Agentic Commerce: AI in Your Wallet

For the first time, the entity browsing products, comparing prices, and initiating checkout is not a human; it’s software acting with delegated authority. In mid-2025, major card networks and processors began rolling out a fundamentally new capability: AI agents that authenticate, tokenize payment credentials, and complete purchases without human intervention.

Agentic commerce = the authorization of AI agents to discover, compare, negotiate, and complete purchases on behalf of consumers or businesses. For example: AI doesn’t just recommend a Mother’s Day gift, it finds options within your budget, selects one based on your preferences, and completes the transaction using a tokenized payment credential. All you do is approve (or set rules once, and let it run).

A chatbot can suggest a product, but an agentic system can actually buy it. The distinction is that authentication, tokenization, and pre-authorized spending authority make agentic commerce a payments infrastructure challenge, not just an advancement in user experience.

In 2025-2026, the payments industry has responded with four closely coordinated capability layers. Card networks launched “intelligent commerce” frameworks (Visa TAP, Mastercard Agent Pay): authentication and tokenization designed for agent-initiated transactions, rather than human-in-browser checkout. Orchestration platforms (Stripe, Adyen, Shopify) built catalog APIs and offer-generation systems that make merchant inventory legible to AI agents in real time. Merchant Agents are emerging: bespoke systems that merchants deploy to negotiate outcomes, manage inventory, and maintain brand voice across AI platforms. And processors are building Payment Agent intelligence, with AI-driven routing, fraud detection, and authorization optimization specifically calibrated for non-human transaction patterns.

The overarching goal is to provide the rails, trust layer, and merchant connectivity, so agents can transact independently, and safely, at scale (1). Without this unified experience, agents can simply route transactions through cheaper, more programmable infrastructure that bypasses traditional networks and processors entirely, leaving incumbents watching from the sidelines as payments shift to new rails.

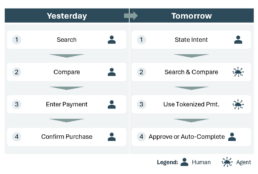

Exhibit 1. How Agentic Commerce Changes Shopping

How Agentic Commerce Rewires Commerce

For leaders across payments, retail, and financial services, this rewiring of commerce raises urgent, non-deferrable strategic imperatives.

Trust

When software is spending customer money, how do networks and processors prove the transaction is legitimate? The authentication models built for human-in-browser checkout don’t translate cleanly to agent-initiated flows.

Behavior

AI agents operate at machine speed and scale. They can comparison-shop across dozens of merchants in milliseconds, renegotiate subscriptions automatically, and aggregate purchases in ways that traditional fraud models may flag as suspicious. Will current risk infrastructure recognize agent behavior as legitimate, or block it as fraud?

Control

Whoever owns the agent relationship controls demand and the pre-checkout decision. If payments networks and processors don’t embed themselves as the trusted authentication and settlement layer, agents may route around them entirely, choosing cheaper, more programmable alternatives.

The implications extend far beyond payments infrastructure. Merchants must build agent-readable catalogs and, increasingly, bespoke Merchant Agents that actively negotiate outcomes rather than wait to be discovered. Consumers need transparent controls, spend limits, and audit logs to trust agents with delegated spending authority. Regulators are beginning to ask hard questions about consent, liability, and consumer protection when the “buyer” is software. The window to shape this architecture is open.

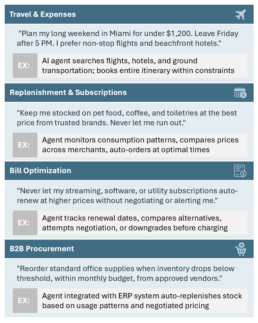

Exhibit 2. Agentic Commerce in Action

More Than Checkout Acceleration

Every payments system built in the last 30 years assumes a human is reading screens, clicking buttons, and consciously authorizing each transaction. That assumption runs through everything from 3-D Secure workflows, to fraud detection models, to dispute resolution processes.

Agentic commerce breaks this assumption. The buyer is software operating under pre-agreed rules, changing core commerce fundamentals.

The next 18-24 months determine who sets the infrastructure rules. The stakes differ by player. For networks such as Visa & Mastercard: will their legacy authentication and tokenization infrastructure become the default trust fabric for agentic transactions, or will alternative schemes (e.g., Google’s Agent Payments Protocol, Apple’s proprietary flows) fragment the ecosystem and reduce dependence? For processors: agents don’t care about legacy relationships; they optimize for speed, cost, and API simplicity. Traditional processors risk being routed around unless they build compelling orchestration capabilities. For merchants: brand loyalty and margin are under structural pressure when agents comparison-shop in milliseconds. Merchants who build Merchant Agents (bespoke systems that negotiate, adjust, and maintain agent-readable catalogs) will outperform those who simply offer a static catalog. For banks: When customers see unexpected charges from agent-initiated purchases, audit trails and real-time alerts become trust advantages that mitigate chargebacks, not compliance costs.

Those who embed themselves as essential infrastructure in the agent-to-merchant-to-network flow will capture outsized share of a multi-billion dollar incremental revenue pool. Those who treat this as “just another checkout method” risk becoming optional routing choices that agents optimize around.

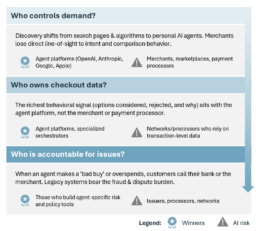

Exhibit 3. Structural Shifts from Agentic Commerce

How Infrastructure Enables Agentic Commerce

The structural shifts outlined above are powered by a four-layer agentic infrastructure stack. Each layer answers a different question about how value flows from consumer intent, to merchant fulfillment, to payment settlement. Understanding who controls each layer reveals where the leverage lies, where the revenue will concentrate, and which players are at risk.

Layer 1: Consumer & AI Platforms

At the top sits the AI agent itself, where consumers express intent in natural language. By late 2025, public platforms like ChatGPT, Perplexity, Claude, and Gemini had become major discovery channels, influencing which merchants consumers visit before they ever reach a website.

Unlike humans, AI agents do not scroll or interpret visual hierarchy, they extract structured data from feeds, APIs, and schema.org markup. A merchant’s homepage, banner ads, and UX flows carry little weight for an agent. Instead, agents evaluate products as rows in a table with attributes, prices, availability, and policies they can parse and compare across dozens of merchants in milliseconds. Merchants with near-complete attribute coverage in their product feed report higher AI visibility; agents routinely skip products with missing shipping windows, sizing, or return policies. For payments networks and processors, this creates a fundamental problem: you don’t see the customer until after the agent has already made the routing decision. The most powerful signal: what the consumer considered, what was rejected, and why – sits with the agent platform, not you.

Layer 2: Merchant Agents & Orchestration

The second layer is where the public AI agent and the merchant actually connect. This is where Stripe’s Agentic Commerce Protocol (ACP), Google’s Agent Payments Protocol (AP2), and Shopify’s Universal Commerce Protocol are competing to become the universal translation layer. But the Merchant Agent is emerging as a key sub-component. When a public agent arrives with a request, e.g., “a $120 running shoe shipping by Tuesday” a merchant agent interprets that intent, maps it to the merchant’s live catalog and logistics, and assembles the best offer the merchant can make. It manages real-time inventory, selects the optimal fulfillment path, applies promotions, and maintains brand voice. Rather than leaving it to the public agent to scrape pages and guess, merchant agents become active negotiating counterparts. Over time, they will surface real-time inventory, pricing, and risk signals that PSPs and card networks can optimize against, making them the default interface to merchants. Merchants who build bespoke agents to actively shape transactions will win the margin, others will compete on price alone (2).

Exhibit 4. Four Layers of Agentic Infrastructure

Layer 3: Payment Agents (PSPs)

Processors and payment platforms are evolving beyond rails into operational centers. Payment agents handle fraud detection, routing optimization, authorization performance, dispute management, reconciliation, and compliance enforcement across thousands of merchants and millions of transactions. Key controls include: checkout and funding – approve/decline decisions and fraud signal interpretation in real time; (2) authorization and routing – AI-driven routing that can reduce fraud losses for revenue uplifts; and (3) post-payment controls such as chargeback validation and liquidity management. PSPs can become a shared asset for merchants who want agentic capabilities without building the infrastructure themselves.

Layer 4: Trust and Standards

Card networks are evolving from passive rails into intelligent orchestration layers. Visa’s Trusted Agent Protocol (TAP), built with Cloudflare, provides verification for AI agents, allowing merchants and PSPs to distinguish trusted agents from malicious automation. Mastercard’s Agent Pay, when partnered with Microsoft, IBM, and Google, provides special credentials that prove “I am ChatGPT acting for John S.” Scheme agents detect agent traffic through cloud IPs, automation fingerprints, and protocol flags, then apply agent-specific authentication rules. A new “agent-present” transaction category is emerging alongside the online transaction ‘card-not-present’ classification. Agent-present does not equate to card-not-present; agent-initiated purchases lack the fingerprints, IP geolocation, and behavioral signals that CNP fraud engines rely on. Networks must move toward broad adoption of these standards, with clear liability rules defining what happens when an authorized agent makes a harmful decision.

The Agentic Market Opportunity

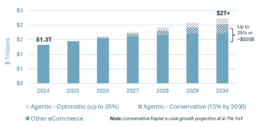

Independent market forecasts from leading firms converge on a striking consensus: by 2030, AI agents could control up to 15-25% of all U.S. e-commerce transactions1.

U.S. e-commerce is projected to exceed ~$2.0 trillion by 2030. If agents capture 15-25% of that market, agentic commerce will represent $300-500 billion in U.S. transactions annually by the end of the decade (1). Using this range and applying standard payments economics, the revenue opportunity becomes clear:

– A net-new payments revenue channel across authentication, authorization, processing, fraud prevention, and dispute resolution

– Hundreds of millions in incremental orchestration revenue (session-level analytics, catalog normalization, agent value-added services that don’t depend on transaction volume alone)

– Hundreds of millions of new authorization requests annually requiring real-time agent authentication, policy enforcement, and non-human fraud detection

Agentic commerce represents net-new revenue for players in the payments ecosystem, that is, if incumbents position themselves to capture it. For those who don’t, this attractive revenue channel will flow to their competitors who did.

The early signals are impressive. ChatGPT already fields ~50 million shopping-related queries per day (2% of its ~2.5 billion daily prompts). At even a conservative 5% conversion rate, that’s 2.5 million potential daily orders from ChatGPT alone2. AI-driven retail traffic also surged 1,200% year-over-year as of October 2025 while traditional search’s share of retail discovery continues to erode (3). And because agents “ride the rails” of existing infrastructure – meaning no new apps for consumers, no rebuilt checkout flows for merchants – adoption curves will scale faster than mobile payments or contactless.

For payments networks and processors, even capturing 5-10% of this incremental market represents billions in new annual revenue by 2030. Those who move decisively in 2026-2027, embedding agent authentication, building orchestration capabilities, and shaping industry standards, will capture disproportionate share. Those who wait will compete on price alone in commoditized payment and settlement services.

Exhibit 5. U.S. e-Commerce Revenue & Agentic Commerce Projections (1, 4)

Risks, Governance and Responsible Autonomy

As autonomy grows, so does the need for disciplined risk management. Agentic systems introduce unique failure modes, including goal misalignment, tool misuse (such as acting in the wrong environment or on the wrong dataset), hallucinated context, and uncontrolled loops after context changes.

To address these risks, organizations are translating policy into concrete, enforceable guardrails at the agent level, embedded directly into operational workflows such as the access removal process illustrated in Exhibit 4:

These guardrails help ensure that agents operate safely, reliably, and in alignment with organizational policies, while still allowing for scalable, automated decision-making.

– Policy boundaries: Defining what agents do without human approval (e.g., financial thresholds, data access limits, transaction scope).

– Escalation rules: Triggering human review based on confidence scores, dollar amounts, user types, or data sensitivity.

– Simulation and sandboxing: Testing new workflows against synthetic or recorded data before production.

– Circuit breakers: Automatically halting agents when monitoring detects anomalous patterns, unexpected volumes, or conflicting signals, forcing manual review.

Regulators and risk bodies consistently emphasize that AI and agents should fit within model risk management and governance frameworks rather than bypass them. In practice, this means defining clear accountability for agent behavior, maintaining audit trails and explainability, and enforcing segregation of duties even when decisions are automated.

When compliance, risk, and governance teams are involved from the outset, they become enablers of responsible autonomy rather than gatekeepers. Their participation allows organizations to push further along the autonomy curve with confidence, knowing that control and accountability remain intact as orchestration shifts from humans to agents.

Agentic Roadmap

Realizing value from Agentic AI requires a structured path that aligns technology, processes, and governance. This begins with a focused diagnostic to quantify coordination drag, map cross-system workflows, and identify policy-constrained segments. The outcome is a prioritized set of attainable opportunities, autonomy boundaries, and risk profiles.

Early adoption favors depth over breadth. Organizations typically pilot one autonomous workflow per major function (e.g., IT, finance, operations, HR) under explicit guardrails. Common starting points include password resets, variance preparation, and standard onboarding. Each pilot incorporates observability, human-in-the-loop controls, and outcome-based metrics (e.g., cycle time, throughput, CSAT) to validate impact and build trust.

Scaling depends on standardization, not custom-made builds. Enterprises institutionalize Agentic AI through reusable agent libraries, domain-specific memory, and shared monitoring infrastructure. At scale, consistent context management becomes as important as model quality. Standardized protocols provide a common way for agents to encode, share, and update context (e.g., goals, task state, and dependencies), enabling predictable multi-agent coordination and reliable expansion across the enterprise.

Organizations that treat Agentic AI as an operating capability, grounded in standardization, shared context, and governance, are best positioned to scale autonomy responsibly and capture sustained productivity gains.

Conclusion

As agentic AI matures, advantage is shifting from tool adoption to enabling seamless flow of work. Traditional automation optimized tasks but left coordination costs largely intact, limiting its value realization. Agentic workflows address this by translating intent into policy-aligned execution, reducing cross-system friction and manual oversight while improving speed, cost, and predictability.

This shift is already underway, with AI agents in production and investment accelerating. For executives, the immediate priorities are straightforward:

1. Quantify your coordination drag. Identify the three to five highest-volume workflows where handoffs, status checks, and cross-system lookups consume the most time relative to actual value-adding work.

2. Run a bounded pilot. Select one workflow per major function, define explicit guardrails and escalation rules, and measure cycle time, throughput, and error rates before and after.

3. Engage governance early. Bring risk, compliance, and security teams into the design process, not as reviewers at the end, but as co-designers of autonomy boundaries.

4. Invest in the platform, not just the pilot. Build reusable components, shared memory infrastructure, and standardized integration patterns that allow pilots to scale without rebuilding from scratch.

Organizations that act first by redesigning high-drag workflows with governance will convert coordination overhead into competitive advantage.

- PWC, Global Workforce Survey, 2025

- Precedence Research, Agentic AI Market Size, 2025

- International Journal of Advanced Computer Science and Applications

- Forrester, AI Centric Service Desk Results, 2025

- PWC, AI Agent Survey, 2025