Research Overview

The global datacenter industry is undergoing a structural transformation unlike anything seen since the cloud computing revolution of the 2010s. Artificial intelligence in particular has made compute infrastructure a hot commodity, driving demand for datacenter space that far outpaces current capacity to build it.

Into this gap has stepped private credit, where firms like Blackstone, Apollo, and Blue Owl are deploying tens of billions of dollars to fund a new generation of datacenter acquisitions, expansions, and retrofits. An existing datacenter owner can take advantage of this demand through a sale-leaseback, where the owner sells their datacenter facility to an investor and simultaneously leases it back, transforming a capital asset into a predictable operating expense while receiving a large upfront cash payment.

Why Space is at a Premium

To understand why private capital is rushing into the datacenter sector, one must first understand the scale of the demand shock that AI has delivered. Over the past few years, demand has surged for AI models deployed across enterprise workflows and consumer applications alike. Training and running large AI models is extraordinarily compute-intensive, and compute is inseparable from the physical infrastructure that houses it.

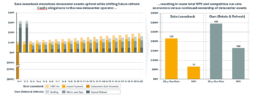

Exhibit 1. Data Center Investment & Density

The AI Compute Imperative

Modern AI accelerators, such as NVIDIA’s H100 and B200 GPUs, operate at extreme power densities with a single rack consuming over 120 kilowatts, or 10-20x that of traditional compute. (4) Many existing enterprise datacenters, built in the early 2000s for air-cooled servers are functionally unable to host modern AI hardware without expensive retrofits. To accommodate the power draw, air-cooling is being replaced with liquid cooling and bringing with it a wholesale shift in datacenter infrastructure.

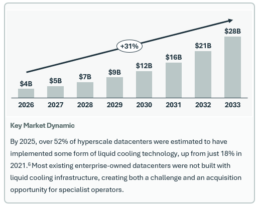

Exhibit 2. Global Liquid Cooling Market(5)

Supply Constraints

Building a new hyperscale datacenter from the ground up is an 18–36 month endeavor under optimal conditions. (7) Power connectivity is the most acute bottleneck: connecting a large campus to the electrical grid can take 8–10 years in many jurisdictions due to utility planning cycles and infrastructure backlogs.(8) This makes existing datacenters, even aging ones, extraordinarily valuable, since they already have power, fiber, and permits in place.

Private Credit Enters the Datacenter Space

Institutional private credit has identified the datacenter sector as one of the most compelling long-term infrastructure investment opportunities of this decade. The reasons are structural: long-duration leases with creditworthy tenants, mission-critical assets with high switching costs, demand growth driven by cloud, AI, and enterprise digitalization, and the ability to deploy very large sums into a single transaction.

Why Private Credit, Not Just Private Equity

While private equity firms acquire datacenter platforms outright (as Blackstone did with QTS Realty Trust and AirTrunk), private credit plays a complementary and increasingly important role. Credit vehicles can provide debt financing to datacenter operators who need capital quickly and at scale, without requiring the operator to cede equity. This structure is ideal for:

- New Construction & Expansion: Provides capital to fund greenfield builds and capacity scale-ups without diluting operator equity

- Large-Scale Retrofits: Finances critical infrastructure upgrades such as power capacity additions and liquid cooling installations

- Portfolio Acquisitions: Enables operators to acquire existing datacenter assets and integrate them into a broader platform strategy

- Bridge Financing: Fills the gap between a sale-leaseback close and the placement of permanent long-term debt

The Sale-Leaseback Mechanism

The sale-leaseback is the cornerstone transaction structure in this playbook. In a datacenter sale-leaseback, an enterprise that owns its own facility sells that building (and often the associated power and cooling infrastructure) to a specialist datacenter operator or investment vehicle. The selling enterprise simultaneously signs a lease, typically structured as a triple-net (NNN) lease, allowing it to continue using the facility exactly as before. The only change is the name on the deed.

Exhibit 3. Sale-Leaseback Transaction Flow

What the Operator Gets

For the datacenter operator backed by private credit, the sale-leaseback delivers an immediate, revenue generating asset with a creditworthy anchor tenant already in place. The operator can then leverage the facility as a platform, upgrading unused capacity, installing liquid cooling infrastructure, and leasing additional space to new tenants. The private credit backer earns a yield on the debt it has provided, secured by the underlying real estate and the lease cash flows.

Exhibit 4. Notable Blackstone Datacenter Deals (9) (10) (11)

Why Enterprises are Selling

Many enterprises, from financial institutions to telecoms and beyond, built their datacenters in the early 2000s to house technology that was then central to their business model. Two decades later, the world has changed dramatically: cloud computing has absorbed many workloads, staff with specialist datacenter skills have become scarce and expensive, and the capital required to upgrade legacy facilities is significant.

The Core Motivations

A.Unlocking Trapped Equity: Datacenters in Tier-1 markets have appreciated significantly. An enterprise may have built a facility for $50 million in 2003 that is now worth $200 million or more. A sale-leaseback allows the company to crystallize that gain and redeploy the capital.

B.Converting CapEx to OpEx: Owning a datacenter requires periodic capital replacement on 10–15 year cycles. A sale-leaseback converts unpredictable CapEx into steady OpEx, improving financial planning.

C.Escaping the Refresh Dilemma: Older facilities face major capital refresh cycles. Rather than invest $30–80M into a non-core asset, many prefer to sell at peak value and let a specialist operator bear the cost.

D.Right-Sizing Usage: Enterprises typically use only 60–70% of capacity.(12) A sale-leaseback allows environment right-sizing while avoiding the long timelines and costs associated with a cloud or colocation migration.

E.Economies of Scale in Operations: Specialist operators achieve economies of scale in labor, maintenance, and procurement by pooling fixed roles and leveraging portfolio-wide purchasing power and designs.

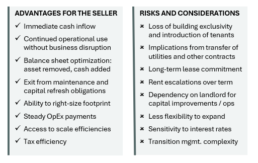

Pros, Cons & Considerations

Exhibit 5. Advantages & Risks to Sellers

It is important to note that the attractiveness of sale-leaseback valuations is sensitive to interest rates. Class A facility cap rates have typically ranged from 100 to 150 basis points (bps) above the 10-yr Treasury yield, while older facilities requiring significant upgrades can trade up to 550 to 600 bps above the 10-yr Treasury.(13) Since 2022, rising rates have pushed cap rates higher, compressing prices. However, the scarcity value of powered, connected real estate has kept prices elevated despite the higher-rate environment.

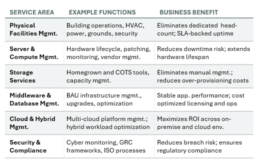

Role of Specialist Operators

One of the most overlooked components of a sale-leaseback is what happens operationally post-close. When an enterprise has owned its facility for 20+ years, it has typically accumulated a large team of dedicated facility staff. A new operator, looking to rationalize costs and professionalize operations, will often seek to transition responsibilities to a specialist MSP.

The Case for Outsourced Datacenter Operations

Existing global technology services firms offer comprehensive datacenter management services from physical facilities operations through to core IT operations. This operating model has become popular in datacenter acquisitions for the following reasons:

Exhibit 6. Benefits of Utilizing Outsourcer by Service Area

The Transition Playbook

A successful facility management transition in the context of a sale-leaseback typically follows a structured phased approach:

Discovery & Assessment (Weeks 1–4): The managed services provider conducts a full audit of the facility: physical plant condition, power and cooling infrastructure, IT asset inventory, staffing levels, existing contracts, and compliance posture. SLA baselines are established.

Knowledge Transfer & Parallel Running (Weeks 4–12): Existing staff and processes are documented. The MSP team shadows operations, taking over monitoring and incident response while the incumbent team remains available. Automation tools are deployed to replace manual processes.

Cutover & Stabilization (Weeks 12–24): Full operational responsibility transfers to the MSP. Staff rationalization occurs with some resources offered positions within the MSP while others may be redeployed elsewhere in the enterprise. SLA performance is monitored against agreed metrics.

Optimization & Continuous Improvement (Ongoing): The MSP applies best practices, automation, and scale efficiencies to drive down cost and improve performance. Regular reviews align service delivery to the evolving needs of both the enterprise tenant and the new datacenter owner.

Making the Numbers Work

One of the most powerful arguments for the sale-leaseback is the net present value (NPV) analysis. In terms of the NPV, the contribution of the cash injection up front and/or the removal of capital outlay to refresh a datacenter is significant enough to make the long-term lease payments well worthwhile. The NPV case typically rests on four pillars:

1.Immediate cash release: If the enterprise receives $80 million today and can deploy it at a 12% return in its core business, the opportunity cost of retaining ownership is substantial.

2.Discount rate differential: The lease payments, discounted at the enterprise’s cost of capital, often have a lower NPV than the total cost of ownership (capital refresh + operating costs + opportunity cost).

3.CapEx avoidance: Significant required capital investment in the near-term (e.g., an impending datacenter refresh) poses a major hit to NPV; converting this into a lease over time frees up capital for immediate use.

4.Tax flexibility: Lease payments are fully deductible as incurred, providing an immediate tax shield. Ownership can offer comparable benefits under current bonus depreciation rules, but only for operators with the taxable income and cost of capital to justify the investment.

Exhibit 7. Illustrative Cost Comparison: Lease vs. Buyback

Hypothetical 20-year analysis $80M Facility 7% Discount Rate

The Road Ahead

Private Credit also Supporting Greenfield Builds

Beyond acquiring existing assets, private credit is increasingly funding greenfield construction. Meta’s $29 billion data center expansion project funded by Blue Owl and PIMCO exemplifies this trend. (14)The model of co-locating datacenters with dedicated power generation assets, thereby bypassing the 7–10 year grid interconnection queue, is likely to become a template for large-scale AI infrastructure development.

AI Premium on Liquid-Cooled Facilities

Turnkey AI compatible datacenters, with liquid cooling, high-density power, and heightened structural integrity, are seeing the sharpest demand spikes and commanding valuation premiums.(15)This is only expected to intensify as AI demand proliferates.

Conclusion

The convergence of AI-driven demand, private capital seeking long-duration yield, and enterprise desire to optimize balance sheets has created one of the most dynamic capital markets stories in digital infrastructure. The sale-leaseback is not a new financial tool, but its application to the datacenter sector combined with the managed services model represents a shift in how compute infrastructure is financed, owned, and operated.

Enterprises with owned datacenter assets would do well to assess their options carefully. An attractive sale price, NPV-favorable lease terms, and a well-managed operational transition may represent a significantly better outcome than continued ownership of an increasingly non-core asset.

- McKinsey, The Cost of Compute Power, 2025

- S&P Global Intelligence Report, 2025

- AFCOM, State of the Data Center Report, 2024

- Face of IT Tech Report, NVIDIA GPU Comparisons, 2025

- Markets&Markets, Hyperscale Datacenter Report, 2025

- IDC, 2025

- CBRE, 2025

- JLL, 2025

- Blackstone News, 2025

- Colovore News, 2025

- Reuters Business News, 2025

- Kepler Research & Analysis, 2026

- CBRE & Kepler Research & Analysis, 2026

- Reuters Business News, 2025

- CBRE, 2025