The Inflection Point

Digital wallets have fundamentally transformed the way people pay, ushering a new era in convenience and flexibility for payments. Users can store all their payment information on their devices, allowing them to simply tap or scan to make a payment. Whether it’s swiping through different options to pay through your smartphone, topping up mobile accounts, paying your friend for your portion of last night’s dinner, or paying for your groceries with the tap of your phone, digital wallets have made the payment experience even more seamless.

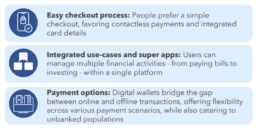

This evolution has propelled digital wallets to the forefront of consumer and business preferences. With their unmatched convenience and versatility, digital wallet have set a new standard for how transactions are conducted. Here are some key drivers on how digital wallets have surged to the top payment method:

The impacts of this shift are diverse and increasingly evident across the financial sector. Issuers are seeing a decline in traditional card usage as consumers favor the convenience and security of digital wallets. On the other hand, acquirers are adapting by accepting more digital wallet transactions by the day.

Financial institutions must recognize these factors and adapt accordingly to stay competitive and ahead of the game. By integrating digital wallet solutions into their offerings, financial institutions can meet the evolving preferences of consumers and secure their position in the payments landscape.

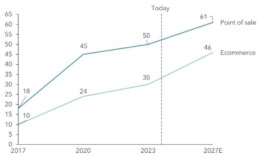

Exhibit 1. Digital Wallets’ Share of Global Transaction Value (1)

Ripple Effects Across The Value Chain

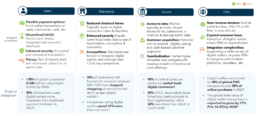

The rise of digital wallets has far-reaching effects on multiple players across the payments value chain. From direct competition with existing revenue streams, such as traditional card transactions, to new opportunities for monetizing transaction data, the impact is both broad and deep. Financial institutions, merchants, payment networks, and even consumers are all influenced by the shift towards digital wallets.

Exhibit 2. Digital Wallet Impact and Adoption Across Key Stakeholders in the Value Chain

Types Of Wallets: Finding The Right Fit For Every Need

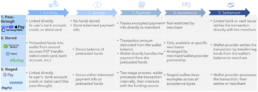

Understanding the different types of digital wallets is crucial for both consumers and businesses. These wallet types – pass-through, stored, and staged – offer varying levels of convenience, security, and functionality that can significantly impact user experience and merchant operations. For consumers, the differences among digital wallet types can affect transaction speed, funding options, and where they can pay. Pass-through wallets act as secure canals, stored wallets maintain user funds, and staged wallets combine elements of both. For merchants, certain wallet types may cater to different types of customer segments and provide different experiences. These distinctions affect everything from transaction speed and flexibility to regulatory compliance and merchant integration, making it essential to grasp their unique characteristics when choosing or implementing digital payment solutions.

Exhibit 3. Types of Wallets and Differentiation across the Value Chain

The digital wallet space is highly competitive for providers, with players adopting distinct strategies to stand out. Some focus on offering vertically integrated solutions, tailoring specific features to targeted customer segments and use cases (e.g., transportation). While others pursue a platform approach, enabling users to access and pay for almost anything online within the wallet. The differentiation and unique use-cases of wallets are what have led them to become so wide-spread.

Exhibit 4. Various Use-Cases across Digital Wallets

Friend Or Foe: Impact Of Wallet Economics On FIs

Digital wallets account for over 50% global e-commerce transactions. Their financial impact has led to several changes in fee structures and revenue models for key payment players. Recognizing and adapting to these shifts is essential for understanding the potential threats and opportunities that digital wallets present to each participant in the transaction value chain.

Opportunities For FIs To Cash-in

The digital wallet market offers financial institutions a chance to innovate and thrive. By leveraging their strengths to create differentiated offerings, they can enhance customer engagement and tap into new revenue streams. The key is to innovate/differentiate themselves in ways that complement, not compete with, their core services—unlocking new opportunities while securing their place in the digital future. Those who adapt quickly will not only maintain relevance but also lead in shaping the next era of financial services.

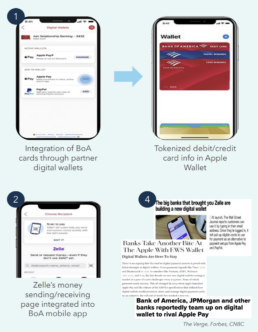

Bank Of America: Evolving Amidst Disruption

In Conclusion

Digital wallets are not so much a strategic option as they are an imperative to survive and thrive in today’s payments landscape. The impact of wallets on Financial Institutions is profound in that they have fundamentally shifted the way consumer make payments. The ripples of their impact on Financial Institutions run wide and deep. They affect multiple players in the value chain, and can either pose as a direct threat, symbiotic partner, or net new offering for Financial Institutions.

The wallet landscape is saturated with various offerings, each with their own value proposition to customers, providers, and partners. Some wallets take a platform approach and develop wallets for every and all types of financial needs, while others offer verticalized solutions that target specific industries, customer segments, or use-cases. Financial Institutions must choose to create or partner with a wallet that suits their specific situation and objective.

Creating a Digital Wallet may be a daunting task, even for the most tech-savvy institution. Hence, not all FIs choose to go down this route. There are other options to tap into the Wallets boom. Players may partner or offer an array of financial products or services to wallet providers. Each option has its own trade-offs. Generally, the closer you are to the customer, the higher the risk and competitive moats. To succeed in this competitive space, Financial Institutions need to carefully plan and execute their foray into the space.

- Worldpay Global Payments Report, 2024

- Juniper Research

- Forbes Advisor

- PYMNTS Intelligence

- Capital One Research

- Bank for International Settlements

- Flagship advisory partners

- Websites of wallet providers

- A fee paid by the merchant’s bank to the cardholder’s bank for processing a card payment.

- The percentage of a sale that a merchant pays to cover processing fees

- A per-transaction charge assessed by payment processors or networks for handling payment.

- Bank of America

- The Verge