Checkout Leakage Is Structural

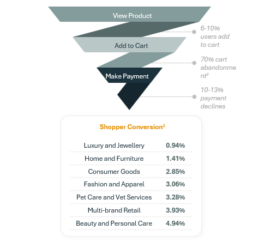

Digital commerce generates over $6 trillion in annual global transaction value, yet significant value leakage persists across the e-commerce journey despite ongoing investments in user experience and payment innovation. An estimated $4 trillion of merchandise is expected to be abandoned in digital carts next year alone. The scale of the drop-off is well understood; its cause is routinely misdiagnosed as an interface or usability problem.1Beyond cart abandonment, payment declines represent a second major source of inefficiency. When a payment fails, only a small proportion of customers attempt an alternative method, while a large proportion abandon the purchase entirely. Each failed transaction therefore represents not only lost revenue in the moment but also a meaningful risk of losing the customer relationship altogether.Most of this leakage is invisible. It shows up as incomplete transactions and softer conversion rather than as discrete system failures, opening a structural gap between consumer intent and transaction execution.That gap is not mainly a matter of user-experience friction. It reflects how decisions are made across checkout.Each transaction depends on a series of independent decisions, including payment method selection, routing, risk evaluation, and authorization, that are executed across fragmented systems with limited shared intelligence.

Exhibit 1. Value Leakage at Checkout

Fragmented Decision-Making

The value leakage in the e-commerce funnel stems less from poor user experience than from a structural consequence of how the payments ecosystem is designed. Every transaction involves three core participants: Merchants, Payment Processors, and Issuing Banks, each operating with only partial information about the transaction. While each player holds critical data, no participant has a complete view of the end-to-end decision context. As a result, each participant optimizes within its own domain. Merchants focus on conversion, processors on routing efficiency, and issuers on fraud prevention, creating a system that is locally rational but globally suboptimal.

In the absence of a shared intelligence layer, conservative decisions at one stage often cancel out value created at another. The payments stack, as currently designed, is optimized for settlement reliability and regulatory compliance, not for coordinated decision-making across the transaction lifecycle. This structural limitation is what constrains checkout performance today.

Exhibit 2: Data Visibility Across Transaction Participants

Optimization Within Silos Has Hit a Ceiling

Checkout friction is not one problem but three, and they map cleanly onto the three participants. Discovery friction, where buyers stitch search and comparison across fragmented sites, is owned by the merchant. Execution friction, where payment-method choice drives abandonment, is owned by the processor. Authorization friction, where conservative issuer logic rejects legitimate intent, is owned by the issuer. The three are mutually exclusive and, together, account for where value leaks.

Predictive AI attacked all three and delivered real gains: ML-driven ranking sharpened discovery, smart payment-method ordering eased execution, and ML risk scoring lifted approval rates. But every gain landed inside a single participant’s domain. Each silo got better at its own decision while the decisions stayed disconnected. Therefore, conservative choices at one stage continued to cancel out value created at another.

The constraint is no longer algorithmic. It is architectural. Predictive AI improves decisions; it does not connect them. Macro outcomes confirm it: cart abandonment remains near 70%, conversion has plateaued, and approval gains are incremental. The next leg of value will come not from better models within each layer but from coordinated decisioning across them, which is what agentic AI structurally enables. The system is approaching diminishing returns from optimization alone. The next opportunity lies in coordinating decisions across the transaction lifecycle.

Exhibit 3: From Friction to Agentic Resolution

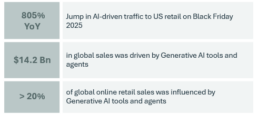

The shift to agentic commerce is no longer theoretical. During the 2025 holiday season, AI agents and assistants began influencing purchase decisions and completing transactions at meaningful scale, prompting major technology and payments players to accelerate their investment in the space.

Exhibit 4: Early Signals of Agentic at Scale (4)

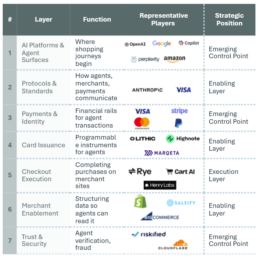

Beneath these early signals, a new commerce stack is rapidly emerging. Every agent-initiated purchase depends on multiple layers, from AI platforms and protocols to payments, merchant infrastructure, identity, and trust networks.

Every transaction touches these layers, from the AI surface where intent originates to the infrastructure that authorizes, coordinates, and completes the purchase. As agentic commerce scales, competition is increasingly shifting toward defining how these layers interact.

Exhibit 5 : The Agentic Commerce Value Chain4 (4)

Not every layer will capture equal value. As agentic commerce scales, advantage is likely to accrue to participants that control intent, identity, trust, and orchestration rather than transaction execution alone.

The race is already underway and players like Google (AP2), Visa (TAP), and Mastercard (Agent Pay) are all competing to define the future control points of commerce.

Agentic AI Shifts Control to Systems

Recent advances in AI are enabling a shift from decision support to decision execution. Rather than simply optimizing checkout, AI systems are increasingly capable of acting on behalf of users, interpreting intent, evaluating options, and completing transactions autonomously. Consumers no longer navigate fragmented interfaces across multiple merchants. Instead, they delegate an outcome to an agent that translates intent into action across the transaction lifecycle. The deeper implication isn’t better interfaces; it is a fundamental change in how transactions are structured.

Today, the consumer acts as the integration layer, stitching together discovery, evaluation, and checkout across disconnected systems. In an agentic model, that work shifts to AI and complexity moves from the user to the system. Checkout evolves from a user interface into a system-level orchestration problem, where decisions are executed through coordinated interactions across the commerce stack.

Exhibit 6: The Integration Layer Is Shifting from Humans to AI

Walmart Sparky: Proof That Orchestration Creates Value

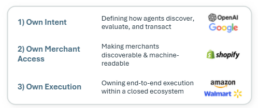

As agentic commerce develops, participants are pursuing three distinct strategies to establish control over the transaction lifecycle. Some are building the agent layer, some are making merchants agent-ready, and some are embedding agentic execution directly into commerce experiences.

Exhibit 7: Control Points Are Being Contested

The clearest proof of value today comes from Walmart Sparky. Unlike most participants, Walmart controls the agent, catalogue, customer identity, payment experience, fulfilment network, and merchant relationship.

Rather than optimizing individual steps in isolation, Sparky coordinates decisions across the entire transaction lifecycle; letting intent, discovery, personalization, payment, and fulfilment to operate as a single system rather than a collection of disconnected workflows.5

Exhibit 8: Walmart Sparky in Production

The reported results suggest that value emerges when decision-making is coordinated across layers rather than optimized within them. Walmart’s advantage isn’t a better AI assistant, it is the ability to connect intent, identity, catalogue, payment, and fulfilment within a single ecosystem.

While few participants can replicate Walmart’s level of vertical integration, the implications extend far beyond retail. Whether through ownership, partnerships, or standards, participants across the ecosystem are pursuing the same objective: becoming the coordination layer that sits between consumer intent and transaction execution.

The competition is no longer for checkout share alone. It is for ownership of the orchestration layer that determines how agent-initiated commerce operates.

The Cross-Layer Orchestration Problem

While consumers experience digital commerce through simple interfaces such as product pages and checkout buttons, each transaction is executed across a complex set of backend systems that must operate in real time. Modern checkout platforms aren’t single applications, they’re multi-layered transaction systems spanning identity, fraud, orchestration, payments, and analytics.

But the deeper issue it that the infrastructure was built for human-initiated transactions, and agentic commerce operates differently. Transactions are increasingly policy-driven, continuous, and machine-to-machine, creating a structural mismatch between how the system is designed and how it is beginning to be used.

This shift has implications across every layer of the stack. Identity systems must move from authenticating users at a point in time to supporting delegated identity, where agents act as credentialed proxies within defined permission boundaries.

Merchant systems must move beyond interface-driven checkout flows to expose structured, machine-readable data that agents can consume directly. Checkout therefore evolves from a linear sequence of system calls into a cross-layer orchestration process, where decisions are made holistically rather than independently. The strategic implication is clear: value will increasingly accrue to systems that can integrate signals across layers and enable real-time, programmable coordination.

Exhibit 9: Commerce Stack Underpinning Every Transaction

Three Unsolved Problems Define the Land Grab

Agentic commerce will scale only as fast as three structural problems are solved. None has been solved yet, and the participants that solve each first will price the next decade of digital transactions.

Each problem has a natural owner. The move each player should make follows directly from what they already control.

Issuers sit closest to the customer and own the trust problem most directly. The opportunity is to be first to let customers safely authorize an agent and set its spending boundaries – and then turn proprietary identity and risk signals into the reason agents and merchants prefer your cardholders’ transactions over anyone else’s. Whoever defines the consent and limit model that customers actually adopt will set the standard for the rest of the ecosystem.

Processors and orchestrators own the rules layer. Their move is to become the single connection that works across every competing protocol – ACP, UCP, AP2, TAP, Agent Pay, so merchants integrate once instead of five times. The strategic prize isn’t betting on which standard wins; it’s making protocol fragmentation invisible to the merchant. Whoever delivers that abstraction will become the default routing layer for agent-initiated transactions.

Wallets and commerce players own two things at once: the consent moment and reach. They are the surface where customers actually approve agents to act, and they have direct distribution into both ends of the transaction – the AI interface where intent is captured, and the merchant catalogs where it is fulfilled. The opportunity is to extend that approval across every AI surface and every merchant they touch, becoming the default credential for agent transactions.

Exhibit 10: The Three Problems

Agentic Commerce Will Scale Gradually, But Control Will Be Won Early

Agentic commerce is advancing rapidly, but scaling it requires clearing structural constraints that remain unsolved. Identity systems built for humans leave a gap in how autonomous actions are authenticated and authorized; fraud models must shift from point-in-time checks to continuous validation of agent behaviour; and most infrastructure still lacks the structured data, real-time visibility, and API access machine execution requires. Regulatory uncertainty compounds all of it, with accountability still unclear across agents, merchants, and financial institutions.

These aren’t isolated technical gaps, they’re systemic barriers to coordinated decision-making, and the economic cost is already visible.

False declines alone are among the largest sources of preventable revenue loss in digital commerce, yet they go unmeasured because they surface as missed conversions rather than outright failures.

The patter holds: the next phase of value will come not from optimizing within existing systems, but from coordinating decisions across them.

As these constraints are cleared, agentic commerce will scale in stages, AI first as an assistant that improves discovery and checkout while the user stays in control; then delegated models, where agents execute repeatable transactions within set constraints; and ultimately end-to-end, machine-to-machine execution across the ecosystem.