost of future transformation endeavors.

Ignoring Readiness:

Deploying ostensibly easy-to-implement solutions without due consideration for readiness levels (technological, organizational, process, financial) can lead to resistance, inefficiencies, and suboptimal long-term ROI.

Exhibit 7. Conventional Approach to back-office Digitization

How To Get It Right

To address these challenges and steer toward sustainable success, organizations must:

- Solution individual LOBs first and then expand (versus the converse)

- Prioritize use cases based on benefits beyond immediate operational savings (versus misleading indicators)

- Innovate designs for modularity, agility and efficiency (versus point solutions)

- Customize digitization journey based on readiness levels (versus ad hoc implementations)

Let us dive deeper into each of these guiding principles:

1. Solutioning individual LOBs first

In theory, maximizing enterprise-wide ROI by solutioning across the enterprise with potential synergies and economies of scale would be the right approach.

The problem with this enterprise approach is that the onus of digitization then lies with the CIO’s office.

This path is riddled with challenges as the broad mandate is difficult to execute considering specific goals and targets of individual business units.

However, we have seen digitization efforts gaining success when deployed within an LOB, contained within a cost center, and then expanded to other LOBs.

The recommended approach would be to target use case(s) within a specific LOB, fix issues with ease, and deploy solutions contained in the same cost center.

Further, contained implementations also provide a better line of sight into customer satisfaction, identifying learnings that can be extended to the broader organization.

Upon successful implementation, the solution can be extended as needed through in-house efforts or partnerships with external players.

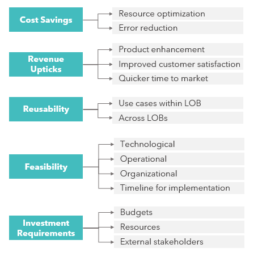

2. Prioritizing use cases with benefits beyond immediate savings

There is no denying the fact that a high degree of manual effort, physical paper documents, and repetitive data exchange are strong indicators of areas that can benefit from digitization.

However, following these signals alone to develop one’s digitization journey map might dampen the ROI, as there are use cases that can hugely benefit from digitization in other ways beyond these direct operating expense savings.

The most pertinent examples are revenue-side benefits such as better up-sell/cross-sell potential due to improved customer satisfaction, quicker time to market, product differentiation and indirect cost savings like reusability/applicability of solution to other use case(s) or LOB(s) and so on.

Not to mention the fact that factors such as feasibility (technology, operational) and investment requirements need to be incorporated while scoring and prioritizing use case(s).

Exhibit 8. Use-case Prioritization

3. Innovating designs for modularity, agility and efficiency

In all fairness, there has been digitization of back-office processes across accounting and finance, transaction processing, underwriting and risk management, customer service, compliance and regulatory reporting over the past few years. However, such digitization has often been unstructured, and the presence of legacy systems, paper-heavy manual processes, strict regulations, and high cost of error still hinders effective digitization.

Under such conditions, innovating design to be modular, agile, and efficient is crucial. Most FS back-office processes follow a standard flow that begins with incoming data from different channels and sources being received by back-office staff. It is then processed based on established rules, and often in collaboration with cross-functional teams. The processed output is then used for downstream purposes (e.g, sending output to customer, reporting). Finally, the data is archived to generate insights and for regulatory purposes.

For example, a bank loan application’s data inputs could be paper documents (application and proofs) in the case of in-person branch visit, or digital files from a digital application. Relevant information from the paper is manually validated and entered in a loan origination or management system (LOS/LMS).

Information processed in these systems is used across teams (e.g., underwriting, risk management, compliance, regulatory reporting) and is taken by the customer service team to request further proofs, or to communicate the sanctioned loan amount and terms. Only a digital back-office would allow different teams to glue things together to satisfy customer needs effectively and avoid the large degree of back and forth that this complex process would otherwise require.

Designing different components of this back-office involves careful consideration of the following:

1. Data inputs: As incoming data arrives from different channels (e.g., fully digital, “phygital”, paper documents) with different levels of sensitivity (incl. PII), the data ingestion mechanism must be comprehensive enough to handle wide spectrum of:

- Data types: structured, semi-structured and unstructured

- Data sources: paper documents, PDFs, images, excel files

- Data channels: digital (bulk uploads, portals, emails), scanned paper documents, mobile application, fax

2. Core Processing Engine: The effectiveness of an FI’s processing engine largely depends on:

- Intelligent processing capabilities: The industry is shifting from basic optical character recognition (OCR) based processing towards advanced AI/ML based intelligent document processing (IDP) and NLP based customer service. Enterprises should be open to partnerships with relevant startups if they lack necessary expertise in-house and/or need faster deployment

- Taxonomy and Rules Engine: Extracted data needs to correctly classified and categorized. Thereafter, workflows need to be configured based on rules. Using both standard taxonomy and rules for cross-use cases/LOB application and specific taxonomy and rules customized to specific use cases/LOB is key for successful deployment.

- Process automation: Lastly, workflows need to be automated allowing for human in the loop (HITL) layer to accommodate manual checks for exception handling

3. Integrations: Effective functioning of the core processing engine requires seamless integration through:

- 3rd party APIs: to connect with required 3rd party systems (e.g., PEP data bases for KYC checks)

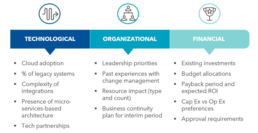

4. Customizing digitization journey based on readiness

To kickstart digitization, it is imperative for FIs to customize plans based on technological, organizational, and financial readiness.

i. Tech Readiness

This involves understanding share of legacy to modern systems, feasibility of modernization, and complexity of integrations involved. Organizations must also assess their degree of decoupled architecture to gauge agility and flexibility in deploying digital solutions. Evaluating partnerships and integration feasibility becomes crucial, as does ensuring the impact of digitization on data security, compliance, and regulatory reporting standards.

ii. Organizational Readiness

Often, the type and number of resources for back-office processes changes with digitization. Therefore, assessing an organization’s appetite for change based on past experiences becomes key. Moreover, aligning digitization initiatives with leadership priorities ensures strategic alignment and support, while addressing the ability to maintain business as usual (BAU) operations during the transition period increases organizational confidence and probability of success.

iii. Financial Readiness

Financial readiness assessments involve a comprehensive analysis of existing investments, budget allocation, and financial goals. Organizations must conduct a thorough examination of investments already made and subsequently estimate the expected payback period in order to measure ROI. Further, considerations such as budget allocation and preferences towards capital versus operational expenditure help inform investment strategies and assist with decision-making as final approvals are sought from a cross-functional leadership body.

Exhibit 9. Digital back-office Design [Sample]

Exhibit 10. Readiness Assessments

In Closing...

End-to-end digital transformation is a prerequisite for long term success for financial institutions. To stay competitive, retain customer loyalty, and move the needle from customer experience to customer satisfaction, financial institutions need to digitize their back-offices as soon as possible. And while there are plenty of obstacles that accompany this transformation (e.g., channel complexities, low perceived ROI, stringent regulations), digital back-offices allow for the optimization of resources, improved efficiency, bolstered customer satisfaction, and leveraging of emerging technology.

Financial institutions should aim to digitize aggressively, whether that be solutioning on an individual LOB level and expanding, prioritizing use cases based on perceived returns, taking a modular but agile approach to innovation, or customizing based on overall readiness.

The status quo has too long indexed on customer experience as the dominant consideration for digitization. Customers are no longer fooled by fancy UI; they are more focused on their overall satisfaction. Further, rapidly emerging technology and innovation will not adapt to accommodate legacy systems and institutions. It is time for FIs to move past the reactive environment where “above the glass” enhancements to customer experience are considered sufficient and begin tackling their digital back-office transformations.

__________________________________________________________________________________________________________

- SSO Network

- Mely AI

- Itemize

- Horne Insights

- Lexis Nexis

Read More

Transformation Readiness

70% of all planned transformation initiatives fail to deliver tangible business value and 84% of organizations fail at tech transformations in particular.

Rethinking the Future of your Business

The economic climate is becoming increasingly uncertain with cautionary signals of recession, along with inflationary pressure, fluctuating currencies, and uncontrollable impact of geopolitical events. Firms need to proactively take this opportunity to refocus their future investments on high value, high potential business lines.

Technology and Healthcare

Data production in healthcare occurs in different volumes, velocities, and formats by multiple sources – EHR, diagnostic, imaging, claims, billing, medical devices to name a few.

Enterprise Cyber Resilience in a Hybrid World

Cybersecurity incidents are also not only a threat to corporations’ internal operations and bottom line; customer personally identifiable information and financial data is also at serious risk of exposure and misuse, in turn impacting customer perception and long-term brand loyalty.

Finding Growth in US Insurance

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Data-Driven Post-Merger Integration

A common misconception is that revenue synergies are illusive or “icing on the cake”, primarily because they are more challenging to quantify.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

Platformization of Health Tech

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously

Are Your Vendor Risks Under Control?

Investing in vendor risk management today can secure a future brimming with cost-effective, secure, successful and trust-worthy partnerships.

(AI)ntelligent Procurement

In a competitive business environment, high-performing CPOs are 18x more likely to fully deploy AI/cognitive capabilities. This typically leads to 92% faster demand forecasting, on average 350 man-hours are saved through automation, and there is a potential for 24/7 operations

Realizing Your Workforce Strategy

Organizations are now recognizing the limitations in their workforce programs, so are making a concerted effort to develop a contingent workforce strategy, consolidate their master vendors/staffing agencies, and extract maximum benefits from the program.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Getting the Basics Right

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Embracing Open Banking

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

Ensuring Loyalty of your Prized Clients

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

The Cloud-Native Paradigm

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Business Analytics in Pandemic Times

Strategic direction is evolving rapidly during COVID-19. Businesses are struggling with ways to respond to the pandemic and have numerous challenges facing them including potentially significant revenue shifts, interaction changes and resource limitations.

Fortunately, organizations can analyze readily available data by using both business and data intelligence to better serve their customers.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Reshaping Wealth Tech

Before the Covid-19 inducted recession, the wealth tech sector was already experiencing a slowdown - both in the number of new startups and total capital raised. Now more than ever, investors and operators must be bold in re-inventing their Firm's long-term value proposition.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

How to Thrive in the New Normal

Now that Business As Usual is unusual, leaders are forced to re-imagine business models and build ‘winning strategies’ - to not only survive the pandemic but also emerge as successful change-makers, shaping an altered business reality.

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Trends in Digitalization of Insurance

For some, Insurance might seem a monolithic industry, but for the ones keeping a close eye on it- Insurance is revamping itself faster than ever!

From days when underwriting a simple policy would take weeks and months, to now when it can be done in seconds with a simple ‘selfie’ - there seem to be no bounds in the future of this industry.

Customer Engagement Index

While firms have found tremendous success in using these loyalty metrics to successfully grow customer relationships, they are lagging indicators and provide little help in providing immediate insight into whether or not improvements and initiatives are moving the needle.

Strategic Sourcing of a “Difficult” Spend Category

Some clients have even deemed spend reduction in procurement categories like legal services, where recourses and expertise are concentrated within humans not technology, to be intractable. At Kepler Cannon, we continuously challenge these sorts of conventional wisdom.

Third Party Information Risk Mitigation

It is well known that one way to make better predictions about how your customers, distributors and suppliers will behave, is to augment your own data with that of third parties.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Reducing Strategic Over-Dependence on IT Vendors

Over time, many firms realize that they have become so reliant on vendors/contractor for critical knowledge on key applications, that they have, in fact, ceded control of those applications to the vendors.

Are Blockchains Evolving Like Securities Exchanges?

Driven by data security concerns, a majority of financial institutions are now looking at so-called private or hybrid blockchains, rather than fully decentralized public blockchains (like the blockchain used for Bitcoin)

How Global Resourcing May Be Killing Your Company’s Efficiency

As global firms respond to the post-Great Recession regulatory and economic realities, efficiency of the back-office has become critical to ongoing success.

Third Party Vendor Risk – A Continuous Mitigation Strategy

The last thing any multinational organization wants to worry about are business and compliance risks introduced by third party vendors.

Everything You Wanted to Know About Blockchain (But Were Too Afraid to Ask)

As cryptocurrencies and their underlying ledger system gain momentum, many financial institutions are trying to determine how to best be part of this revolution. In particular, they want to know how best to update their existing IT architectures and operations to capitalize on this new technology.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

Enabling Growth through Practice Management

In the world of financial advisory, growth strategies often focus squarely on the end client; after all, growth is achieved through new client acquisition or new asset acquisition from existing clients. While this logic is not incorrect, it fails to acknowledge the intricacies of third party distribution.

Reshaping the Indian Life Insurance Market

The Indian life insurance market is the fifth largest in the world. Although the per capita premium remains lower than in other emerging markets, the size and growth of India’s working class remains one of the largest globally, presenting enormous opportunity for life insurance companies to expand into and within the Indian market.

The Growing Asian Wealth Management Market: Capturing the Mass Affluent Opportunity

One of the largest and fastest growing wealth segments, the Asian mass affluent, is projected to hold $43.3 trillion in assets by 2020, yet only 20% of all wealth in Asia is tapped by the wealth management industry.

(Not) Selling Life Insurance in Asia

Amidst a boom in insurance business, Asian consumers remain largely underinsured.

Role Reversal: The Future of US Banks in the Online Lending Market

Following the financial crisis in 2008, Fintech startups gained a lot of prominence globally as consumers started to look for alternatives to traditional banking methods. These startups have penetrated every service area of consumer retail banking with the goal of dis-intermediating banks and becoming the new leaders of the financial services industry.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.