The Credit Invisibility Opportunity

The U.S. has one of the most sophisticated credit infrastructures globally – three nationwide bureaus, decades of repayment history, and widespread use of automated underwriting. Yet nearly 45 million adults and most small businesses remain outside the reach of traditional scoring models, according to the CFPB. These are not inactive or high-risk entities. They are active participants in the modern economy whose financial lives simply do not flow into bureau systems.

This disconnect between economic activity and credit visibility has widened as consumer behavior moved toward digital payments, subscription-based spending, and gig-economy earnings – categories that are rich in behavioral signal but poorly represented in bureau records. As a result, there is a paradox of lenders operating in a data-rich economy while making decisions with 20th-century signal sets.

Exhibit 1. Unbanked Population in the US(1)

WHO IS MOST AFFECTED?

Credit invisibility disproportionately affects younger adults, recent immigrants, gig/platform workers, digital-first consumers and SMBs. These exhibit high levels of economic activity, such as, steady rent payments, consistent digital payment behavior, gig income deposits. But these signals rarely reach the credit bureaus. As a result, millions of financially responsible individuals and businesses remain hard to score not due to risk, but due to data representation gaps

Exhibit 2. Target Group

The segments with the richest economic participation – young adults, gig workers, small & freelance businesses – are also the least visible to traditional scoring, creating a blind spot in U.S. credit markets

Traditional Credit Scoring was built for a different economy

WHY TRADITIONAL SCORING NEEDS AN UPLIFT

- The Bureau data pipeline was built for a different economyBureaus mostly ingest lender-reported trades, not day-to-day money behavior. Rent, subscriptions, BNPL, wallets, and gig income sit outside the file — so real financial health goes uncaptured.

- Scores depend on past credit, not present ability-to-payFICO/VantageScore work when history exists, but fail for thin-file users. That creates circular exclusion: you need credit to get credit, even if your cash-flow is strong.

- Modern repayment structures break legacy assumptionsToday’s repayment is fragmented and real-time (micro-payments, split bills, recurring debits). Legacy models assume fixed monthly cycles, so they misread modern patterns.

- Disproportionate impact on historically excluded groupsThis is a data inheritance problem: groups historically shut out of formal credit remain underrepresented in bureau files. The result is under-scoring due to missing signals, not higher true risk.

THE UNLOCK

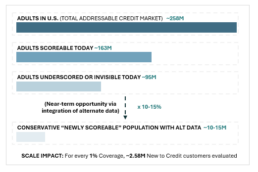

Alternate data can meaningfully expand who is “scoreable” by capturing financial behavior that bureaus miss. In the U.S., this directly targets the credit-invisible population (and a wider thin-file segment), creating a material inclusion unlock at scale; even small gains in coverage translate into millions of additional credit evaluations.

Exhibit 3. Credit Visibility Gap

Beyond access, alternate data improves underwriting quality by shifting the risk lens from static credit history to dynamic financial health. Cash-flow signals (income stability, volatility, residual liquidity, and repayment behavior) increase separation between resilient and fragile borrowers, enabling sharper risk-based pricing rather than blanket declines. The same signals also strengthen fraud detection through behavioral consistency checks and enable portfolio monitoring via early-warning triggers, making alternative data not just an inclusion lever but a modernization of core credit infrastructure.

Enter- Alt(ernate) Data

WHAT QUALIFIES AS ALT DATA?

Alternative data refers to credit-relevant information not traditionally captured in standard bureau scoring inputs—especially signals that reflect how a consumer earns, pays, and manages cash flow in real life. This commonly includes bank-account cash-flow data, income and employment verification, rent and utility payment history, and other recurring obligations that many consumers pay reliably but that may never appear as credit trades.

Done well, alternative data does not replace the bureau file—it fills the visibility gaps for thin-file and new-to-credit consumers, and can sharpen underwriting even for fully scored borrowers by adding “current-state” behavioral context

Exhibit 4. Leading Data Types & Data Matrix

Exhibit 5.Value Unlocked with Alternate Data

Noteworthy Examples

DATA TYPES USED

Traditional bureau data plus :

- Employment and income indicators

- Education and career trajectory proxies

- Other non-traditional variables that improve risk separation

HOW IT IS USED

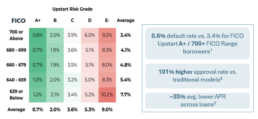

Upstart trains machine-learning models to predict probability of default rather than rely on fixed score thresholds. Borrowers are evaluated holistically, allowing higher approval rates, risk-adjusted pricing, lower APRs for some underserved borrowers.

DATA TYPES USED

- Bank account transaction data (via open banking integrations)

- Income inflows

- Expense regularity

- Balance volatility

- Savings behavior

HOW IT IS USED

Petal builds a cash-flow-based risk score (often referred to as CashScore) to estimate repayment ability. This score can be generated even when no traditional credit history exists.

Credit limits and pricing are adjusted based on observed financial stability, not just credit history length.

DATA TYPES USED

Traditional bureau data plus :

- Telecommunication

- Student Information

- Alternative Credit

- Transaction History

HOW IT IS USED

Socure verifies identity instantly via non‑document signals (email/phone graphs, behavioral biometrics), bringing the verification speed down to a P95 of 1.5 seconds1, compared to the industry average of more than 30 seconds.

DATA TYPES USED

- Bank account transaction data (via open banking integrations)

- Income inflows

- Employment Verification

- Cash Flow Data

- Utility Payments History

HOW IT IS USED

Alloy integrates alternative data into real-time ML models for credit underwriting and fraud prevention. It orchestrates all sources via a single API: traditional signals (bureaus, IDs) combine with alt data to assess repayment ability for thin-file users (gig workers, SMBs), enabling auto-approvals while flagging synthetics

Implementation Considerations

The Plug & Play Model

Institutions do not “implement alternative data” in one step. They assemble a custom decisioning stack by choosing a business wedge, selecting an operating model, plugging in the right data blocks, and inserting them into the decision flow with governance baked in before scaling.

Conclusion

Credit scoring in the U.S. was built for an earlier financial reality – one defined by traditional lending products, periodic payments, and lender-reported data. That model no longer reflects how millions of consumers earn, spend, and manage money today. As financial activity increasingly flows through digital payments, subscriptions, gig income, and real-time cash movements, the gap between economic participation and credit visibility continues to widen .

Alternative data offers a practical way to close this gap. It expands credit visibility for thin-file and new-to-credit consumers while improving risk precision for lenders. Importantly, this evolution does not require abandoning traditional bureau frameworks. The most effective approaches integrate alternative signals alongside existing scores – enhancing decision quality, improving segmentation, and unlocking new lending opportunities without increasing portfolio risk.

For financial institutions, the question is no longer whether alternative data belongs in credit decisioning, but how to implement it responsibly and at scale. Success will depend on choosing the right operating model, embedding governance and explainability from the outset, and aligning data strategy with regulatory expectations. Over time, credit decisioning will move toward more adaptive, real-time models that continuously reflect a consumer’s evolving financial health, rather than static point-in-time assessments. Institutions that move deliberately – balancing innovation with discipline – will be best positioned to modernize credit access, strengthen portfolio resilience, and ensure that creditworthiness reflects real economic behavior.