Prologue

In December of 2024, Visa unveiled its Web3 Loyalty Engagement Solution that leverages AI to transform customer loyalty by tailoring customer offers based on preferences, historical data, and social media activity. This loyalty program innovation enhances Visa’s value-added services, which accounts for a third of Visa’s revenue.

Meanwhile, HSBC has been innovating since 2018, using AI in its credit card loyalty program in partnership with Maritz Motivation Solutions to deliver personalized offers to over 75,000 cardholders – a strategy that earned them the prestigious 2019 Grand Motivation Master award.

Introduction

Thanks to digital leaders such as Amazon, Netflix, Nike, and Spotify, customers have grown to expect and desire personalized experiences, and that expectation is no different when it comes to customer offers, particularly among financial institutions.

89% of customers are interested in receiving personalized merchant offers from their credit card, but only 44% of consumers find their offers very relevant. This creates a dangerous situation for attrition, with 41% of consumers stating that they will switch credit cards if their need for personalized merchant offers are not being met.

Given the customer demand for personalized offers, and the threat to financial institutions of losing cardholders, it is surprising that only 20% of banks state they are doing a good job at it.

For many financial institutions, personalization at scale is extremely challenging. This presents an area of opportunity for AI to step in; through AI, financial institutions have the potential to revolutionize customer retention at scale, driving customer loyalty and ultimately bolstering the bottom line.

Exhibit 1. Consumer Demand for Personalization

The New AI-enabled Loyalty Lifecycle

Artificial intelligence engines have emerged as a key driver of hyper-personalization. Fintechs, issuers, and legacy card networks are among the first to leverage its benefits, ensuring data-driven experiences that maximize customer engagement and profitability. From analyzing customer spend patterns to dynamically tailoring offers in real-time, AI-powered recommendation engines can ensure the right promotion reaches the right customer, at the right moment — throughout every stage of the offer lifecycle (See Exhibit 3). These use cases are examined in further detail below.

STAGE 1: DISCOVER HIGH-IMPACT PARTNERSHIPS

Financial institutions must first identify key merchant partnerships that align with cardmembers’ spending behaviors to drive engagement. Leveraging machine learning and advanced analytics, AI plays a crucial role in this process by analyzing vast datasets, including customer transaction data, to determine high-spend categories, assess potential uplift from partnerships, and evaluating competitive dynamics. For example, AI-powered clustering algorithms can segment customers based on transaction history, revealing category affinities (e.g., frequent travelers vs. high-end retail shoppers). Predictive modeling can then estimate potential engagement and incremental spend for various merchant partnerships by analyzing historical program performance and behavior patterns.

Visa’s multi-year partnership with Analytics Partners, announced in October 2024, is the latest example of this use case. The AI-powered marketing research firm will deliver real-time insights based on Visa’s extraordinary amount of card and consumer transaction data.

Separately, AI-driven recommendation engines can match financial service providers with optimal merchant partners by identifying business with overlapping customer bases and predicting partnership success rates. Natural language processing (NLP) can further enhance this process by analyzing consumer sentiment from online data (e.g., reviews, social media, surveys) to gauge merchant reputation and customer interest. This form of competitive benchmarking can position offerings strategically via automated analyses.

Exhibit 2. Visa & Analytics Partners’ Multi-year Partnership

Exhibit 3. AI-Enabled Loyalty Lifecycle

STAGE 2: DESIGN HYPER-PERSONALIZED LOYALTY PROGRAMS

Exhibit 4 details how travel-related offers could be personalized for varying customer archetypes. For example, older, working professionals may receive more premium travel experiences or perks to incentivize great spend, while younger cardholders are more likely to make use of budget-friendly product offers, tailored to their specific needs.

Whether cashback, points-based, or tiered rewards, AI-automated A/B testing of reward structures can ensure continuous program optimization, by systematically comparing two program elements (i.e. version A vs version B).

By moving from a “one size fits all” approach to a custom, predictive model, AI-powered recommendation engines transform the user experience, not just through personalized offers but also through gamification elements such as milestone bonuses and streaks.

Meanwhile, fraud detection algorithms can flag suspicious redemption behaviors in real-time, mirroring generative AI technology already in use by major card networks, such as Mastercard’s Cyber Secure offerings or Visa’s Advanced Authorization machine-learning models. These programs, in place for both card-present and card-not-present transactions, are a short step away from implementation in loyalty programs.

Exhibit 4. AI-Enabled Travel Offers

STAGE 3: PROMOTE PROGRAMS VIA TARGETED OUTREACH

AI can support effective adoption via personalized, data-driven marketing campaigns, such as by optimizing marketing channels to maximize engagement or leveraging real-time behavioral triggers to share merchant offers based on spending activity.

Real-time behavioral triggers are a highly valuable feature, particularly for targeted merchant offers. By timing certain promotions based off key transaction-based triggers, such as offering category-based travel rewards immediately after a customer books a flight, or geolocation-based triggers, such as sending real-time discounts when a customer is near a partner merchant, AI can significantly enhance engagement by delivering highly relevant, time-sensitive rewards.

STAGE 4: MONITOR & REFINE THE LOYALTY STRATEGY

Financial institutions can also leverage AI to track performance, including engagement, profitability, and retention. AI-powered analytics platforms leverage predictive modelling to anticipate churn risk by detecting disengaged users and triggering targeted retention offers. Separately, AI-driven anomaly detection can identify potential fraud or reward abuse, such as unusual redemption patterns or artificial transaction inflation. To evaluate model performance, recall and accuracy metrics such as F-scores measure how often customers employ targeted merchant offers. Ranking metrics can also inform AI’s effectiveness in its recommendations, while A/B testing can compare various live models to validate improvements post-deployment.

Exhibit 5. AI-enabled Loyalty Program Framework

The Size of the Prize

Personalization through AI in merchant credit card offers can bring significant benefits to both the business and the customer experience.

FOR BUSINESSES:

a) Scalable Personalization: AI can analyze large volumes of transaction data to recommend accurate, personalized offers, enabling personalized offers for a broader audience.

b) Increased Revenue: Companies that excel at personalization can generate 25% more revenue and reduce customer acquisition costs by up to 50%.

c) Increased Loyalty and Retention: With a greater scale of accurate personalization, customers are more likely to stay. Just a 5% increase in retention can increase profit by 25 – 95%.

d) Differentiation in a Competitive Market: Over 40% of consumers are willing to switch credit cards for better personalization.9

FOR CONSUMERS:

a) Enhanced Accuracy: With only 44% of consumers currently finding offers very relevant, AI can help improve data accuracy by up to 80%, making for more accurate personalized offers.6

b) Real-Time Adjustments: By continuously analyzing data and using machine learning algorithms to identify patterns and trends, AI can make real-time changes to its offer recommendations.

c) Tailored Experience: Through accurate and personalized offers, financial institutions can offer a more tailored experience to provide a more engaging customer experience.

Exhibit 6. AI Engine Concept Design

Looking towards the Future

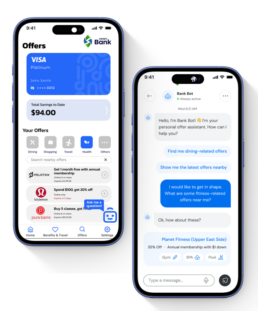

Financial institutions can expand on this use case with an AI-powered chatbot to revolutionize how consumers take advantage of offers (Exhibit 7).

Let’s take John Smith, a Visa cardholder. He is interested in finding offers for fitness classes near him. To do so, he opens the mobile banking app and asks the AI chat bot to recommend fitness-related offers that he can select from, based on his historical transaction data, spend preferences, and location.

Instead of manually browsing through countless promotions that may be irrelevant, John is able to simply describe the type of offer he is looking for, and the chatbot would instantly recommend eligible deals tailored to his needs.

This streamlined approach ensures customers can quickly access relevant offers without the hassle of sifting through hundreds of irrelevant ones, making the experience more efficient and personalized.

In a highly competitive market, an AI-powered chatbot offers distinct advantages by delivering easily accessible personalized offers, helping to attract and retain customers while ultimately driving revenue growth.

To achieve all this, it’s imperative that the building blocks fall into place – those building blocks start with ensuring the seamless integration of AI through all stages of the offer lifecycle. Crucially, ensuring merchant offers are hyper-personalized and accurate towards the consumer.

Exhibit 7. Sample AI-powered Chatbot

Key Challenges

While AI holds the promise of driving significant benefits for both businesses and consumers, enhancing customer loyalty and ultimately strengthening the bottom line, the journey to AI adoption is not without its challenges. To most effectively reap the benefits of AI in loyalty, it is important for issuers to address the following challenges to enhance their AI readiness.

1. POOR DATA QUALITY

AI’s effectiveness is intrinsically tied to the quality of the data it analyzes. Incomplete or incorrect transaction data can hinder AI’s ability to generate accurate, personalized offers. For example, identifying online vs. brick-and-mortar transactions purely from transaction data isn’t a consistent experience. These examples of unclean transaction data can introduce additional noise, biases, and inaccuracies into the LLM training process.

2. DATA PRIVACY CONCERNS

AI’s reliance on data continues to raise concerns about privacy and security. Issuers must ensure compliance with regulations (e.g., Payment Card Industry Data Security Standard), balancing innovation with consumer trust. Additionally, consumers may be hesitant to share certain transaction or geolocation data, thereby reducing the accuracy and effectiveness of AI-enabled personalized offers.

3. MERCHANT RELUCTANCY

Merchant partners may also be hesitant to share proprietary pricing/SKU data significantly inhibiting the extent to which offers may be personalized. For example, an AI-engine may recommend fitness-related offers if a consumer purchases a new pair of shoes from a large retailer. However, without product-specific SKU data, issuers may not be able to detect the exact product (i.e., a new pair of shoes) purchased. This example illustrates the complexity of AI implementation between merchants, technology providers, and financial insinuations.

4. LEGACY INFRASTRUCTURE

Many financial institutions still rely on decades-old core systems, which are often challenging to integrate with AI. For example, most transaction processing occurs in batch mode, creating delays in real-time data access. To address this, several API-based integrations are being developed to enhance system responsiveness. For AI, especially LLMs, modernization efforts are crucial to ensure continuous access to the latest data from multiple sources—including issuers, merchants, and core banking or processor engines, enabling more accurate offers.

In Conclusion

AI in customer loyalty isn’t just a phase, but an inevitable evolution.

The emerging wave of AI adoption in customer loyalty is set to transform the global payments industry, and both innovative fintechs and legacy financial institutions are uniquely positioned to leverage its growth to gain key benefits for both the consumer and the business.

– Enhanced accuracy with real-time adjustments: AI analyzes transaction data at scale to deliver accurate, personalized offers to a wider audience, with the ability to adjust offers in real-time

– Scalable personalization: AI analyzes transaction data to deliver accurate, personalized offers to a larger audience

– Increased loyalty and revenue: Better personalization boosts retention, with just a 5% increase driving profits up by 25–95%

These benefits not only help to explain the rapid growth of AI implementation in financial services but also point to a future where all customer loyalty programs are hyper-personalized and enabled via AI.

By leveraging powerful data analytics and real-time insights, financial institutions can optimize engagement, drive retention, and unlock revenue growth. Meanwhile, overcoming challenges such as data quality, privacy concerns, and outdated tech systems will be essential to fully realizing AI’s potential in this space.

Looking ahead, institutions that embrace AI-powered loyalty programs will be poised to differentiate themselves in a competitive market, ensuring their customers remain engaged and loyal for years to come.